A New Generalized Kumaraswamy Distribution

Abstract

A new five-parameter continuous distribution which generalizes the Kumaraswamy and the beta distributions as well as some other well-known distributions is proposed and studied. The model has as special cases new four- and three-parameter distributions on the standard unit interval. Moments, mean deviations, Rényi’s entropy and the moments of order statistics are obtained for the new generalized Kumaraswamy distribution. The score function is given and estimation is performed by maximum likelihood. Hypothesis testing is also discussed. A data set is used to illustrate an application of the proposed distribution.

Keywords: Beta distribution; Continuous proportions; Generalized Kumaraswamy distribution; Kumaraswamy distribution; Maximum likelihood; McDonald Distribution; Moments.

1 Introduction

We introduce a new five-parameter distribution, so-called generalized Kumaraswamy (GKw) distribution, which contains some well-known distributions as special sub-models as, for example, the Kumaraswamy (Kw) and beta () distributions. The GKw distribution allows us to define new three- and four-parameter generalizations of such distributions. The new model can be used in a variety of problems for modeling continuous proportions data due to its flexibility in accommodating different forms of density functions.

The GKw distribution comes from the following idea. Wahed (2006) and Ferreira and Steel (2006) demonstrated that any parametric family of distributions can be incorporated into larger families through an application of the probability integral transform. Specifically, let be a cumulative distribution function (cdf) with corresponding probability density function (pdf) , and be a pdf having support on the standard unit interval. Here, and represent scalar or vector parameters. Now let

| (1) |

Note that is a cdf and that and have the same support. The pdf corresponding to (1) is

| (2) |

This mechanism for defining generalized distributions from a parametric cdf is particularly attractive when has a closed-form expression.

The beta density is often used in place of . However, different choices for have been considered in the literature. Eugene et al. (2002) defined the beta normal distribution by taking to be the cdf of the standard normal distribution and derived some of its first moments. More general expressions for these moments were obtained by Gupta and Nadarajah (2004a). Nadarajah and Kotz (2004) introduced the beta Gumbel (BG) distribution by taking to be the cdf of the Gumbel distribution and provided closed form expressions for the moments, the asymptotic distribution of the extreme order statistics and discussed the maximum likelihood estimation procedure. Nadarajah and Gupta (2004) introduced the beta Fréchet (BF) distribution by taking to be the Fréchet distribution, derived the analytical shapes of its density and hazard rate functions and calculated the asymptotic distribution of its extreme order statistics. Also, Nadarajah and Kotz (2006) dealt with the beta exponential (BE) distribution and obtained its moment generating function, its first four cumulants, the asymptotic distribution of its extreme order statistics and discussed maximum likelihood estimation.

The starting point of our proposal is the Kumaraswamy (Kw) distribution (Kumaraswamy, 1980; see also Jones, 2009). It is very similar to the beta distribution but has a closed-form cdf given by

| (3) |

where , and . Its pdf becomes

| (4) |

If is a random variable with pdf (4), we write . The Kw distribution was originally conceived to model hydrological phenomena and has been used for this and also for other purposes. See, for example, Sundar and Subbiah (1989), Fletcher and Ponnambalam (1996), Seifi et al. (2000), Ganji et al. (2006), Sanchez et al. (2007) and Courard-Hauri (2007).

In the present paper, we propose a generalization of the Kw distribution by taking as cdf (3) and as the standard generalized beta density of first kind (McDonald, 1984), with pdf given by

| (5) |

where , and , is the beta function and is the gamma function. If is a random variable with density function (5), we write . Note that if then , i.e., has a beta distribution with parameters and .

The article is organized as follows. In Section 2, we define the GKw distribution, plot its density function for selected parameter values and provide some of its mathematical properties. In Section 3, we present some special sub-models. In Section 4, we obtain expansions for the distribution and density functions. We demonstrate that the GKw density can be expressed as a mixture of Kw and power densities. In Section 5, we give general formulae for the moments and the moment generating function. Section 6 provides an expansion for the quantile function. Section 7 is devoted to mean deviations about the mean and the median and Bonferroni and Lorenz curves. In Section 8, we derive the density function of the order statistics and their moments. The Rényi entropy is calculated in Section 9. In Section 10, we discuss maximum likelihood estimation and determine the elements of the observed information matrix. Section 11 provides an application to a real data set. Section 12 ends the paper with some conclusions.

2 The New Distribution

We obtain an appropriate generalization of the Kw distribution by taking as the two-parameter Kw cdf (3) and associated pdf (4). For , we consider a three-parameter generalized beta density of first kind given by (5). To avoid non-identifiability problems, we allow to vary on only. We then write which varies on . Using (1), the cdf of the GKw distribution, with five positive parameters , , , and , is defined by

| (6) |

where is the parameter vector.

The pdf corresponding to (6) is straightforwardly obtained from (2) as

| (7) |

Based on the above construction, the new distribution can also be referred to as the McDonald Kumaraswamy (McKw) distribution. If is a random variable with density function (7), we write .

An alternative, but related, motivation for (6) comes through the beta construction (Eugene et al., 2002). We can easily show that

| (8) |

where denotes the incomplete beta function ratio. Thus, the GKw distribution can arise by taking the beta construction applied to a new distribution, namely the exponentiated Kumaraswamy (EKw) distribution, to yield (7), which can also be called the beta exponentiated Kumaraswamy (BEKw) distribution, i.e., a beta type distribution defined by the baseline cumulative function .

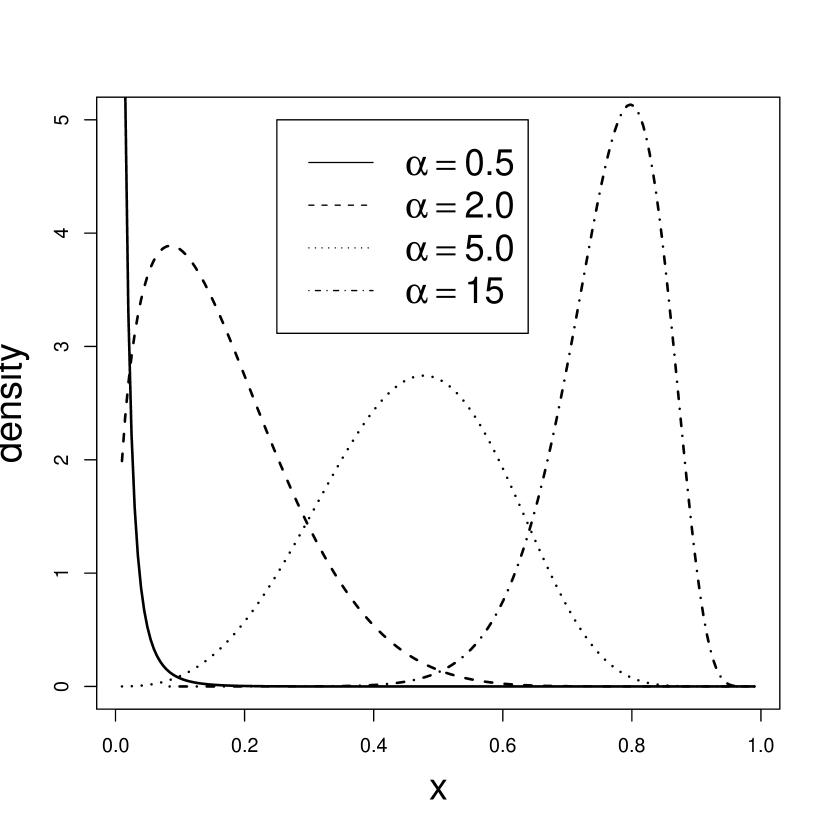

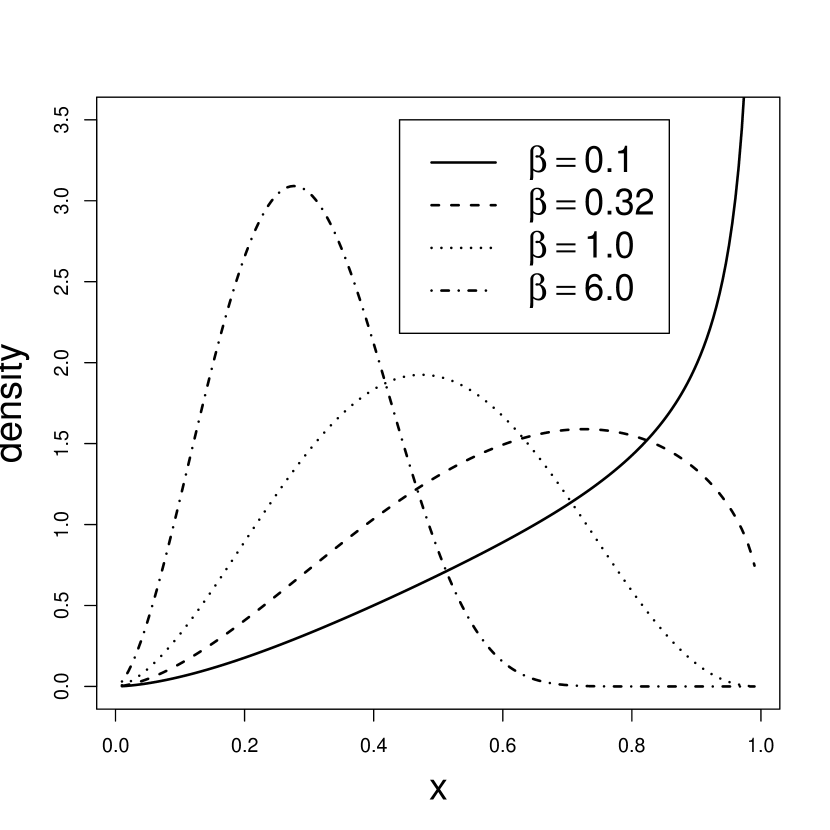

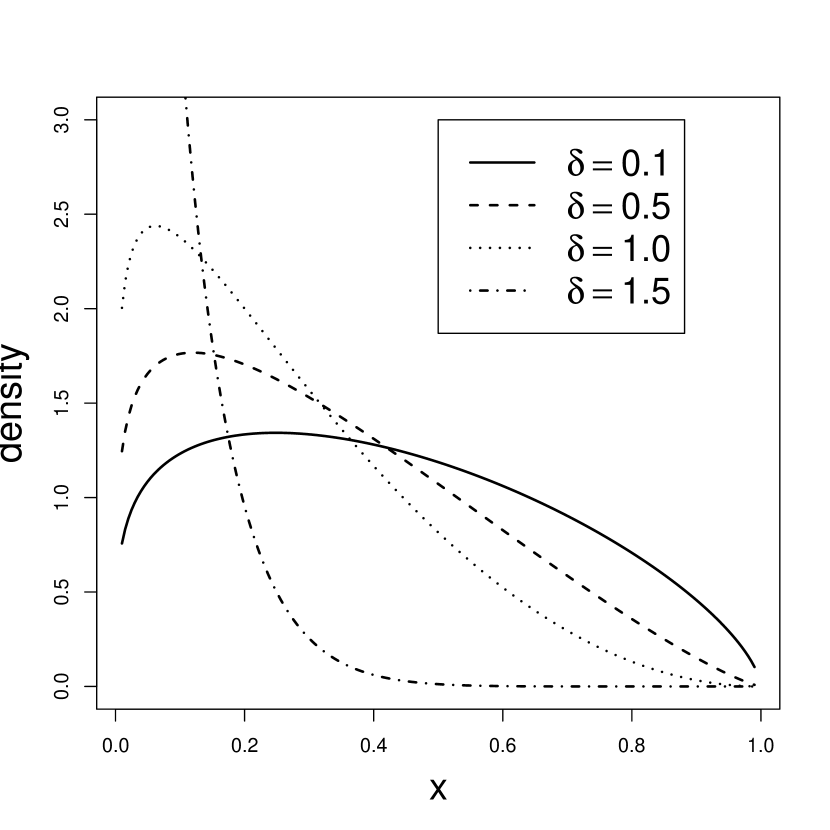

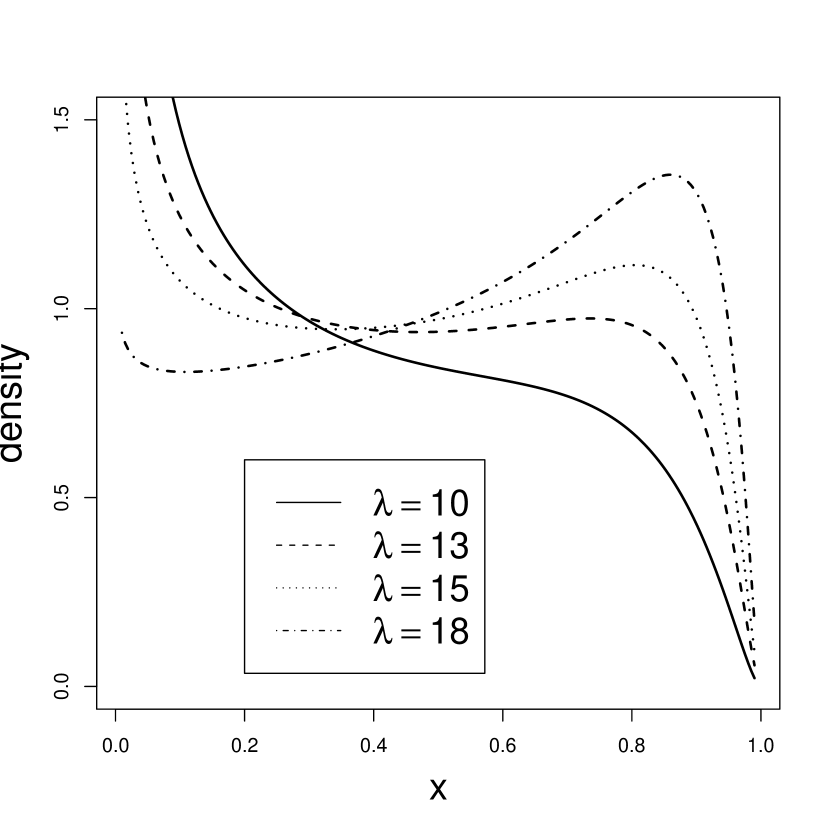

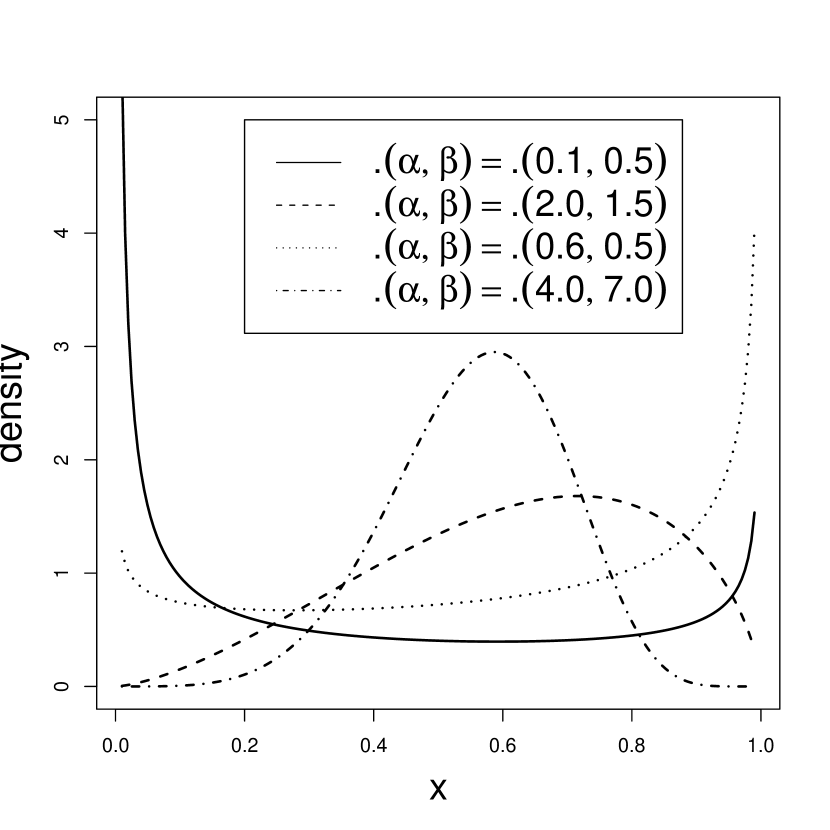

Immediately, inverting the transformation motivation (8), we can generate following the GKw distribution by , where is a beta random variable with parameters and . This scheme is useful because of the existence of fast generators for beta random variables. Figure 1 plots some of the possible shapes of the density function (7). The GKw density function can take various forms, bathtub, , inverted , monotonically increasing or decreasing and upside-down bathtub, depending on the parameter values.

(a)

(b)

(c)

(d)

(e)

(f)

(g)

(h)

(i)

We now provide two properties of the GKw distribution.

Proposition 1. If , then for .

Proposition 2. Let and . Then, the pdf of is given by

| (9) |

We call (9) the log-generalized Kumaraswamy (LGKw) distribution.

3 Special Sub-Models

The GKw distribution is very flexible and has the following distributions as special sub-models.

The Kumaraswamy distribution (Kw)

The McDonald distribution (Mc)

For , we obtain the Mc distribution (5) with parameters , and .

The beta distribution

If , the GKw distribution reduces to the beta distribution with parameters and .

The beta Kumaraswamy distribution (BKw)

The Kumaraswamy-Kumaraswamy distribution (KwKw)

The EKw distribution

If and , (7) gives

It can be easily seen that the associated cdf can be written as

where is the cdf of the distribution. This distribution was defined before as the EKw distribution which is a new three-parameter generalization of the Kw distribution.

The beta power distribution (BP)

For and , (9) reduces to

This density function can be obtained from (2) if and is taken as the beta density with parameters and . We call this distribution as the BP distribution.

The LGKw distribution (9) contains as special sub-models the following distributions.

The beta generalized exponential distribution (BGE)

For , (9) gives

| (10) |

which is the density function of the BGE distribution introduced by Barreto-Souza et al. (2010). If and in addition to , the LGKw distribution becomes the generalized exponential distribution (Gupta and Kundu, 1999). If and , (10) coincides with the exponential distribution with mean .

The beta exponential distribution (BE)

For and , (9) reduces to

which is the density of the BE distribution introduced by Nadarajah and Kotz (2006).

4 Expansions for the Distribution and Density Functions

We now give simple expansions for the cdf of the GKw distribution. If and is a non-integer real number, we have

| (11) |

where (for ) is the descending factorial. Clearly, if is a positive integer, the series stops at . Using the series expansion (11) and the representation for the GKw cdf (6), we obtain

if is a non-integer real number. By simple integration, we have

| (12) |

where

| (13) |

and is given by (3). If is a positive integer, the sum stops at .

The moments of the GKw distribution do not have closed form. In order to obtain expansions for these moments, it is convenient to develop expansions for its density function. From (12), we can write

If we replace by (3) and use (4), we obtain

| (14) |

where with Here, and denotes the density function with parameters and . Further, we can express (14) as a mixture of power densities, since the Kw density (4) can also be written as a mixture of power densities. After some algebra, we obtain

| (15) |

where

Equations (14) and (15) are the main results of this section. They can provide some mathematical properties of the GKw distribution from the properties of the Kw and power distributions, respectively.

5 Moments and Moment Generating Function

Let be a random variable having the GKw distribution (7). First, we obtain an infinite sum representation for the rth ordinary moment of , say . From (14), we can write

| (16) |

where is the rth moment of the distribution which exists for all . Using a result due to Jones (2009, Section 3), we have

| (17) |

Hence, the moments of the GKw distribution follow directly from (16) and (17). The central moments and cumulants of are easily obtained from the ordinary moments by and , etc., respectively. The th descending factorial moment of is

where is the Stirling number of the first kind given by . It counts the number of ways to permute a list of items into cycles. Thus, the factorial moments of are given by

The moment generating function of the GKw distribution, say , is obtained from (15) as

By changing variable, we have

and then reduces to the linear combination

where denotes the incomplete gamma function.

6 Quantile Function

We can write (8) as , where . From Wolfram’s website444http://functions.wolfram.com/06.23.06.0004.01 we can obtain some expansions for the inverse of the incomplete beta function, say , one of which is

where for and , , ,

The coefficients s for can be derived from the cubic recursion (Steinbrecher and Shaw, 2007)

where if and if . In the last equation, we note that the quadratic term only contributes for . Hence, the quantile function of the GKw distribution can be written as .

7 Mean Deviations

If has the GKw distribution, we can derive the mean deviations about the mean and about the median from

respectively. From (8), the median is the solution of the nonlinear equation

These measures can be calculated using the relationships

Here, the integral is easily calculated from the density expansion (15) as

We can use this result to obtain the Bonferroni and Lorenz curves. These curves have applications not only in economics to study income and poverty, but also in other fields, such as reliability, demography, insurance and medicine. They are defined by

respectively, where .

8 Moments of Order Statistics

The density function of the ith order statistic , say , in a random sample of size from the GKw distribution, is given by (for )

| (18) |

The binomial expansion yields

and using and integrating (15) we arrive at

where .

We use the following expansion for a power series raised to a integer power (Gradshteyn and Ryzhik, 2000, Section 0.314)

| (19) |

where is any positive integer number, and for all .] We can write

where and (for )

The rth moment of the ith order statistic becomes

| (20) |

We now obtain another closed form expression for the moments of the GKw order statistics using a general result due to Barakat and Abdelkader (2004) applied to the independent and identically distributed case. For a distribution with pdf and cdf , we can write

where

For a positive integer , we have

By replacing (12) in the above equation we have

| (25) |

By replacing by (3) and using (11) we obtain

where . Since for (Gupta and Nadarajah, 2004b), we have

where

Finally, reduces to

| (32) |

Equations (20) and (32) are the main results of this section. The L-moments are analogous to the ordinary moments but can be estimated by linear combinations of order statistics. They are linear functions of expected order statistics defined by (Hoskings, 1990)

The first four L-moments are , , and . These moments have several advantages over the ordinary moments. For example, they exist whenever the mean of the distribution exists, even though some higher moments may not exist, and are relatively robust to the effects of outliers. From (32) applied for the means (), we can obtain expansions for the L-moments of the GKw distribution.

9 Rényi Entropy

The entropy of a random variable with density function is a measure of variation of the uncertainty. One of the popular entropy measures is the Rényi entropy given by

| (33) |

From (15), we have

In order to obtain an expansion for the above power series for , we can write

Using equation (19), we obtain

where and for all . Hence,

10 Maximum Likelihood Estimation

Let be a random sample from the distribution. From (7) the log-likelihood function is easy to derive. It is given by

By taking the partial derivatives of the log-likelihood function with respect to , , , and , we obtain the components of the score vector, . They are given by

where is the digamma function, , , , and .For interval estimation and hypothesis tests on the model parameters, the observed information matrix is required. The observed information matrix is given in the Appendix.

Under conditions that are fulfilled for parameters in the interior of the parameter space, the approximate distribution of is multivariate normal , where is the maximum likelihood estimator (MLE) of and is the expected information matrix. This approximation is also valid if is replaced by .

The multivariate normal distribution can be used to construct approximate confidence regions. The well-known likelihood ratio (LR) statistic can be used for testing hypotheses on the model parameters in the usual way. In particular, this statistic is useful to check if the fit using the GKw distribution is statistically superior to a fit using the BKw, EKw and Kw distributions for a given data set. For example, the test of versus is equivalent to compare the BKw distribution with the GKw distribution and the LR statistic reduces to , where and are the unrestricted and restricted MLEs of , respectively. Under the null hypothesis, is asymptotically distributed as . For a given level , the LR test rejects if exceeds the -quantile of the distribution.

11 Application

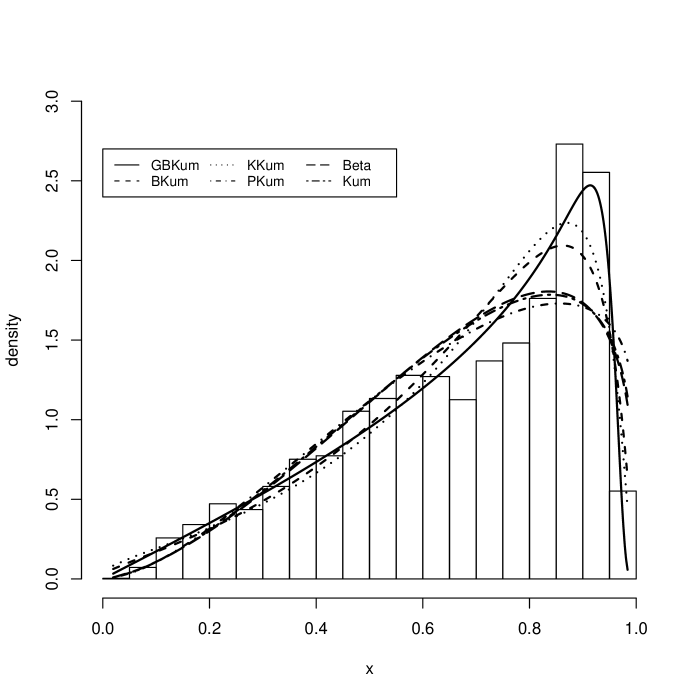

This section contains an application of the GKw distribution to real data. The data are the observed percentage of children living in households with per capita income less than R$ 75.50 in 1991 in 5509 Brazilian municipal districts. The data were extracted from the Atlas of Brazil Human Development database available at http://www.pnud.org.br/. The histogram of the data is shown in Figure 2 along with the estimated densities of the GKw distribution and some special sub-models. Apparently, the GKw distribution gives the best fit.

The GKw model includes some sub-models described in Section 3 as especial cases and thus allows their evaluation relative to each other and to a more general model. As mentioned before, we can compute the maximum values of the unrestricted and restricted log-likelihoods to obtain the LR statistics for testing some sub-models of the GKw distribution.

We test versus is not true,

i.e. we compare the GKw model with the beta model. In this case, (p-value) indicates that the

GKw model gives a better representation of the data than

the beta distribution. Further, the LR statistic for testing

versus , i.e. to

compare the GKw model with the BKw model, is

(p-value). It also yields favorable indication

for the GKw model. Table 1 lists the MLEs of the

model parameters (standard errors in parentheses) for different models. The computations were

carried out using the subroutine MAXBFGS implemented in the Ox matrix

programming language (Doornik, 2007).

| Distribution | ||||||

|---|---|---|---|---|---|---|

| GKw | 18.1161 | 1.8132 | 0.7303 | 0.0609 | 15.7803 | 1510.6670 |

| (0.1829) | (0.0219) | (0.0057) | (0.0008) | (0.8908) | ||

| BKw | 0.0247 | 0.1849 | 26.0933 | 17.3768 | 1383.5690 | |

| (0.0003) | (0.0005) | (0.1054) | (0.0739) | |||

| KKw | 2.7191 | 0.4654 | 0.0968 | 79.9999 | 1405.0650 | |

| (0.0086) | (0.0060) | (0.0005) | (1.0915) | |||

| PKw | 17.9676 | 0.1647 | 1.1533 | 1237.5800 | ||

| (0.2421) | (0.0019) | (0.0054) | ||||

| BP | 0.1590 | 16.7313 | 0.2941 | 1269.9760 | ||

| (0.0018) | (0.1998) | (0.0129) | ||||

| Kw | 2.4877 | 1.3369 | 1278.7860 | |||

| (0.0295) | (0.0180) | |||||

| Beta | 2.5678 | 0.3010 | 1271.5610 | |||

| (0.0317) | (0.0147) |

12 Conclusions

We introduce a new five-parameter continuous distribution on the standard unit interval which generalizes the beta, Kumaraswamy (Kumaraswamy, 1980) and McDonald (McDonald, 1984) distributions and includes as special sub-models other distributions discussed in the literature. We refer to the new model as the generalized Kumaraswamy distribution and study some of its mathematical properties. We demonstrate that the generalized Kumaraswamy density function can be expressed as a mixture of Kumaraswamy and power densities. We provide the moments and a closed form expression for the moment generating function. Explicit expressions are derived for the mean deviations, Bonferroni and Lorenz curves and Rényi’s entropy. The density of the order statistics can also be expressed in terms of an infinite mixture of power densities. We obtain two explicit expressions for their moments. Parameter estimation is approached by maximum likelihood. The usefulness of the new distribution is illustrated in an analysis of real data. We hope that the proposed extended model may attract wider applications in the analysis of proportions data.

Acknowledgments

We gratefully acknowledge financial support from FAPESP and CNPq.

Appendix

The elements of the observed information matrix for are

where , , , , , , and is the first derivative of the digamma function.

References

Barreto-Souza, W., Santos, A. S., Cordeiro, G. M. (2010). The beta generalized exponential distribution. Journal of Statistical Computation and Simulation, 80, 159-172.

Barakat, H., Abdelkader, Y.H. (2004). Computing the moments of order statistics from nonidentical random variables. Statistical Methods and Applications, 13, 15-26.

Courard-Hauri, D. (2007). Using Monte Carlo analysis to investigate the relationship between overconsumption and uncertain access to one’s personal utility function. Ecological Economics, 64, 152-162.

Doornik, J. (2007). Ox: An Object-Oriented Matrix Programming Language. London: Timberlake Consultants Press.

Eugene, N., Lee, C., Famoye, F. (2002). Beta-normal distribution and its applications. Communications in Statistics - Theory and Methods, 31, 497-512.

Ferreira, J.T., Steel M. (2006). A constructive representation of univariate skewed distribution. Journal of the American Statistical Association, 101, 823-829.

Fletcher, S.C., Ponnambalam, K. (1996). Estimation of reservoir yield and storage distribution using moments analysis. Journal of Hydrology, 182, 259-275.

Ganji, A., Ponnambalam, K., Khalili, D., Karamouz, M. (2006). Grain yield reliability analysis with crop water demand uncertainty. Stochastic Environmental Research and Risk Assessment, 20, 259-277.

Gradshteyn, I.S., Ryzhik, I.M. (2000). Table of Integrals, Series, and Products. New York: Academic Press.

Gupta, A.K., Kundu, D. (1999). Generalized exponential distributions. Australian and New Zealand Journal of Statistics, 41, 173-188.

Gupta, A.K., Nadarajah, S. (2004a). On the moments of the beta normal distribution. Communications in Statistics-Theory and Methods, 33, 1-13.

Gupta, A.K., Nadarajah, S. (2004b). Handbook of Beta Distribution and its Applications. New York: Marcel Dekker.

Hoskings, J.R.M. (1990) L-moments: analysis and estimation of distribution using linear combinations of order statistics. Journal of the Royal Statistical Society B, 52, 105-124.

Jones, M.C. (2009). Kumaraswamy’s distributions: A beta-type distribution with some tractability advantages. Statistical Methodology, 6, 70-81.

Kumaraswamy, P. (1980). A generalized probability density function for double bounded random processes. Journal of Hydrology, 46, 79-88.

McDonald, J.B. (1984). Some generalized function for the size distributions of income. Econometrica, 52, 647-663.

Nadarajah, S., Gupta, A.K. (2004). The beta Fréchet distribution. Far East Journal of Theoretical Statistics, 14, 15-24.

Nadarajah, S., Kotz, S. (2004). The beta Gumbel distribution. Mathematical Problems in Engineering, 4, 323-332.

Nadarajah, S. Kotz, S. (2006). The exponentiated type distributions. Acta Applicandae Mathematicae, 92, 97-111.

Sanchez, S., Ancheyta, J., McCaffrey, W.C. (2007). Comparison of probability distribution function for fitting distillation curves of petroleum. Energy and Fuels, 21, 2955-2963.

Seifi, A., Ponnambalam, K., Vlach, J. (2000). Maximization of manufacturing yield of systems with arbitrary distributions of component values. Annals of Operations Research, 99, 373-383.

Steinbrecher, G., Shaw, W.T. (2007). Quantile Mechanics. Department of Theoretical Physics, Physics Faculty, University of Craiova. Working Paper.

Sundar, V., Subbiah, K. (1989). Application of double bounded probability density-function for analysis of ocean waves. Ocean Engineering, 16, 193-200.

Wahed, A.S. (2006). A general method of constructing extended families of distribution from an existing continuous class. Journal of Probability and Statistical Science, 4, 165-177.