Nonlinear stochastic equations with multiplicative Lévy noise

Abstract

The Langevin equation with a multiplicative Lévy white noise is solved. The noise amplitude and the drift coefficient have a power-law form. A validity of ordinary rules of the calculus for the Stratonovich interpretation is discussed. The solution has the algebraic asymptotic form and the variance may assume a finite value for the case of the Stratonovich interpretation. The problem of escaping from a potential well is analysed numerically; predictions of different interpretations of the stochastic integral are compared.

pacs:

02.50.Ey,05.40.Ca,05.40.FbI Introduction

The Langevin equation can not always be expressed by means of a deterministic drift term, supplemented by a time-dependent stochastic force (an additive noise). A physical quantity, which is represented by the random component, may require the noise to depend on the stochastic variable itself. In the Langevin description, that dependence emerges as a variable noise amplitude (a multiplicative noise). The multiplicative noise emerges also in descriptions of complicated systems, as a result of the elimination of fast degrees of freedom. The stochastic equation is then of the form

| (1) |

where and are given functions. The stochastic force is uncorrelated, , and it is characterised by a given probability distribution. In the present paper we assume that has the symmetric stable Lévy distribution defined by the Fourier transform

| (2) |

where is the order parameter and scales the distribution. In Secs.II and III we assume . The case corresponds to the normal distribution which is well known in the context of multiplicative processes vkam ; schen .

The general and stable Lévy processes, for , exhibit long tails of the distribution which makes the moments divergent. They are frequently encountered in nature, since long jumps are associated with a complex structure of the environment, in particular with long-range correlations. Examples can be found in biological physics wes , disordered media bou and finance car1 ; man1 ; san . A master equation description of thermal activation of particles within the folded polymers bro also involves the multiplicative Lévy noise in a sense that the equation is fractional (Lévy jumps) and it contains a variable diffusion coefficient. However, a direct Langevin representation of the topological complexity problem is unknown garb . Since the complex environment is usually nonhomogeneous, one can expect that the Lévy noise in the Langevin equation is rather multiplicative than additive. Therefore formalisms, which are supposed to describe complex processes and which do that in terms of the additive noise alone, may miss essential features of the problem. For example, in the field of finance, the standard Black-Scholes equation contains the additive Gaussian noise. Eq.(1) in its general form could be an important generalisation of that equation car1 ; man1 .

Eq.(1) is not sufficiently defined for the white noise because it is not clear at which time should be evaluated. In the following, we define the stochastic integrals, connected with Eq.(1), as Riemann integrals. According to Stratonovich, one assumes

| (3) |

where and is a time step. This interpretation is appropriate for many physical phenomena since it constitutes a white noise limit for correlated processes. In this case Eq.(1) can be solved like usual differential equation, which can be rigorously proved if has the convergent variance gar ; zee . In particular, one can introduce a transformation

| (4) |

which leads to the Langevin equation with the additive noise:

| (5) |

Alternatively, we can simply assume

| (6) |

which formula defines the Itô interpretation. Predictions of Eq.(1) in both interpretations are different but in the case in Eq.(2) there is a simple relation between them: the difference resolves itself to the spurious drift gar . For such a relation does not exist. The Stratonovich interpretation predicts a dependence of the probability distribution on the noise amplitude which may change the diffusion properties of the system; in particular the accelerated diffusion, in the case of the additive noise, can change to the subdiffusion. That problem is discussed in Ref.sro for the case without drift and for the linear drift. In the Itô interpretation, in turn, shape of the distribution tail is not affected by the amplitude sro2 .

In this paper we discuss properties of the Langevin equation which is driven by the multiplicative Lévy noise and nonlinear forces, in particular the problem of escaping from a potential well. In Sec.II, properties of stochastic integrals for the stable Lévy processes and those with truncated distributions are compared. The Fokker-Planck equation for the problem of an algebraic, nonlinear potential is solved in Sec.III. The escape from the potential well, understood as the first passage time problem, is calculated in Sec.IV and results for both interpretations of the stochastic integral are compared.

II Stable Lévy distributions versus truncated ones

A well known property of the Stratonovich integral (3) allows us to apply standard rules of the calculus and then to reduce Eq.(1) to an equivalent equation with the additive noise. It can be proved gar ; zee for the normally distributed noise, i.e. on the assumption that increments are independent and the variance is finite. For the general Lévy stable processes the latter condition is not satisfied. However, we can approximate Lévy distributions by introducing a truncation at some large value of the argument either in a form of the sharp cut-off or as a rapidly falling tail. Then a sum of stochastic variables converges to the normal distribution, according to the central limit theorem. Since in the physical phenomena process values are usually finite, introducing truncated distributions is realistic. In the random walk theory, the truncated Lévy flights are often considered car1 ; man ; man1 ; kop ; sro1 . They agree with the Lévy flights for an arbitrarily large jump value; deviations appear only at very far tails man . However, there are also remarkable differences between processes which involve the stable distribution and the truncated one. We will demonstrate that difference for a simple case of the linear noise.

Let and . If the standard rules of the calculus work – we can expect that for the Stratonovich interpretation – the variable in Eq.(1) can be changed. As a result we obtain from Eq.(5) the probability density distribution in the ’log-Lévy’ form

| (7) |

where denotes the Lévy distribution with order parameter , width parameter and . If the process is continuous the point acts as an absorbing barrier, i.e. for . It is the case for the Wiener process but it may no longer be true if the variance is divergent; then Eq.(7) is no longer valid. The distribution in the form Eq.(7) for is known as the log-normal distribution and it is frequently encountered in nature, e.g. electron velocities in the solar wind shlc , as well as rainfall amounts atc obey this statistics. Moreover, it can serve as a natural model of the multifragmentation shlw .

On the other hand, we can solve Eq.(1) for the Stratonovich interpretation directly from the definition, by means of Eq.(3). The discretisation gives us ; therefore , where . The final solution of the stochastic equation reads

| (8) |

where . If a cut-off is introduced, for a small . We take the logarithm of Eq.(8), approximate by and neglect terms of the order and higher. That procedure yields

| (9) |

The above expression converges to the Lévy distribution with the order parameter , unless is large compared to the cut-off position, and we obtain Eq.(7). Since the variance is finite for the process with the truncated distribution, in the limit the normal distribution must be reached, according to the central limit theorem, but the convergence is extremely slow.

The case of the stable distribution is distinguished by the presence a considerable number of events for which is not small for any given . Difference in respect to the case of the truncated distribution, due to the presence of those events, becomes visible when we consider the distribution for negative . Obviously in the limit of small , if any cut-off is introduced. For the case without truncation, may turn to the negative. Let us estimate the probability that this cannot happen, i.e. that all factors in Eq.(8) are positive. We have , where . Since , we may insert the asymptotic form of the Lévy distribution, . Then . Finally we have

| (10) |

Probability that at least one of the terms in Eq.(8) becomes negative, , appears finite and it rises with time to unity. One can easily demonstrate that converges to one with for any if is normally distributed. In this case for .

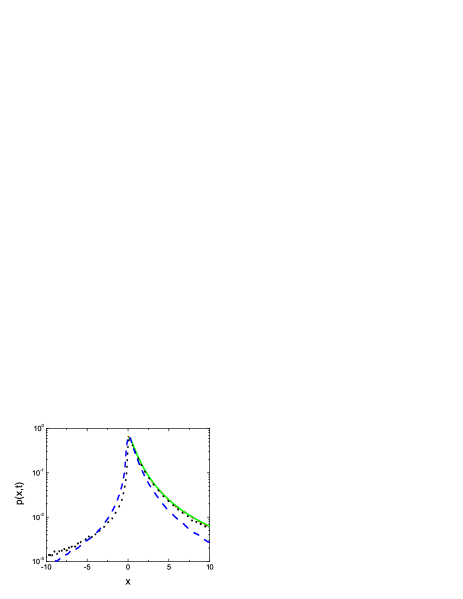

Numerical analysis of the above case is presented in Fig.1. The distribution (7) was evaluated by means of the series expansion

| (11) |

The result for the truncated distribution is identical with Eq.(7) whereas the case without any cut-off (marked by dots) exhibits a branch for the negative . However, both distributions for are very similar and then Eq.(7) can serve as an approximation of the Lévy stable case. The result for the Itô interpretation, Eq.(6), is also presented in Fig.1. It falls much faster than the Stratonovich one.

III Nonlinear case

In this section we consider stochastic processes which are governed by Eq.(1) with a nonlinear deterministic force. This problem is an important generalisation, compared to the linear case, since the corresponding Newton equation may become nonintegrable and the dynamics is then chaotic. It happens for a periodic time- dependent driving (the Duffing oscillator) or if the system has more than two degrees of freedom lich . We assume the algebraic and :

| (12) |

In the new variable,

| (13) |

the Langevin equation, Eq.(5), has the additive noise. The corresponding fractional Fokker-Planck equation is of the form

| (14) |

where and . The drift term in Eq.(14) corresponds to the effective potential . We are interested in the asymptotic shape of a steady-state solution . The solution for large can be found by taking into account small wave numbers in the Fourier expansion. The Fourier transform of Eq.(14) in the stationary limit reads

| (15) |

We assume the solution in the form of the Fox function mat ; sri ,

| (19) |

where is the normalisation constant and the coefficients are to be determined. Some useful properties of the Fox functions are presented in Appendix. Eq.(19) represents the stable and symmetric Lévy distribution for , and sch . We insert Eq.(19) into Eq.(15) and apply the general formula (A7) in order to get rid of the algebraic factor. Then we calculate the Fourier transform, according to the formula (A14), and expand both sides of Eq.(15) by using the Fox function series representation, Eq.(A18). Eq.(15) takes the form

| (20) |

where , and are constants. The above equation is satisfied if and which conditions determine the coefficients: and . The condition , where

| (21) |

can be satisfied by an appropriate choice of .

The asymptotic behaviour of follows from expansion of the Fox function in powers of : it can be obtained by a variable transformation by means of Eq.(A25) and by applying Eq.(A18). The first term produces the result which, after transformation to the original variable according to the formula , yields the final result

| (22) |

To satisfy the normalisation condition, we assume . Eq.(22) predicts the Lévy stable distribution with a divergent variance for . If , the variance is finite though higher moments may be divergent. Therefore, long tails of the distribution can be confined either by choosing a sufficiently steep potential or an appropriate noise. The latter must be such that amplitude declines with position sufficiently fast (large ) and/or the order parameter is large (steep tails). The case corresponds to the harmonic oscillator; it is discussed in Ref.sro . If and is an odd integer, an analytical expression for the stationary probability distribution, valid for arbitrary , can be derived che .

On the other hand, we solve Eq.(1) by a numerical simulation of stochastic trajectories. It can be performed in two ways. First, we directly apply the discretisation formula which follows from Eq.(3) and is of the form wer

| (23) |

To find the process value, one has to solve, at each step, the following nonlinear equation

| (24) |

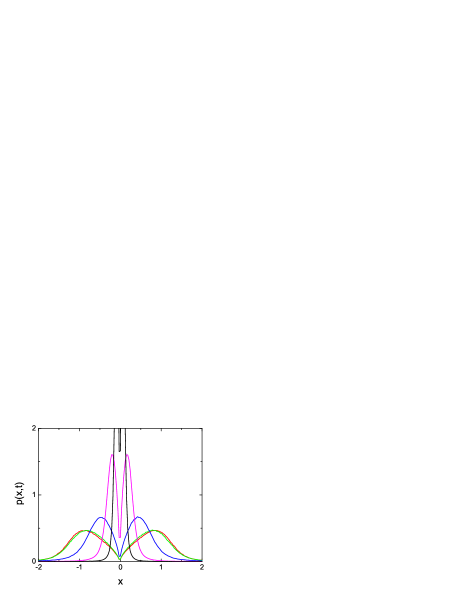

where . For that purpose we apply the parabolic interpolation scheme (the Muller method) ral . The algorithm must be carefully implemented since, due to the explicit multiplication of the noise by the dependent factor, the round-off errors are large and then it is difficult to achieve a high accuracy of the results. Alternatively, we can first transform Eq.(1) to Eq.(5), simulate trajectories to find and finally transform the distribution: . Comparison of both algorithms is presented in Fig.2 for positive and negative ; the distributions are actually identical. In the following simulations we apply the method of variable transformation.

Distributions which are initially positioned at evolve with time to the steady state. The convergence appears very fast. Example of the evolution is presented in Fig.3 for and . The stationary distribution is reached already at .

Various sets of parameters , and define processes which are either stable Lévy ones, with divergent variance, or processes with heavy tails, for which the variance exists but higher moments are divergent. Examples are presented in Fig.4. The case of negative and a weakly changing (the case 1. in the figure) corresponds to the slope 2.6, in the other cases the slope is larger than three. Slopes of the straight lines in the figure follow from the asymptotic formula, Eq.(22), and they agree with the numerical results.

IV Escape from a potential well

A particular case of Eq.(1), which involves the nonlinear deterministic force and the boundary conditions, is the problem of passing over a potential barrier. This problem is of great physical importance and it has been extensively studied for the case of the normal distribution han . For example, fusion of heavy ions in nuclear physics consists in a transfer of mass over the Coulomb barrier. A multiplicative noise emerges when one considers a parametric activation of the potential, i.e. if height of the barrier randomly varies woz . Increasing intensity of the multiplicative noise in the bistable stochastic system can produce a stochastic resonance gamm . Properties of systems driven by general Lévy stable noises may be different than those for . In particular, a waiting time for noise-induced jumping between metastable states may depend, due to the presence of single long jumps, more on the width than on the height of the barrier dit . Moreover, the ratio of first mean passage time from one to the other minimum is no longer twice of the time to reach the top of the barrier dyb2 . Asymmetry in the Lévy distribution affects the escape time; it can both enhance and suppress the escape events. The rate of escape, as a function of the parameter , is discontinuous. It was recently demonstrated that a double stochastic resonance can be observed in a single well potential without explicit external driving, if the Lévy stable noise is introduced dyb3 .

In this section we consider the problem of escaping from the potential well for the multiplicative noise and, in particular, the dependence of the mean first passage time (MFPT) on the specific interpretation of the stochastic integral, either Stratonovich or Itô. We assume the potential in the form

| (25) |

and the noise amplitude is given by Eq.(12). The main quantity of interest is the dependence of MFPT on the parameter , which quantifies the noise amplitude variability. The transformed Fokker-Planck equation with additive noise is the following

| (26) |

where

| (27) |

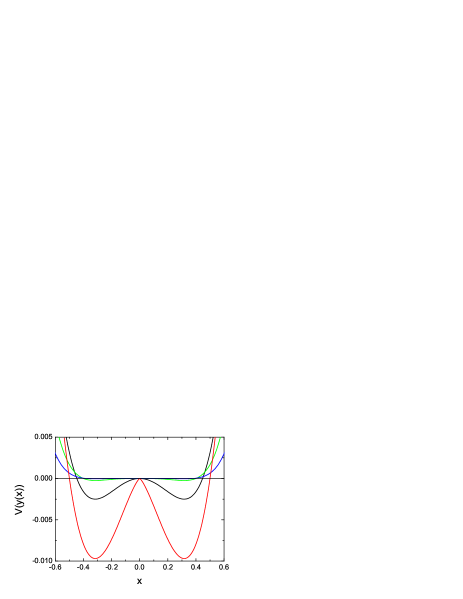

The effective drift depends only on the ratio . We can infer some qualitative conclusions about the dynamics from the shape of an effective potential, which follows from Eq.(27). This potential, as a function of the original variable , is presented in Fig.5. The height of the barrier falls sharply with – the potential is very shallow for negative – whereas position of the barrier is constant. Therefore we can expect a suppression of transport, which is defined by the boundary conditions in the variable , for large .

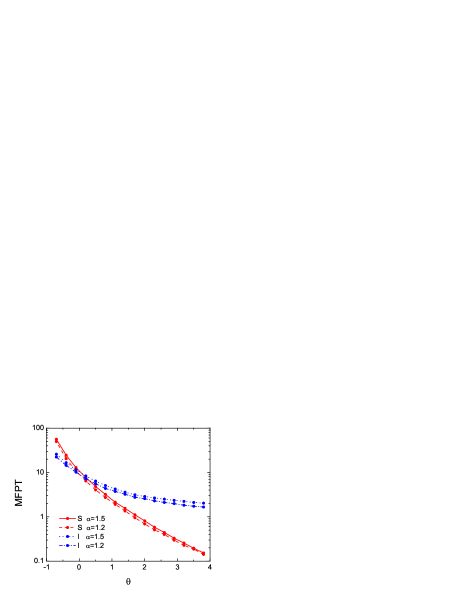

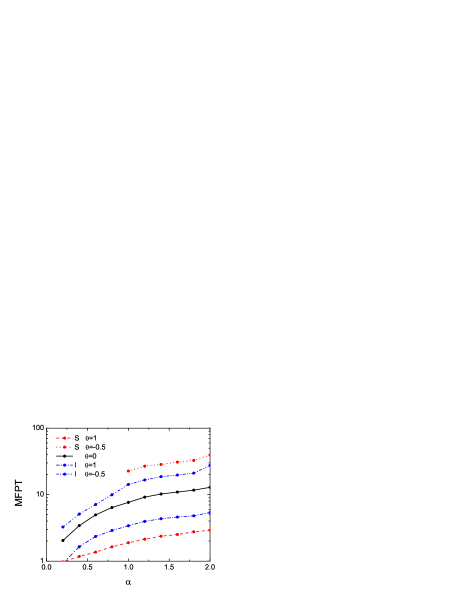

A numerical analysis of the potential barrier problem must take into account that the system under consideration is limited in space. Long tails of the distribution may not manifest themselves if the available space is too small. Therefore, in the following, we rescale the system by putting in Eq.(2) . MFPT, defined as a time the particle needs to pass for the first time from the left minimum of the potential to any , was calculated by numerical solving of Eq.(5) with the initial condition and the boundary condition at the absorbing barrier, . The average time, as a function of for two values of , 1.5 and 1.2, is presented in Fig.6. It falls sharply with , like an exponential, which is a consequence of the shallow effective potential for large . Results for both values of are similar, they differ only by a constant factor. MFPT rises with since jumps become shorter. This result is presented in Fig.7; a difference between the case of positive and negative one is substantial.

Predictions for the Itô interpretation are also presented in Figs.6 and 7. The dependence of MFPT on is much weaker than for the Stratonovich case; MFPT falls algebraically for large . In this case, the dynamics is affected by the noise only near the top of the barrier – the noise is then localised and very strong – while inside the well the deterministic trapping dominates. Results for different are qualitatively the same. Moreover, MFPT rises with in the Itô case, similarly as in the Stratonovich interpretation.

V Summary and conclusions

Lévy distribution is characterised by long tails which cause the divergent moments. If noise in the Langevin equation is defined in terms of the Lévy distribution, the influence of the tails can be confined either by the potential or by the variable noise amplitude. Then the process which is described by the Langevin equation may have a finite variance. We studied such processes by solving the Langevin equation with the multiplicative Lévy noise and nonlinear drifts. The asymptotic shape of the stationary probability distribution depends both on the noise amplitude, assumed in the power-law form with the parameter , and on the potential slope , according to Eq.(22). If the above parameters are large enough, the variance is finite for any order parameter . The asymptotic formula (22) is valid only for the Stratonovich interpretation; in the Itô interpretation, the distribution is less sensitive on the slope of the noise amplitude (the parameter ). For the case without drift and with the linear drift, the asymptotic formula is the same as for the additive noise, i.e. the dependence on does not appear sro ; sro2 . Then the variance is always infinite.

The difference between both interpretations of the stochastic integral is also visible in the problem of escape from the potential well. This problem was studied numerically: MFPT was calculated, as a function of and . The effective potential, which includes the variable diffusion coefficient in the Stratonovich interpretation, possesses a high barrier when is negative. As a consequence, MFPT rapidly falls with . This effect is not observed in the Itô case: MFPT falls with according to a power-law. Moreover, MFPT rises with in both interpretations. The above conclusions are valid only if the relative size of the system is large enough to allow the long tails of the Lévy distribution to manifest themselves. It was ensured in the calculations by taking a small value of the noise parameter .

Both analytical and numerical calculations for the case of the Stratonovich interpretation were performed by using the statement that rules of the ordinary calculus apply and change of variables is possible. That statement is exact if the variance is finite, in particular for the truncated distribution. Otherwise, the Langevin equation in the transformed variables, Eq.(5), offers only an approximation to Eq.(1) since for the case of Lévy stable processes those equations are not strictly equivalent. The approximation is quite accurate but one can also encounter qualitative differences. We demonstrated, by considering the case of the linear noise, that the stochastic variable may change its sign, which is forbidden for the case of the normal distribution or if the cut-off is present. A possibility to use Eq.(5) is of great practical importance. It enables us not only to perform analytical calculations but also offers a simple numerical tool of much higher precision than the direct integration of Eq.(1).

APPENDIX

In the Appendix, we present properties of the Fox functions which are used in Sec.III. The multiplication rule

| (A7) |

where , allows us to evaluate products involving algebraic terms. The cosine Fourier transform is given by the following expression

| (A14) |

Numerical values of the Fox function can be obtained by means of the following series expansion

| (A18) |

where . The asymptotic expansion results from the property:

| (A25) |

References

- (1) N. G. van Kampen, J. Stat. Phys. 24, 175 (1981).

- (2) A. Schenzle and H. Brand, Phys. Rev. A 20, 1628 (1979).

- (3) B. J. West and W. Deering, Phys. Rep. 246, 1 (1994).

- (4) J.-P. Bouchaud and A. Georges, Phys. Rep. 195, 127 (1990).

- (5) A. Cartea and D. del-Castillo-Negrete, Physica A 374, 749 (2007).

- (6) R. N. Mantegna and H. E. Stanley, J. Stat. Phys. 89, 469 (1997).

- (7) P. Santini, Phys. Rev. E 61, 93 (2000).

- (8) D. Brockmann and T. Geisel, Phys. Rev. Lett. 90, 170601 (2003).

- (9) P. Garbaczewski and V. Stephanovich, Phys. Rev. E 80, 031113 (2009).

- (10) C. W. Gardiner, Handbook of Stochastic Methods for Physics, Chemistry and the Natural Sciences (Springer-Verlag, Berlin, 1985).

- (11) Z. Schuss, Theory and Applications of Stochastic Differential Equations (John Wiley & Sons, New York, 1980).

- (12) T. Srokowski, Phys. Rev. E 80, 051113 (2009).

- (13) T. Srokowski, Phys. Rev. E 79, 040104(R) (2009).

- (14) R. N. Mantegna and H. E. Stanley, Phys. Rev. Lett. 73, 2946 (1994).

- (15) I. Koponen, Phys. Rev. E 52 1197 (1995).

- (16) T. Srokowski, Physica A 388, 1057 (2009).

- (17) M. F. Shlesinger and M. Coplan, J. Stat. Phys. 52, 1423 (1988).

- (18) J. Atchison and J. C. Brown, The Lognormal Distribution (Cabridge U Press, New York, 1963).

- (19) M. F. Shlesinger and B. J. West, in: Random Fluctuations and Pattern Growth: Experiments and Models (Kluwer Academic Publishers, Boston, 1988), p.320.

- (20) A. J. Lichtenberg and M. A. Lieberman, Regular and Chaotic Dynamics (Springer, Heidelberg-New York, 1992).

- (21) A. M. Mathai and R. K. Saxena, The -function with Applications in Statistics and Other Disciplines (Wiley Eastern Ltd., New Delhi, 1978).

- (22) H. M. Srivastava, K. C. Gupta, and S. P. Goyal, The -functions of one and two variables with applications (South Asian Publishers, New Delhi, 1982).

- (23) W. R. Schneider, in Stochastic Processes in Classical and Quantum Systems, Lecture Notes in Physics, edited by S. Albeverio, G. Casati, D. Merlini (Springer, Berlin, 1986), Vol. 262.

- (24) A. Chechkin, V. Gonchar, J. Klafter, R. Metzler, and L. Tanatarov, Chem. Phys. 284, 233 (2002). The method used in this paper is applicable also to the problem of multiplicative noise if is an odd integer.

- (25) A. Janicki and A. Weron, Simulation and Chaotic Behavior of -Stable Stochastic Processes (Marcel Dekker, New York, 1994).

- (26) A. Ralston, A First Course in Numerical Analysis (McGraw-Hill Book Company, New York, 1965).

- (27) P. Hänggi, P. Talkner, and M. Borkovec, Rev. Mod. Phys. 62, 251 (1990).

- (28) A. Wozinski and J. Iwaniszewski, Phys. Rev. E 80, 011129 (2009).

- (29) L. Gammaitoni, F. Marchesoni, E. Menichella-Saetta, and S. Santucci, Phys. Rev. E 49, 4878 (1994).

- (30) P. D. Ditlevsen, Phys. Rev. E 60, 172 (1999).

- (31) B. Dybiec, E. Gudowska-Nowak, and P. Hänggi, Phys. Rev. E 75, 021109 (2007).

- (32) B. Dybiec, Phys. Rev. E 80, 041111 (2009).