Robustness and accuracy of methods for high dimensional data analysis based on Student’s statistic

Aurore Delaigle1,2 Peter Hall1,3 and Jiashun Jin4

1 Department of Mathematics and Statistics, University of Melbourne, VIC 3010, Australia.

2 Department of Mathematics, University of Bristol, Bristol BS8 1TW, UK.

3 Department of Statistics, University of California at Davis, Davis, CA 95616, USA.

4 Department of Statistics, Carnegie Mellon University, Pittsburgh, PA 15213, USA

Abstract: Student’s statistic is finding applications today that were never envisaged when it was introduced more than a century ago. Many of these applications rely on properties, for example robustness against heavy tailed sampling distributions, that were not explicitly considered until relatively recently. In this paper we explore these features of the statistic in the context of its application to very high dimensional problems, including feature selection and ranking, highly multiple hypothesis testing, and sparse, high dimensional signal detection. Robustness properties of the -ratio are highlighted, and it is established that those properties are preserved under applications of the bootstrap. In particular, bootstrap methods correct for skewness, and therefore lead to second-order accuracy, even in the extreme tails. Indeed, it is shown that the bootstrap, and also the more popular but less accurate -distribution and normal approximations, are more effective in the tails than towards the middle of the distribution. These properties motivate new methods, for example bootstrap-based techniques for signal detection, that confine attention to the significant tail of a statistic.

Keywords: Bootstrap, central limit theorem, classification, dimension reduction, higher criticism, large deviation probability, moderate deviation probability, ranking, second order accuracy, skewness, tail probability, variable selection.

AMS SUBJECT CLASSIFICATION. Primary 62G32; Secondary 62F30, 62G90, 62H15, 62H30

Short title. Student’s statistic

1 Introduction

Modern high-throughput devices generate data in abundance. Gene microarrays comprise an iconic example; there, each subject is automatically measured on thousands or tens of thousands of standard features. What has not changed, however, is the difficulty of recruiting new subjects, with the number of the latter remaining in the tens or low hundreds. This is the context of so-called “ problems,” where denotes the number of features, or the dimension, and is the number of subjects, or the sample size.

For each feature the measurements across different subjects comprise samples from potentially different underlying distributions, and can have quite different scales and be highly skewed and heavy tailed. In order to standardise for scale, a conventional approach today is to use -statistics, which, by virtue of the central limit theorem, are approximately normally distributed when is large. W. S. Gosset, when he introduced the Studentised -statistic more than a century ago (Student, 1908), saw that quantity as having principally the virtue of scale invariance. In more recent times, however, other noteworthy advantages of Studentising have been discovered. In particular, the statistic’s high degree of robustness against heavy-tailed data has been quantified. For example, Giné, Götze and Mason (1997) have shown that a necessary and sufficient condition for the Studentised mean to have a limiting standard normal distribution is that the sampled distribution lie in the domain of attraction of the normal law. This condition does not require the sampled data to have finite variance. Moreover, the rate of convergence of the Studentised mean to normality is strictly faster than that for the conventional mean, normalised by its theoretical (rather than empirical) standard deviation, in cases where the second moment is only just finite (Hall and Wang, 2004). Contrary to the case of the conventional mean, its Studentised form admits accurate large deviation approximations in heavy-tailed cases where the sampling distribution has only a small number of finite moments (Shao, 1999).

All these properties are direct consequences of the advantages conferred by dividing the sample mean, , by the sample standard deviation, . Erratic fluctuations in tend to be cancelled, or at least dampened, by those of , much more so than if were replaced by the true standard deviation of the population from which the data were drawn.

The robustness of the -statistic is particularly useful in high dimensional data analysis, where the signal of interest is frequently found to be sparse. For any given problem (e.g. classification, prediction, multiple testing), only a small fraction of the automatically measured features are relevant. However the locations of the useful features are unknown, and we must separate them empirically from an overwhelmingly large number of more useless ones. Sparsity gives rise to a shift of interest away from problems involving vectors of conventional size to those involving high dimensional data.

As a result, a careful study of moderate and large deviations of the Studentised ratio is indispensable to understanding even common procedures for analysing high dimensional data, such as ranking methods based on -statistics, or their applications to highly multiple hypothesis testing. See, for example, Benjamini and Hochberg (1995), Pigeot (2000), Finner and Roters (2002), Kesselman et al. (2002), Dudoit et al. (2003), Bernhard et al. (2004), Genovese and Wasserman (2004), Lehmann et al. (2005), Donoho and Jin (2006), Sarkar (2006), Jin and Cai (2007), Wu (2008), Cai and Jin (2010) and Kulinskaya (2009). The same issues arise in the case of methods for signal detection, for example those based on Student’s versions of higher criticism; see Donoho and Jin (2004), Jin (2007) and Delaigle and Hall (2009). Work in the context of multiple hypothesis testing includes that of Lang and Secic (1997, p. 63), Tamhane and Dunnett (1999), Takada et al. (2001), David et al. (2005), Fan et al. (2007) and Clarke and Hall (2009).

In the present paper we explore moderate and large deviations of the Studentised ratio in a variety of high dimensional settings. Our results reveal several advantages of Studentising. We show that the bootstrap can be particularly effective in relieving skewness in the extreme tails. Attractive properties of the bootstrap for multiple hypothesis testing were apparently first noted by Hall (1990), although in the case of the mean rather than its Studentised form.

Section 2.1 draws together several known results in the literature in order to demonstrate the robustness of the ratio in the context of high level exceedences. Sections 2.2 and 2.3 show that, even for extreme values of the ratio, the bootstrap captures particularly well the influence that departure from normality has on tail probabilities. We treat cases where the probability of exceedence is either polynomially or exponentially small. Section 2.4 shows how these properties can be applied to high dimensional problems, involving potential exceedences of high levels by many different feature components. One example of this type is the use of -ratios to implement higher criticism methods, including their application to classification problems. This type of methodology is taken up in section 3. The conclusions drawn in sections 2 and 3 are illustrated numerically in section 4, the underpinning theoretical arguments are summarised in section 5, and detailed arguments are given by Delaigle et al. (2010).

2 Main conclusions and theoretical properties

2.1 Advantages and drawbacks of studentising in the normal approximation

Let denote independent univariate random variables all distributed as , with unit variance and zero mean, and suppose we want to test against . Two common test statistics for this problem are the standardised mean and the Studentised mean , defined by and where

| (2.1) |

denote the sample mean and sample variance, respectively, computed from the dataset .

In practice, experience with the context often suggests the standardisation that defines . Although both and are asymptotically normally distributed, dividing by the sample standard deviation introduces a degree of extra noise which can make itself felt in terms of greater impact of skewness. However, we shall show that, compared to the normal approximation to the distribution of , the normal approximation to the distribution of is valid under much less restrictive conditions on the tails of the distribution of .

These properties will be established by exploring the relative accuracies of normal approximations to the probabilities and , as increases, and the conditions for validity of those approximations. This approach reflects important applications in problems such as multiple hypothesis testing, and classification or ranking involving high dimensional data, since there it is necessary to assess the relevance, or statistical significance, of large values of sample means.

We start by showing that the normal approximation is substantially more robust for than it is for . To derive the results, note that if

| (2.2) |

then the normal approximation to the probability is accurate, in relative terms, for almost as large as . In particular, as , uniformly in values of that satisfy , for any positive sequence that converges to zero (Shao, 1999). This level of accuracy applies also to the normal approximation to the distribution of the nonstudentised mean, , except that we must impose a condition much more severe than (2.2). In particular, , uniformly in , for each fixed , if and only if

| (2.3) |

see Linnik (1961). Condition (2.3), which requires exponentially light tails and implies that all moments of are finite, is much more severe than (2.2).

Although dividing by the sample standard deviation confers robustness, it also introduces a degree of extra noise. To quantify deleterious effects of Studentising we note that

| (2.4) | ||||

| (2.5) |

uniformly in satisfying , for a sequence , and where is the standard normal distribution function and (Shao, 1999; Petrov, 1975, Chap. 8). (Property (2.2) is sufficient for (2.4) if and as , and (2.5) holds, for the same range of values of , provided that, for some , .) Thus it can be seen that, if and is small, the relative error of the normal approximation to the distribution of is approximately twice that of the approximation to the distribution of .

Of course, Student’s distribution with or degrees of freedom is identical to the distribution of when is normal N, and therefore relates to the case of zero skewness. Taking in (2.4) we see that, when has Student’s distribution with or degrees of freedom, we have . It can be deduced that the results derived in (2.4) and (2.5) continue to hold if we replace the role of the normal distribution by that of Student’s distribution with or degrees of freedom. Similarly, the results on robustness hold if we replace the role of the normal distribution by that of Student’s distribution. Thus, approximating the distributions of and by that of a Student’s distribution, as is sometimes done in practice, instead of that of a normal distribution, does not alter our conclusions. In particular, even if we use the Student’s distribution, is still more robust against heavy tailedness than , and in cases where the Student approximation is valid, this approximation is slightly more accurate for than it is for .

2.2 Correcting skewness using the bootstrap

The arguments in section 2.1 show clearly that is considerably more robust than against heavy-tailed distributions, arguably making the test statistic of choice even if the population variance is known. However, as also shown in section 2.1, this added robustness comes at the expense of a slight loss of accuracy in the approximation. For example, in (2.4) and (2.5) the main errors that arise in normal (or Student’s ) approximations to the distributions of are the result of uncorrected skewness. In the present section we show that if we instead approximate the distribution of using the bootstrap then those errors can be quite successully removed. Similar arguments can be employed to show that a bootstrap approximation to the distribution of is less affected by skewness than a normal approximation. However, as for the normal approximation, the latter bootstrap approximation is only valid if the distribution of is very light tailed. Therefore, even if we use the bootstrap approximation, remains the statistic of choice.

Let denote a resample drawn by sampling randomly, with replacement, from , and put

| (2.6) |

The bootstrap approximation to the distribution function is , and the bootstrap approximation to the quantile is

| (2.7) |

Theorem 1, below, addresses the effectiveness of these approximations for large values of .

As usual in hypothesis testing problems, to calculate the level of the test we take a generic variable that has the distribution of the test statistic and we calculate the probability that the generic variable is larger than the estimated quantile. This generic variable is independent of the sample, and since the quantile of the bootstrap test is random and constructed from the sample then, to avoid confusion, we should arguably use different notations for and the generic variable. However, to simplify notation we keep using for a generic random variable distributed like . This means that we write the level of the test as , but here denotes a generic random variable independent of the sample, whereas denotes the random variable defined at (2.7) and calculated from the sample. In particular, here is independent of .

Define , and write for the probability measure when is drawn from the population with distribution function . Here we highlight the dependence of the probabilities on because we shall use the results in subsequent sections where a clear distinction of the distribution will be required.

Theorem 1.

For each and there exists , increasing no faster than linearly in as the latter increases, such that

| (2.8) |

as , uniformly in all distributions of the random variable such that , and , and in all satisfying .

The assumption in Theorem 1 that serves to determine scale, without which the additional condition would not be meaningful for the very large class of functions considered in the theorem. The theorem can be deduced by taking in Theorem B in section 5.1, and shows that using the bootstrap to approximate the distribution of removes the main effects of skewness. To appreciate why, note that if we were to use the normal approximation to the distribution of we would obtain, instead of (2.8), the following result, which can be deduced from Theorem A in section 5.1 for each such that and :

| (2.9) |

Comparing (2.8) and (2.9) we see that the bootstrap approximation has removed the skewness term that describes first-order inaccuracies of the standard normal approximation.

The size of the remainder in (2.8) is important if we wish to use the bootstrap approximation in the context of detecting weak signals, or of hypothesis testing for a given level of family-wise error rate or false discovery rate among populations or features. (Here and below it is convenient to take to be a function of , which we treat as the main asymptotic parameter.) In all these cases we generally wish to take of size , in the sense that is bounded away from zero and infinity as . This property entails , and therefore Theorem 1 implies that the tail condition , for some , is sufficient for it to be true that “ for and uniformly in the class of distributions of for which , and .”

On the other hand, if, as in Fan and Lv (2008), is exponentially large as a function of , then we require a finite exponential moment of . The following theorem addresses this case. In the theorem, unless , in which case . The proof of the theorem is given in section 5.2.

Theorem 2.

For each and there exists , increasing no faster than linearly in as the latter increases, such that

| (2.10) |

as , uniformly in all distributions of the random variable such that (where ), and , and in all satisfying .

Theorem 2 allows us to repeat all the remarks made in connection with Theorem 1 but in the case where is exponentially large as a function of . Of course, we need to assume that exponential moments of are finite, but in return we can control a variety of statistical methodologies, such as sparse signal recovery or false discovery rate, for an exponentially large number of potential signals or tests. Distributions with finite exponential moments include exponential families and distributions of variables supported on a compact domain. Note that our condition is still less restrictive than assuming that the distribution is normal, as is done in many papers treating high dimensional problems, such as for example Fan and Lv (2008).

2.3 Effect of a nonzero mean on the properties discussed in section 2.2

We have shown that, in a variety of problems, when making inference on a mean it is preferable to use the Studentised mean rather than the standardised mean. We have also shown that, when the skewness of the distribution of is non zero, the level of the test based on the Studentised mean is better approximated when using the bootstrap than when using a normal distribution. Our next task is to check that, when is not true, the probability of rejecting is not much affected by the bootstrap approximation. Our development is notationally simpler if we continue to assume that and , and consider the test with a scalar that potentially depends on but which does not converge to zero. We define

| (2.11) |

Here we take of magnitude because this represents the limiting case where inference is possible. Indeed, a population with mean of order could not be distinguished from a population with mean zero. Thus we treat the statistically most challenging problem.

Our aim is to show that the probability is well approximated by , where and is given by (2.7), and when and are computed from independent data. We claim that in this setting the results discussed in section 2.2 continue to hold. In particular, versions of (2.8) and (2.10) in the present setting are:

| (2.12) |

where denotes skewness and the remainder term has either the form in (2.8) or that in (2.10), depending on whether we assume existence of polynomial or exponential moments, respectively. In particular, if we take then (2.12) holds uniformly in all distributions of the random variable such that , and , and in all satisfying , provided that is sufficiently large; and in the same sense, but with where , (2.12) holds if we replace the assumption by , provided that is sufficiently large. (We require only if .) Result (2.12) is derived in section 5.3. Hence to first order, the probability of rejecting when is not true is not affected by the bootstrap approximation. In particular, to first order, skewness does not affect the approximation any more than it would if were true (compare with (2.8) and (2.10)).

An alternative form of (2.12), which is useful in applications (e.g. in section 3), is to express the right hand side there more explicitly in terms of . This can be done if we note that, in view of Theorem A in section 5.1,

| (2.13) |

where has the same interpretation as in Theorem A, and the last identity follows from the definition of . Combining this property with (2.12) it can be shown that

| (2.14) |

where satisfies the properties given below (2.12).

2.4 Relationships among many events

So far we have treated only an individual event (i.e. a single univariate test), exploring its likelihood. However, since our results for a single event apply uniformly over many choices of the distribution of then we can develop properties in the context of many events, and thus for simultaneous tests. The simplest case is that where the values of are independent; that is, we observe for , where are constants and the random variables are, for different values , computed from independent datasets. We assume that is defined as at (2.11) but with . We could take the values of to depend on , and in fact the theoretical discussion below remains valid provided that , for positive constants and , as increases. (Recall that is the main asymptotic parameter, and is interpreted as a function of .) As in the case of a single event, treated in Theorems 1 and 2, it is important that the -statistic and the corresponding quantile estimator be independent for each . However, as noted in section 2.2, this is not a problem since represents a generic random variable, and only is calculated from the sample.

Under the assumption that the variables and , for , are totally independent we can deduce from (2.12) that, uniformly in satisfying ,

where, for each , denotes either or , and

| (2.15) |

if represents , otherwise, denotes the skewness of the th population, and the remainder terms have the properties ascribed to in section 2.3.

It is often unnecessary to assume, as above, that the quantile estimators are independent of one another. To indicate why, we note that the method for deriving expansions such as (2.8), (2.10) and (2.12) involves computing by first calculating the conditional probability , where the independence of and is used. Versions of this argument can be given for the case of short-range dependence among many different values of , for . However a simpler approach, giving a larger but still asymptotically negligible bound to the remainder term on the right-hand side of (2.15), can be developed more simply; for brevity we do not give details here.

Cases where the statistics are computed from weakly dependent data can be addressed using results of Hall and Wang (2010). That work treats instances where the variables are computed from the first components in respective data streams , with being independent and identically distributed but correlated between streams. As in the discussion above, since we are treating -statistics then it can be assumed without loss of generality that the variables in each data stream have unit variance. (This condition serves only to standardise scale, and in particular places the means on the same scale for each .) Assuming this is the case, we shall suppose too that third moments are uniformly bounded. Under these conditions it is shown by Hall and Wang (2010) that, provided that (a) the correlations are bounded away from 1, (b) the streams are -dependent for some fixed , (c) is bounded between two constant multiples of , (d) , and (e) for we have , where as ; and excepting realisations that arise with probability no greater than , where ; the -statistics can be considered to be independent. In particular, it can be stated that with probability there are no clusters of level exceedences caused by dependence among the data streams.

These conditions, especially (d), permit the dimension to be exponentially large as a function of . Assumption (e) is of interest; without it the result can fail and clustering can occur. To appreciate why, consider cases where the data streams are -dependent but in the degenerate sense that for . Then, for relatively large values of , the value of is well approximated by that of , where is the empirical variance computed from the first data in the stream . It follows that, for any , the values of , for , are also very close to one another. Clearly this can lead to data clustering that is not described accurately by asserting independence.

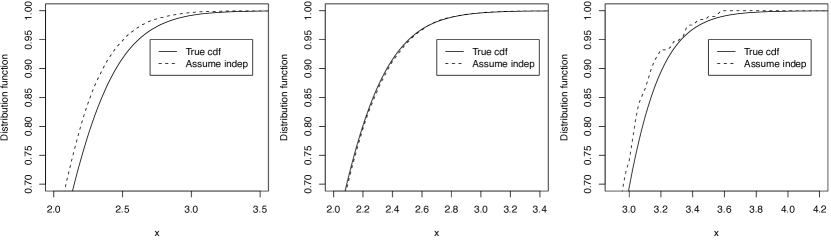

To illustrate these properties we calculated the joint distribution of for short-range dependent -vectors , and compared this distribution with the product of the distributions of the univariate components , . For we took and . Here, is a constant and denote i.i.d. random variables. Figure 1 depicts the resulting distribution functions for several values of and , when the sample size was and the s were from a standardised Pareto(5,5) distribution. We see that the independence assumption gives a good approximation to the joint cumulative distribution function, but, unsurprisingly, the approximation degrades as (and thus the dependence) increases. The figure also suggests that the independence approximation degrades as becomes very large (, in this example).

3 Application to higher criticism for detecting sparse signals in non-Gaussian noise

In this section we develop higher criticism methods where the critical points are based on bootstrap approximations to distributions of statistics, and show that the advantages established in section 2 for bootstrap methods carry over to sparse signal detection.

Assume we observe , for , where all the observations are independent and where, for each , are identically distributed. For example, in gene microarray analysis if often used to represent the log-intensity associated with the th subject and the th gene, represents the mean expression level associated with the th feature (i.e. gene), and the s represent measurement noise. The distributions of the s are completely unknown, and we allow the distributions to differ among components. Let . The problem of signal detection is to test

| (3.1) |

For simplicity, in this section we assume that each , but a similar treatment can be given where nonzero s have different signs.

To perform the signal detection test we use the ideas in section 2 to construct a bootstrap higher criticism statistic that can be calculated when the distribution of the data is unknown, and which is robust against heavy-tailedness of this distribution. (Higher criticism was originally suggested by Donoho and Jin (2004) in cases where the centered data have a known distribution, non-Studentised means were used, and the bootstrap was not employed.) As in section 2.4, let be the Studentised statistic for the the th component, and let be the bootstrap estimator of the quantile of the distribution of , both calculated from the data . We suggest the following bootstrap higher criticism statistic:

| (3.2) |

where is small enough for the statistic at (3.2) to depend only on indices for which is relatively large. This exploits the excellent performance of bootstrap approximation to the distribution of the Studentised mean in the tails, as exemplified by Theorems 1 and 2 in section 2, while avoiding the “body” of the distribution, where the bootstrap approximations are sometimes less remarkable. We reject if is too large.

We could have defined the higher criticism statistic by replacing the bootstrap quantiles in definition (3.2) by the respective quantiles of the standard normal distribution. However, the greater accuracy of bootstrap quantiles compared to normal quantiles, established in section 2, suggest that in the higher criticism context, too, better performance can be obtained when using bootstrap quantiles. The superiority of the bootstrap approach will be illustrated numerically in section 4.

Theorem 3 below provides upper and lower bounds for the bootstrap higher criticism statistic at (3.2), under and . We shall use these results to prove that the probabilities of type I and type II errors converge to zero as . The standard “test pattern” for assessing higher criticism is a sparse signal, with the same strength at each location where it is nonzero. It is standard to take for all but a fraction of s, and elsewhere, where is chosen to make the testing problem difficult but solvable. As usual in the higher criticism context we take

| (3.3) |

where is a fixed parameter. Among these values of the range is the least interesting, because there the proportion of nonzero signals is so high that it is possible to estimate the signal with reasonable accuracy, rather than just determine its existence. See Donoho and Jin (2004). Therefore we focus on the most interesting range, which is . For the most interesting values of are , with . Taking would render the two hypotheses indistinguishable, whereas taking would render the signal relatively easy to discover, since it would imply that the means that are nonzero are of the same size as, or larger than, the largest values of the signal-free s. In light of this we consider nonzero means of size

| (3.4) |

where is a fixed parameter.

Before stating the theorem we introduce notation. Let be a generic multi-log term which may be different from one occurrence to the other, and is such that for any constant , and as . We also define the “phase function” by

In the - plane we partition the region into three subregions (i), (ii), and (iii) defined by , , and , respectively. The next theorem, derived in the longer version of this paper (Delaigle et al., 2010), provides upper and lower bounds for the bootstrap higher criticism statistic under and , respectively.

Theorem 3.

Let , where is fixed, and suppose that, for each , the distribution of the respective satisfies , and , where is chosen so large that (2.8) holds with . Also, take . Then

(a) Under the null hypothesis in (3.1), there is a constant such that

It follows from the theorem that, if we set the test so as to reject the null hypothesis if and only if , where as , and where , then as long as , the probabilities of type I and type II errors tend to zero as (note that ).

It is also of interest to see what happens when , and below we treat separately the cases and , where is the standard phase function discussed by Donoho and Jin (2004). We start with the case . There, Ingster (1999) and Donoho and Jin (2004) proved that for the sizes of and that we consider in (3.3)–(3.4), even when the underlying distribution of the noise is known to be the standard normal, the sum of the probabilities of type I and type II errors of any test tends to as . See also Ingster (2001). Since our testing problem is more difficult than this (in our case the underlying distribution of the noise is estimated from data), in this context too, asymptotically, any test fails if .

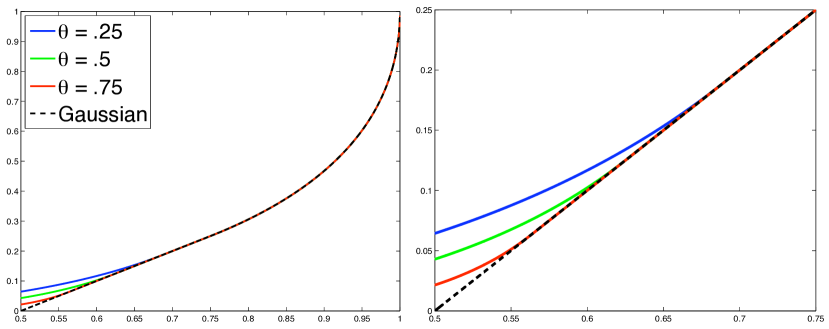

It remains to consider the case . In the Gaussian model, i.e. when the underlying distribution of the noise is known to be standard normal, it was proved by Donoho and Jin (2004) that there is a higher critisicism test for which the sum of the probabilities of type I and type II errors tends to as . However, our study does not permit us to conclude that bootstrap higher criticism will yield a successful test. The reasons for the possible failure of higher criticism are two-fold: the sample size, , is relatively small, and we do not have full knowledge of the underlying distribution of the background noise. See Figure 2 for a comparison of the two curves and .

The case where is exponentially large (i.e. for some constant ) can be interpreted as the case , where reduces to . In this case, if then the sum of probabilities of type I and type II errors of tends to as tends to . The proof is similar to that of Theorem 3 so we omit it.

4 Numerical properties

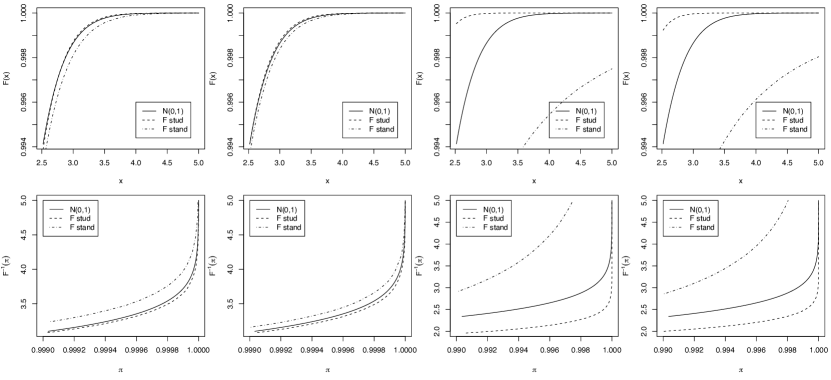

First we give numerical illustrations of the results in section 2.1. In Figure 3 we compare the right tail of the cumulative distribution functions of and with the right tail of , denoting the standard normal distribution function, when has increasingly heavy tails. We take where (moderate tails) or (heavier tails), with . The figure shows that approximates the distribution of better than it approximates that of , and that the approximation of the normal distribution of degrades as the distribution of becomes more heavy-tailed. The figure also compares the right tail of the inverse cumulative distribution functions, which shows that the normal approximation is more accurate in the tails for than for . Unsurprisingly, as the sample size increases the normal approximation for both and becomes more accurate.

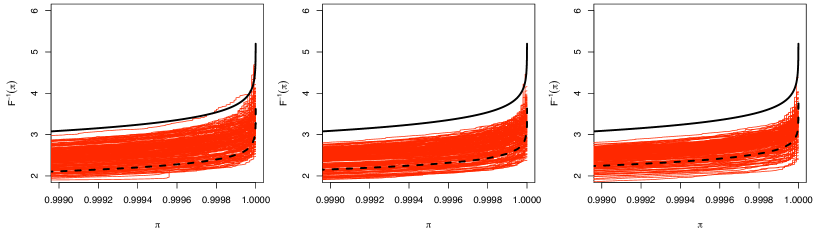

Next we illustrate the results in section 2.2. There we showed that although is more robust than against heavy-tailedness of the distribution of , the distribution of is somewhat more affected by the skewness of . To illustrate the success of bootstrap in correcting this problem we compare the bootstrap and normal approximations for several skewed and heavy-tailed distributions. In particular, Figure 4 shows results obtained when , with . Since, later in this section, we shall be more interested in approximating quantiles of the distribution of , rather than the distribution itself, then in Figure 4 we show the right tail of the inverse cumulative distribution function of and 200 bootstrap estimators of this tail obtained from 200 samples of sizes , or simulated from . We also show the inverse cumulative distribution function of the standard normal distribution. The figure demonstrates clearly that the bootstrap approximation to the tail is more accurate than the normal approximation, and that the approximation improves as the sample size increases. We experimented with other skewed and heavy-tailed distributions, such as other F distributions and several Pareto ditributions, and reached similar conclusions.

Note that, when implementing the bootstrap, the number of bootstrap samples has to be taken sufficiently large to obtain reasonably accurate estimators of the tails of the distribution. In general, the larger , the more accurate the bootstrap approximation, but in practice we are limited by the capacity of the computer. To obtain a reasonable approximation of the tail up to the quantile , where , we found that one should take no less than .

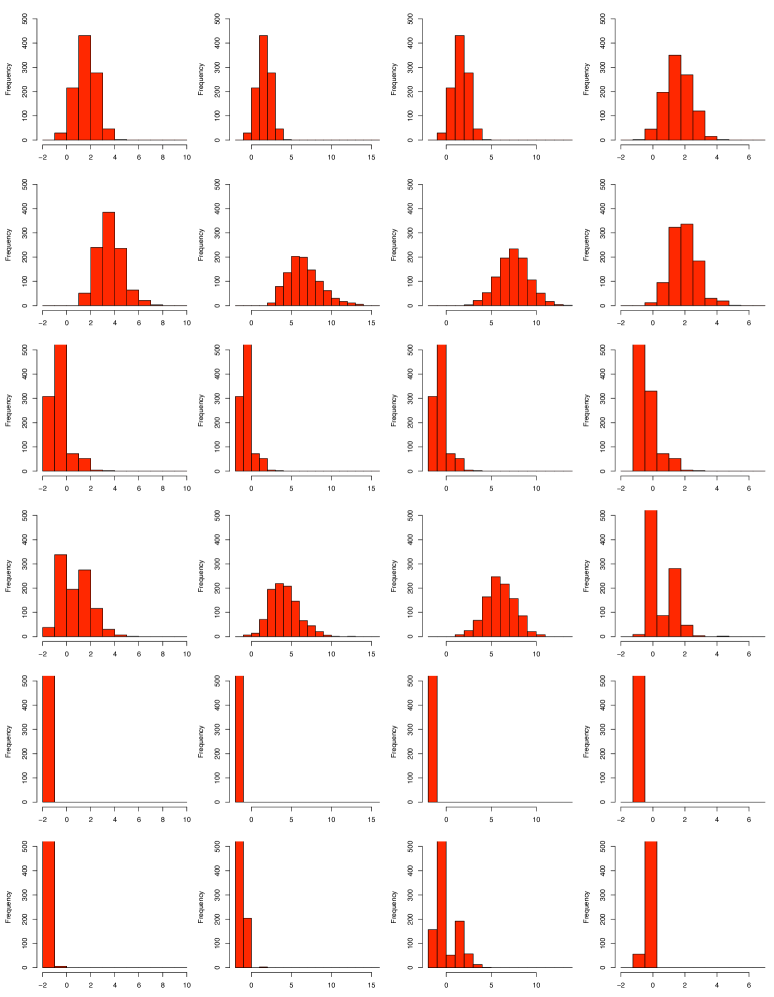

Let and denote, respectively, the theoretical and the normal versions of the higher criticism statistic, defined by the formula at the right hand side of (3.2), replacing there the bootstrap quantiles by and , respectively, where denote the theoretical quantiles of and denote the quantile of the standard normal distribution. To illustrate the success of bootstrap in applications of the higher criticism statistic, in our simulations we compared the statistic which we could use if we knew the distribution , the bootstrap statistic defined at (3.2), where the unknown quantiles are estimated as the bootstrap quantities as discussed in the previous paragraph, and the normal version . We constructed histograms of these three versions of the higher criticism statistic, obtained from 1000 simulated values calculated under or an alternative hypothesis. For any of the three versions, to obtain the 1000 values we generated 1000 samples of size , of -vectors . We did this under , where the mean of each was zero, and under various alternatives , where we set a fraction of these means equal to , with . As in section 3 we took , and , where we chose and to be on the frontier of the .

Figure 5 shows the histograms under and under various alternatives located on the frontier (, for , , and ), when the ’s are standardised variables, and . We can see that the histogram approximations to the density of the bootstrap are relatively close to the histogram approximations to the density of . By contrast, the histograms in the case of show that the distribution of is a poor approximation to the distribution of , reflecting the inaccuracy of normal quantiles as approximations to the quantiles of heavy-tailed, skewed distributions. We also see that, except when , the histograms for and under are rather well separated from those under . This illustrates the potential success of higher criticism for distinguishing between and . By contrast, this property is much less true for .

We also compared histograms for other heavy-tailed and skewed distribution, such as the Pareto, and reached similar conclusions. Furthermore, we considered skewed but less-heavy tailed distributions, such as the chi-squared(10) distribution. There too we obtained similar results, but, while the bootstrap remained the best approximation, the normal approximation performed better than in heavy-tailed cases. We also considered values of further away from the frontier, and, unsurprisingly since the detection problem became easier, the histograms under became even more separated from those under .

5 Technical arguments

5.1 Preliminaries

Let be as in (2.11). Then the following result can be proved using arguments of Wang and Hall (2009).

Theorem A.

Let denote a constant. Then,

| (5.1) |

as , where the function is bounded in absolute value by a finite, positive constant (depending only on ), uniformly in all distributions of for which , and , and uniformly in and satisfying and , where .

We shall employ Theorem A to prove the theorem below. Details are given in a longer version of this paper (Delaigle et al., 2010). Take to be any subset of the class of distributions of the random variable , such that for some and a constant , and . Recall the definition of in (2.6), let and denote the respective solutions of and , and recall that . Take , and let and denote independent random variables with the specified marginal distributions.

Theorem B.

Let denote a constant. Then,

| (5.2) |

as , uniformly in all and in all and satisfying and , where .

5.2 Proof of Theorem 2

The following theorem can be derived from results of Adamczak (2008).

Theorem C.

If are independent and identically distributed random variables with zero mean, unit variance and satisfying

| (5.3) |

for all , where , then for each there exist constants , depending only on , , and , such that for all ,

We use Theorem C to bound the remainder terms in Theorem B. If and we take for an integer , then (5.3) holds for constants and depending on , and , and with . In particular, for all ,

Taking , 2 or 3, and for some ; or and ; we deduce that in each of these settings,

where decreases to zero as . Therefore the remainder term in (5.2) equals , and so Theorem 2 is implied by Theorem B.

5.3 Proof of (2.12)

Note that, by Theorem B in section 5.1, Theorems 1 and 2 continue to hold if we replace the left-hand sides of (2.8) and (2.10) by , provided we also replace the factor on the right-hand sides by . The uniformity with which (2.8) and (2.10) hold now extends (in view of Theorem B) to such that with , as well as to satisfying .

Acknowledgement

We are grateful to Jianqing Fan and Evarist Giné for helpful discussion.

References

ADAMCZAK, R. (2008). A tail inequality for suprema of unbounded empirical processes with applications to Markov chains. Electron. J. Probab. 13, 1000-1034.

BENJAMINI, Y. AND HOCHBERG, Y. (1995). Controlling the false discovery rate: a practical and powerful approach to multiple testing. J. Roy. Statist. Soc. Ser. B 57, 289–300.

BERNHARD, G., KLEIN, M. AND HOMMEL, G. (2004). Global and multiple test procedures using ordered p-values — a review. Statist. Papers 45, 1–14.

CAI, T. AND JIN, J. (2010). Optimal rate of convergence of estimating the null density and the proportion of non-null effects in large-scale multiple testing. Ann. Statist. 38, 100–145.

CLARKE, S. AND HALL, P. (2009). Robustness of multiple testing procedures against dependence. Ann. Statist. 37, 332–358.

DAVID, J.-P., STRODE, C., VONTAS, J., NIKOU, D., VAUGHAN, A., PIGNATELLI, P.M., LOUIS, P., HEMINGWAY, J. AND RANSON, J. (2005). The Anopheles gambiae detoxification chip: A highly specific microarray to study metabolic-based insecticide resistance in malaria vectors. Proc. Natl. Acad. Sci. 102, 4080–4084.

DELAIGLE, A. AND HALL, P. (2009). Higher criticism in the context of unknown distribution, non-independence and classification. In Perspectives in Mathematical Sciences I: Probability and Statistics, 109–138. Eds N. Sastry, M. Delampady, B. Rajeev and T.S.S.R.K. Rao. World Scientific.

DELAIGLE, A., HALL, P. AND JIN, J. (2010). Robustness and accuracy of methods for high dimensional data analysis based on Student’s statistic–long version.

DONOHO, D.L. AND JIN, J. (2004). Higher criticism for detecting sparse heterogeneous mixtures. Ann. Statist. 32, 962–994.

DONOHO, D.L. AND JIN, J. (2006). Asymptotic minimaxity of false discovery rate thresholding for sparse exponential data. Ann. Statist. 34, 2980-3018.

DUDOIT, S., SHAFFER, J.P. AND BOLDRICK, J.C. (2003). Multiple hypothesis testing in microarray experiments. Statist. Sci. 18, 73–103.

FAN, J., HALL, P. AND YAO, Q. (2007). To how many simultaneous hypothesis tests can normal, Student’s or bootstrap calibration be applied? J. Amer. Statist. Assoc. 102, 1282–1288.

FAN, J. AND LV, J. (2008). Sure independence screening for ultrahigh dimensional feature space (with discussion). J. Roy. Statist. Soc. Ser. B 70, 849–911.

FINNER, H. AND ROTERS, M. (2002). Multiple hypotheses testing and expected number of type I errors. Ann. Statist. 30, 220–238.

GENOVESE, C. AND WASSERMAN, L. (2004). A stochastic process approach to false discovery control. Ann. Statist. 32, 1035–1061.

GINÉ, E., GÖTZE, F. AND MASON, D.M. (1997). When is the Student -statistic asymptotically standard normal? Ann. Probab. 25, 1514–1531. IS IT 2007 OR 1997?

HALL, P. (1990). On the relative performance of bootstrap and Edgeworth approximations of a distribution function. J. Multivariate Anal. 35, 108–129.

HALL, P. AND WANG, Q. (2004). Exact convergence rate and leading term in central limit theorem for Student’s statistic. Ann. Probab. 32, 1419–1437.

HALL, P. AND WANG, Q. (2010). Strong approximations of level exceedences related to multiple hypothesis testing. Bernoulli, to appear.

INGSTER, Yu. I. (1999). Minimax detection of a signal for -balls. Math. Methods Statist. 7, 401–428.

INGSTER, Yu. I. (2001). Adaptive detection of a signal of growing dimension. I. Meeting on Mathematical Statistics. Math. Methods Statist. 10, 395–421.

JIN, J. (2007). Proportion of nonzero normal means: universal oracle equivalences and uniformly consistent estimators. J. Roy. Statist. Soc. Ser. B 70, 461–493.

JIN, J. AND CAI. T. (2007). Estimating the null and the proportion of non-null effects in large-scale multiple comparisons. J. Amer. Statist. Assoc. 102, 496–506.

KESSELMAN, H.J., CRIBBIE, R. AND HOLLAND, B. (2002). Controlling the rate of Type I error over a large set of statistical tests. Brit. J. Math. Statist. Psych. 55, 27–39.

KULINSKAYA, E. (2009). On fuzzy familywise error rate and false discovery rate procedures for discrete distributions. Biometrika 96, 201–211.

LANG, T.A. AND SECIC, M. (1997). How to Report Statistics in Medicine: Annotated Guidelines for Authors. American College of Physicians, Philadelphia.

LEHMANN, E.L., ROMANO, J.P. AND SHAFFER, J.P. (2005). On optimality of stepdown and stepup multiple test procedures. Ann. Statist. 33, 1084–1108.

LINNIK, JU. V. (1961). Limit theorems for sums of independent quantities, taking large deviations into account. I. Teor. Verojatnost. i Primenen 7, 145–163.

PETROV, V.V. (1975). Sums of Independent Random Variables. Springer, Berlin.

PIGEOT, I. (2000). Basic concepts of multiple tests — A survey. Statist. Papers 41, 3–36.

SARKAR, S.K. (2006). False discovery and false nondiscovery rates in single-step multiple testing procedures. Ann. Statist. 34, 394–415.

SHAO, Q.-M. (1999). A Cramér type large deviation result for Student’s -statistic. J. Theoret. Probab. 12, 385–398.

STUDENT (1908). The probable error of a mean. Biometrika 6, 1–25.

TAKADA, T., HASEGAWA, T., OGURA, H., TANAKA, M., YAMADA, H., KOMURA, H. AND ISHII, Y. (2001). Statistical filter for multiple test noise on fMRI. Systems and Computers in Japan 32, 16–24.

TAMHANE, A.C. AND DUNNETT, C.W. (1999). Stepwise multiple test procedures with biometric applications. J. Statist. Plann. Inf. 82, 55–68.

WANG, Q. AND HALL, P. (2009). Relative errors in central limit theorems for Student’s statistic, with applications. Statist. Sinica 19, 343–354.

WU, W.B. (2008). On false discovery control under dependence. Ann. Statist. 36, 364–380.

Appendix A PAGES 5.3–A.2: NOT-FOR-PUBLICATION APPENDIX

A.1 Proof of Theorem B

Step 1: Expansions of and . The main results here are (A.3) and (A.5). To derive them, take to have the distribution of , where is as in (2.1), and, for and 4, put

where . Letting in Theorem A, and taking there to have the distribution of conditional on , we deduce that if is given,

| (A.1) |

where and:

the random function satisfies (where

is the same constant introduced in Theorem A) uniformly in datasets

for which and , and uniformly also in satisfying

.

(A.2)

Properties (A.1) and (A.2) imply that satisfies:

| (A.3) |

where is the solution of and, in the case :

the random function satisfies (where

is a finite, positive constant) uniformly in datasets for which

and , and uniformly also in satisfying

(A.4)

Analogously, Theorem A implies that satisfies:

| (A.5) |

where is the solution of and:

the function satisfies (with denoting

a finite, positive constant) uniformly in distributions of for which

, and , and uniformly also in satisfying .

(A.6)

The derivations of the pairs of properties (A.3) and (A.4), and (A.5) and (A.6), are similar. For example, suppose that if is given by (A.3) rather than by , and that the function in (A.3) is open to choice except that it should satisfy (A.4). If we define , then by (A.1), (A.3) and (A.4),

| (A.7) | ||||

where satisfies (A.4). By judicious choice of , satisfying (A.4), we can ensure that in (A.7) vanishes, up to the level of discreteness of the conditional distribution function of . In this case the right-hand side of (A.7) equals simply , so that indeed has the intended property, i.e. .

Step 2: Expansions of the difference between and . The main results here are (A.10) and (A.11). To obtain them, first combine (A.3) and (A.5) to deduce that:

| (A.8) |

where, for :

the random function satisfies (with

denoting a finite, positive constant) uniformly in datasets for which

and ; uniformly in distributions of for which ,

and ; and uniformly also in satisfying

.

(A.9)

Using (A.5), (A.6), (A.8) and (A.9) we deduce that:

and , where (the latter appearing below) satisfy (A.9). Therefore,

| (A.10) |

Similarly, using (A.5) and (A.8),

| (A.11) |

where, for :

the random function satisfies (with

denoting a finite, positive constant) uniformly in datasets for

which and , uniformly in distributions of for which

, and , and uniformly also in such

that where , and in such that .

(A.12)

Step 3: Initial expansion of . To derive (A.16), the main result in this step, note that by (A.3)–(A.5) and (A.11),

| (A.13) |

| (A.14) |

Reflecting (A.12), let denote the class of distribution functions of such that , and ; write for probability measure when is drawn from the population with distribution function ; let denote any given event, shortly to be defined concisely; let be the intersection of and the events and ; and write for the complement of . In view of (A.15),

| (A.16) |

uniformly in the following sense:

uniformly in , in such that , where , and

in such that .

(A.17)

Step 4: Simplification of right-hand side of (A.16). Here we derive a simple formula, (A.28), for the expectation on the right-hand side of (A.16). That result, when combined with (A.16) and (A.17), leads quickly to Theorem B.

Put , write to denote the event that where and , and put . Observe that

| (A.18) |

From this property it can be proved that if and is sufficiently small, depending only on , then whenever holds. Therefore if holds, and for , and , then

In these circumstances, defining , we have:

| (A.19) |

Note too that if then

whenever and take values in the set

, and are nonnegative, and or 2.

(A.20)

Also, in the same context as (A.20), if then

| (A.21) |

and if and , and is sufficiently small,

| (A.22) |

where . In deriving (A.22) we used the fact that , and that, by Markov’s inequality (employing the fact that and choosing ),

for , where . Therefore,

| (A.23) |

If then an argument similar to that leading to (A.23) shows that

| (A.24) |

Combining (A.20), (A.21), (A.22) and (A.24); using Taylor expansion to derive approximations to , starting from (A.18); noting the definition of given in the previous paragraph; and observing that if with , and ; we deduce that:

| (A.25) |

Using (A.19), (A.23) and (A.25), and choosing to be the least integer such that , we deduce that:

| (A.26) |

uniformly in the following sense:

uniformly in , in such that with , and

in such that ,

(A.27)

where denotes the intersection of (defined at (A.17)) with the class of distributions of such that .

An argument almost identical to that leading to (A.26) and (A.27) shows that the same pair of results holds if we replace by the event that and . The only change needed is the observation that, since entails , is uniformly bounded above by a constant multiple of . This follows from the fact that, if are random variables satisfying , then . Therefore, in the argument in (A.22) we can replace the bound to by the bound to . This means that (A.26) holds if we replace there by the event , i.e. the event introduced just above (A.16). That is,

| (A.28) |

uniformly in the sense of (A.27).

A.2 Proof of Theorem 3

Throughout this proof we use the notation , where denotes the value of stated in the theorem. Also, for two positive sequences and , we write when . We use the equivalent notation .

Fix . Let , and . We have . We introduce a non-stochastic counterpart

of , where and . Note that .

The keys for the proofs are:

- (A)

-

There is a constant such that

- (B)

-

Under , there is a constant such that for sufficiently large .

- (C)

-

Under , .

Combining (A)–(B), there exit constants and such that and . Therefore,

and part (a) of Theorem 3 follows. Combining (A) and (C) gives that

and part (b) of the theorem follows. Note that and may stand for different quantities in different occurrence.

We now show (A)–(C). Below, whenever we refer to , we assume that . By definition, , where the fraction of is under the null and under the alternative. Using Theorem 1 and noting that and that in (2.8), we have

| (A.29) |

It follows that both under the null and under the alternative,

| (A.30) |

As a result, uniformly in ,

| (A.31) |

Consider (A). Note that for any integer and any positive sequences and , . By the definition of and ,

where is stochastic and is deterministic, and

To show (A), it is sufficient to show that both under the null and the alternative,

| (A.32) |

and that

| (A.33) |

Consider (A.32). Note that

| (A.34) |

For each , applying Bennett’s inequality [Shorack and Wellner (1986) page 851] with and ,

| (A.35) |

where is monotonely decreasing in and satisfies for large , and is the average variance of :

On one hand, recall that there is at least a fraction of s that are , and that when , . We see that

| (A.36) |

On the other hand, by Schwartz inequality,

It follows from the definition of that

| (A.37) |

Recalling that is monotonely decreasing, and that for large , it follows from (A.36)–(A.37) that

| (A.38) |

where is a generic constant. Note that the last term in (A.38) . Combining (A.34)–(A.35) and (A.37)–(A.38) gives (A.32).

It remains to prove (A.33). Recall that . By the definition of ,

| (A.39) |

Under the null, by Theorem 1, , which gives the first assertion in (A.33). For the second assertion, write

Noting that , it follows that

| (A.40) |

Combining (A.39) and (A.40) gives the second claim of (A.33).

Consider (B). In this case, the null hypothesis is true and all s equal . By the definition and (A.29)–(A.31),

| (A.41) |

Recalling that with , and the claim follows.

Consider (C). In this case, the alternative hypothesis is true, and a fraction of s is , with the remaining of them equal to . Using (2.13), where ,

| (A.42) |

where is the survival function of a . Combining (A.29) and (A.42),

and it follows from direct calculations that

| (A.43) |

Recall that . First, . This equals because and . Second, . Inserting these into (A.2) gives

and so

| (A.44) |

We now re-parametrize with as

By Mill’s ratio, we have . Recall that , where . We deduce that the range of possible values for the parameter runs from to (with lower order terms neglected). It follows from elementary calculus that

| (A.45) |

Moreover, by Mill’s ratio,

| (A.46) |

where

Inserting (A.46) into (A.45) gives

| (A.47) |

We now analyze as a function of . In region (i), , and is monotonely decreasing in . Therefore, the maximizing value of is , at which . In region (ii), . As ranges between and , first monotonely increases and reaches the maximum at , then monotonely decreases. The maximum of is then . In region (iii), , and is monotonely increasing in . The maximizing value of is , at which . Combining these with (A.47) and (A.44) gives the claim. ∎

References

SHORACK, G.R. AND WELLNER, J.A. (1986). Empirical Process with Application to Statistics. John Wiley & Sons, NY.