Asymptotic Power Utility-Based

Pricing and Hedging111We thank an anonymous referee and an associate editor for their careful reading of the manuscript.

Jan Kallsen222Mathematisches Seminar,

Christian-Albrechts-Universität zu Kiel,

Westring 383,

D–24118 Kiel, Germany,

(e-mail: kallsen@math.uni-kiel.de).

Johannes Muhle-Karbe333Corresponding author. Departement Mathematik,

ETH Zürich,

Rämistrasse 101,

CH–8092 Zürich, Switzerland, and Swiss Finance Institute.

(e-mail: johannes.muhle-karbe@math.ethz.ch). Partially supported by the National Centre of Competence in Research Financial Valuation and Risk Management (NCCR FINRISK), Project D1 (Mathematical Methods in Financial Risk Management), of the Swiss National Science Foundation (SNF). Richard Vierthauer 444Mathematisches Seminar,

Christian-Albrechts-Universität zu Kiel,

Westring 383,

D–24118 Kiel, Germany,

(e-mail: vierthauer@math.uni-kiel.de).

Abstract

Kramkov and Sîrbu [32, 33] have shown that first-order approximations of power utility-based prices and hedging strategies for a small number of claims can be computed by solving a mean-variance hedging problem under a specific equivalent martingale measure and relative to a suitable numeraire. For power utilities, we propose an alternative representation that avoids the change of numeraire. More specifically, we characterize the relevant quantities using semimartingale characteristics similarly as in Černý and Kallsen [6] for mean-variance hedging. These results are illustrated by applying them to exponential Lévy processes and stochastic volatility models of Barndorff-Nielsen and Shephard type [2]. We find that asymptotic utility-based hedges are virtually independent of the investor’s risk aversion. Moreover, the price adjustments compared to the Black-Scholes model turn out to be almost linear in the investor’s risk aversion, and surprisingly small unless very high levels of risk aversion are considered.

In incomplete markets, derivative prices cannot generally be based on perfect

replication. A number of alternatives have been suggested in the literature, relying, e.g.,

on superreplication, mean-variance hedging, calibration of parametric

families, utility-based concepts, or ad-hoc approaches. This paper focuses on utility indifference prices as studied by Hodges and Neuberger [17] and many others. They make sense for over-the-counter trades of a fixed quantity of contingent claims. Suppose that a client approaches a potential seller

in order to buy European-style contingent claims maturing at . The seller is supposed

to be a utility maximizer with given preference structure. She will enter into the contract only if her

maximal expected utility is increased by the trade. The utility indifference price

is the lowest acceptable premium for the seller. If the trade is made, the seller’s optimal

position in the underlyings changes due to the presence of the option. This adjustment in the optimal

portfolio process is called utility-based hedging strategy for the claim. Both

the utility indifference price and the corresponding utility-based hedging strategy are

typically hard to compute even if relatively simple incomplete market models are considered.

A reasonable way out for practical purposes is to consider approximations for small ,

i.e., the limiting structure for small numbers of contingent claims.

Extending earlier work on the limiting price, Kramkov and Sîrbu [32, 33] show that first-order approximations of the utility indifference price and the utility-based hedging strategy

can be expressed in terms of a Galtchouk-Kunita-Watanabe (GKW) decomposition of the

claim after changing both the numeraire and the underlying probability measure.

From a slightly different perspective one may say that

Kramkov and Sîrbu [32, 33]

relate utility indifference pricing and hedging asymptotically to some

mean-variance hedging

problem. In this representation, the -distance between payoff and

terminal wealth of

approximating portfolios needs to be considered relative to both a new

numeraire and a new probability measure.

This differs from related results for exponential utility (see [34, 3, 28]), where no numeraire change is necessary. In the present study, we show that the numeraire change can also be avoided for power utilities, which constitute the most popular and tractable ones on the positive real line, i.e., in the setup of [32, 33]. This allows to examine directly how the dynamics of the underlying change to account for utility-based rather than mean-variance hedging, and also allows to apply directly a number of explicit resp. numerical results from the literature. The key idea is to consider an equivalent mean-variance hedging problem relative to the original numeraire but under yet another probability measure. More specifically, the solution of [32, 33] for a contingent claim corresponds to a quadratic hedging problem of the form

(1.1)

with some numeraire process and some martingale measure .

If we define a new measure via

the mean-variance hedging problem (1.1) can evidently be rewritten as

(1.2)

where we minimize again over some a set of initial endowments and trading strategies . Replacing (1.1) by

(1.2) constitutes the key idea underlying our approach. For a related transition in the quadratic hedging literature compare

[16] with and [42, 39, 6] without numeraire change. Since the stock is not a martingale in the reformulation (1.2), the Galtchouk-Kunita-Watanabe decomposition does not lead to the solution. Instead, representations as in [42] or, more generally, [6] can be used to obtain concrete formulas, which are provided in Theorem 4.7 of this paper. On a rigorous mathematical level, we do not consider mean-variance hedging problems because the expression in Theorem 4.7 is the solution to such a hedging problem only under additional regularity which does not hold in general. Instead, we show in a more direct fashion that the solution of [32, 33] can be expressed as in Theorem 4.7.

In order to illustrate the applicability of our results and shed light on the role of the investor’s risk aversion for power utility-based pricing and hedging, we consider exponential Lévy processes and the stochastic volatility model of Barndorff-Nielsen and Shephard [2] as examples. For these processes, all technical assumptions can be verified directly in terms of the model parameters. Moreover, results for the related mean-variance hedging problem (cf. [18, 5, 27, 30]) can be adapted to obtain first-order approximations to utility-based prices and hedging strategies explicitly up to some numerical integrations. Using parameters estimated from an equity index time series, we find that the asymptotic utility-based hedging strategies are virtually independent of the investor’s risk aversion, which holds exactly for exponential investors. Moreover, the risk premia per option sold turn out to be almost linear in the investor’s (absolute) risk aversion, which again holds exactly for exponential utilities. Hence, these examples suggest very similar pricing and hedging implications of both exponential and power utilities: risk aversion barely influences the optimal hedges, and enters linearly into the first-order risk-premia. Similarly as in [12, 13] in the context of basis risk, we find that the

price adjustments are negligibly small for the levels of risk aversion typically considered in the literature. In particular, surprisingly high levels of risk aversion are needed to obtain bid- and ask prices below and above the Black-Scholes price, respectively.

The remainder of the paper is organized as follows. After briefly recalling the general theory of power utility-based pricing and hedging in Section 2, we review the asymptotic results of Kramkov and Sîrbu [32, 33]. As a byproduct we derive a feedback formula for the utility-based hedging strategy. Subsequently, we develop our alternative representation in Section 4. Throughout, we explain how to apply the general theory to exponential Lévy processes and the stochastic volatility model of Barndorff-Nielsen and Shephard [2]. A concrete numerical example is considered in Section 6. Finally, the appendix summarizes notions and results concerning semimartingale calculus for the convenience of the reader.

Unexplained notation is generally used as in the monograph of Jacod and Shiryaev [21]. In particular, for a semimartingale , we denote by the predictable -integrable processes and by the stochastic integral of with respect to . We write for the stochastic exponential of a semimartingale and denote by the stochastic logarithm of a semimartingale satisfying . For semimartingales and , represents the predictable compensator of , provided that the latter is a special semimartingale (cf. [20, p. 37]). Finally, we write for the Moore-Penrose pseudoinverse of a matrix or matrix-valued process (cf. [1]) and denote by the identity matrix on .

2 Utility-based pricing and hedging

Our mathematical framework for a frictionless market model is as follows. Fix a terminal time and a filtered probability space in the sense of [21, I.1.2]. For ease of exposition, we assume that and up to null sets, i.e., all -measurable random variables are almost surely constant.

We consider a securities market which consists of assets, a bond and stocks. As is common in Mathematical Finance, we work in discounted terms. This means we suppose that the bond has constant value and denote by the discounted price process of the stocks in terms of multiples of the bond. The process is assumed to be an -valued semimartingale.

Example 2.1

1.

Throughout this article, we will illustrate our results by considering one-dimensional exponential Lévy models. This means that and for a constant and a Lévy process with Lévy-Khintchine triplet relative to some truncation function on . We write

for the corresponding Lévy exponent, i.e., the function such that . When considering exponential Lévy models, we will always assume , which is equivalent to resp. the support of being concentrated on .

2.

We will also consider the stochastic volatility model of Barndorff-Nielsen and Shephard [2] (henceforth BNS model). Here and the return process driving is modelled as

for a constant , a standard Brownian motion , and an independent Lévy-driven Ornstein-Uhlenbeck process . The latter is given as the solution to the SDE

with some constant and an increasing Lévy process with Lévy-Khintchine triplet relative to a truncation function on .

Self-financing trading strategies are described by -valued predictable stochastic processes , where denotes the number of shares of security held at time . We consider an investor whose preferences are modelled by a power utility function with constant relative risk aversion . Given an initial endowment , the investor solves the pure investment problem

(2.1)

where the set of admissible strategies for initial endowment is given by

To ensure that the optimization problem (2.1) is well-posed, we make the following two standard assumptions.

Assumption 2.2

There exists an equivalent local martingale measure, i.e., a probability measure such that is a local -martingale.

Assumption 2.3

The maximal expected utility in the pure investment problem (2.1) is finite, i.e., .

Example 2.4

1.

In a univariate exponential Lévy model , Assumption 2.2 is satisfied if is neither a.s. decreasing nor a.s. increasing. In this case, by [37, Corollary 3.7], Assumption 2.3 holds if and only if , i.e., if and only if the return process has finite -th moments.

2.

By [26, Theorem 3.3], Assumptions 2.2 and 2.3 are always satisfied in the BNS model if the investor’s risk aversion is bigger than . For , they hold provided that

(2.2)

i.e., if sufficiently large exponential moments of the driving Lévy process exist.

In view of [31, Theorem 2.2], Assumptions 2.2 and 2.3 imply that the supremum in (2.1) is attained for some strategy with strictly positive wealth process . By Assumption 2.2 and [21, I.2.27], is strictly positive as well and we can write

for the optimal number of shares per unit of wealth

which is independent of the initial endowment for power utility. Finally, [31, Theorem 2.2] also establishes the existence of a dual minimizer, i.e., a strictly positive supermartingale with such that is a supermartingale for all and is a true martingale. Alternatively, one can represent this object in terms of the opportunity process of the power utility maximization problem (cf. [6, 26] for motivation and more details).

The optimal strategy as well as the joint characteristics of the assets and the opportunity process satisfy a semimartingale Bellman equation (cf. [36, Theorem 3.2]). In concrete models, this sometimes allows to determine and by making an appropriate ansatz.

Example 2.5

1.

Let for a non-monotone Lévy process with finite -th moments. Then it follows from [37, Lemma 5.1] that there exists a unique maximizer of

over the set of fractions of wealth invested into stocks that lead to nonnegative wealth processes. By [37, Theorem 3.2], the optimal number of shares per unit of wealth is given by

with corresponding wealth process and opportunity process

2.

By [26, Theorem 3.3], it is also optimal to hold a constant fraction of wealth in stocks in the BNS model, namely (provided that the conditions of Example 2.4 are satisfied). The optimal number of shares per unit of wealth is then given by with corresponding wealth process , and opportunity process

for

where denotes the Lévy exponent of .

In addition to the traded securities, we now also consider a non-traded European contingent claim with maturity and payment function , which is an -measurable random variable. Following [32, 33], we assume that can be superhedged by some admissible strategy as, e.g., for European puts and calls.

Assumption 2.6

for some and .

If the investor sells units of at time , her terminal wealth should be sufficiently large to cover the payment due at time . This leads to the following definition (cf. [19, 9] for more details).

Definition 2.7

A strategy is called maximal if the terminal value of its wealth process is not dominated by that of any other strategy in . An arbitrary strategy is called acceptable if its wealth process can be written as

for some and such that , and, in addition, is maximal. For and we denote by

the set of acceptable strategies whose terminal value dominates .

Remark 2.8

Given Assumption 2.2, we have by [9, Theorem 5.7] combined with [23, Lemma 3.1 and Proposition 3.1] .

Let an initial endowment of be given. If the investor sells units of for a price of each, her initial position consists of in cash as well as units of the contingent claim . Hence represents the natural set of admissible trading strategies for utility functions defined on . The maximal expected utility the investor can achieve by dynamic trading in the market is then given by

Definition 2.9

Fix . A number is called utility indifference price of if

(2.3)

Existence of indifference prices does not hold in general for power utility. However, a unique indifference price always exists if the number of contingent claims sold is sufficiently small or, conversely, if the initial endowment is sufficiently large.

Lemma 2.10

Suppose Assumptions 2.2, 2.3 and 2.6 hold. Then a unique indifference price exists for sufficiently small . More specifically, (2.3) has a unique solution if , respectively if and , where denotes the initial endowment of the superhedging strategy for from Assumption 2.6.

Proof. First notice that is concave and strictly increasing on its effective domain. By [31, Theorem 2.1], for all . For and we have for . In particular, is continuous and strictly increasing on and in particular on by [40, Theorem 10.1]. By we have . Moreover, Assumption 2.6 implies . Hence there exists a unique solution to . Similarly, for general and , the function is finite, continuous and strictly increasing on an open set containing . Moreover, and . Hence there exists a unique such that . This proves the assertion.

We now turn to optimal trading strategies in the presence of random endowment. Their existence has been established by [8] resp. [19] in the bounded resp. general case.

Theorem 2.11

Fix satisfying the conditions of Lemma 2.10 and suppose Assumptions 2.2, 2.3 and 2.6 are satisfied. Then there exists such that

Moreover, the corresponding optimal value process is unique.

Proof. This follows from [19, Theorem 2 and Corollary 1] because the proof of Lemma 2.10 shows that belongs to the interior of .

Without contingent claims, the investor will trade according to the strategy , whereas she will invest into if she sells units of for each. Hence, the difference between both strategies represents the action the investors needs to take in order to compensate for the risk of selling units of . This motivates the following notion:

Definition 2.12

The trading strategy is called utility-based hedging strategy.

3 The asymptotic results of Kramkov and Sîrbu

We now give a brief exposition of some of the deep results of [32, 33] concerning the existence and characterization of first-order approximations of utility-based prices and hedging strategies in the following sense.

Definition 3.1

Real numbers and are called marginal utility-based price resp. risk premium per option sold if

for , where is well-defined for sufficiently small by Lemma 2.10. A trading strategy is called marginal utility-based hedging strategy if there exists such that

(3.1)

in -probability and is a martingale for the dual minimizer of the pure investment problem.

Remark 3.2

[32, Theorems A.1, 8, and 4] show that for power utility functions, a trading strategy is a marginal utility-based hedging strategy in the sense of Definition 3.1 if and only if it is a marginal hedging strategy in the sense of [33, Definition 2].

The asymptotic results of [32, 33] are derived subject to two technical assumptions.

Assumption 3.3

The following process is -bounded:

The reader is referred to [32] for more details on -bounded processes as well as for sufficient conditions that ensure the validity of this assumption. In our concrete examples, we have the following:

Lemma 3.4

1.

Let for a non-monotone Lévy process with finite -th moments. Then Assumption 3.3 holds if the optimizer from Example 2.5 lies in the interior of the set of fractions of wealth in stocks leading to nonnegative wealth processes.

2.

Assumption 3.3 is automatically satisfied if the stock price is continuous. In particular, it holds in the BNS model.

Proof. First consider Assertion 1. In view of [32, Lemma 8], it suffices to show that is bounded by a predictable process. If , there exists with ; hence by definition of . Consequently, and thus

which shows that the first component of is bounded by a predictable process and hence -bounded. Likewise, if , there exists with . Then and in turn . Hence it follows as above that is bounded by a predictable process. The assertion for the second component of follows similarly.

If the stock price process is continuous, both and are predictable. Hence Assertion 2 follows immediately from [32, Lemma 8].

Since is a martingale with terminal value , we can define an equivalent probability measure via

Let be the space of square-integrable -martingales starting at and set

(3.2)

Assumption 3.5

There exists a constant and a process , such that

for

Assumption 3.5 means that the claim under consideration can be superhedged with portfolios as in (3.2). Note that this is again evidently satisfied for European puts and calls.

Remark 3.6

By [32, Remark 1], Assumption 3.5 implies that Assumption 2.6 holds. In particular, it ensures that indifference prices and utility-based hedging strategies exist for sufficiently small if the pure investment problem is well-posed, i.e., if Assumptions 2.2 and 2.3 are also satisfied.

In the proof of [33, Lemma 1] it is shown that the process

is a square-integrable -martingale. Hence it admits a decomposition

(3.3)

where and is an element of the orthogonal complement of in . Note that this decomposition coincides with the classical Galtchouk-Kunita-Watanabe decomposition if itself is a square-integrable martingale. The following theorem is a reformulation of the results of [32, 33] applied to power utility, and also contains a feedback representation of the utility-based hedging strategy in terms of the original numeraire.

Theorem 3.7

Suppose Assumptions 2.2, 2.3, 3.3, and 3.5 hold. Then the marginal utility-based price and the risk premium exist and are given by

A marginal-utility-based hedging strategy is given in feedback form as the solution of the stochastic differential equation

with from (3.3), and where denotes the identity matrix on .

Proof. The first two assertions follow immediately from [32, Theorems A.1, 8, and 4] adapted to the present notation. For the third, [33, Theorem 2] and [32, Theorems A.1, 8, and 4] yield

(3.4)

because the process from [33, Equation (23)] coincides with for power utility. Set

Then we have and

(3.5)

by [14, Proposition 2.1]. The predictable sets increase to , the predictable process is bounded, and we have

By [23, Lemma 2.2] and (3.5), this implies as well as

Hence solves the stochastic differential equation

(3.6)

By [20, (6.8)] this solution is unique. Since we have shown above, it follows as in the proof of [6, Lemma 4.9] that is well-defined. also solves (3.6), hence we obtain

In view of (3.4), the process therefore satisfies (3.1), so that is indeed a marginal utility-based hedge in the sense of Definition 3.1.

Remark 3.8

If the dual minimizer is a martingale and hence – up to the constant – the density process of the -optimal martingale measure with respect to , the generalized Bayes formula yields . In particular, the marginal utility-based price of the claim is given by its expectation under in this case.

The computation of the optimal strategy and the corresponding dual minimizer in the pure investment problem 2.1 has been studied extensively in the literature. In particular, these objects have been determined explicitly in a variety of Markovian models using stochastic control theory resp. martingale methods. Given , the computation of can then be dealt with using integral transform methods or variants of the Feynman-Kac formula. Consequently, we suppose from now on that and are known and focus on how to obtain and .

As reviewed above, [32, 33] show that and can be obtained by calculating the generalized Galtchouk-Kunita-Watanabe decomposition (3.3). Since is generally only a -supermartingale, this is typically very difficult. If however, happens to be a square-integrable -martingale, (3.3) coincides with the classical Galtchouk-Kunita-Watanabe decomposition. By [11], this shows that represents the mean-variance optimal hedging strategy for the claim hedged with under the measure and is given by the corresponding minimal expected squared hedging error in this case. Moreover, and can then be characterized in terms of semimartingale characteristics.

Assumption 3.9

is a square-integrable -martingale.

For exponential Lévy models, this assumption satisfied if the budget constraint is “not binding” for the optimal fraction of stocks and if, in addition, the driving Lévy process is square-integrable. For the BNS model it is only a matter of integrability.

Lemma 3.10

1.

Let for a non-monotone Lévy process with finite second moments. Then Assumption 3.9 is satisfied if the optimizer of the pure investment problem lies in the interior of .

2.

Let , where is a BNS model. If or (2.2) holds, then is a -martingale.

Proof. If lies in the interior of , it follows from [36, Proposition 5.12] that the dual optimizer is a local martingale. Since it is also the exponential of a Lévy process (cf. [37, Section 6]), it is in a fact a true martingale. Thus it is – up to normalization with – the density process of the -optimal martingale measure by [36, Remark 5.18]. Combined with [21, Proposition III.3.8], this yields that is a -martingale and it remains to show that is square-integrable. By Propositions A.2, A.3, and A.4, the process is the stochastic exponential of a semimartingale with local -characteristics

relative to the truncation function on . This truncation function can be used because is -locally a square-integrable martingale. By [21, Propositions II.2.29 and III.6.35], this holds because is square-integrable, is bounded (cf. the proof of Lemma 3.4) and hence and for some constant (cf. [21, Theorem II.1.8]). As the -characteristics of are deterministic, is a -Lévy process by [21, Corollary II.4.19] and a square-integrable martingale by [21, Proposition I.4.50]. Therefore is a square-integrable martingale as well by [35, Lemma A.1.(x)]. This proves Assertion 1.

Assertion 2 is shown in the proof of [26, Theorem 3.3].

The square-integrability of in the BNS model is discussed in Remarks 4.3 and 5.7 below. Given Assumption 3.9, we have the following representation.

Lemma 3.11

Suppose Assumptions 2.2, 2.3, 3.3, 3.5 and 3.9 hold. Denote by the modified second -characteristic of with respect to some (cf. Appendix A). Then

(3.7)

Proof. Since is a square integrable -martingale by Assumption 3.9, the claim follows from [6, Theorems 4.10 and 4.12] applied to the martingale case.

4 An alternative representation

We now develop our alternative representation of power utility-based prices and hedging strategies. As explained in the introduction, they can – morally speaking – be represented as the solution to a mean-variance hedging problem relative to the original numeraire, but subject to yet another probability measure . Given Assumption 3.9, the latter can be defined as follows:

Remark 4.1

If we write the density process of with respect to as for a semimartingale with , the local joint -characteristics of and relative to some truncation function on satisfy

(4.1)

and solve

(4.2)

by [23, Lemma 3.1] and Propositions A.3, A.2 . Conversely, if a strictly positive semimartingale satisfies and (4.1), (4.2), then is a -martingale and the density process of if it is a true martingale.

In concrete models, the drift condition (4.2) often allows to determine by making an appropriate parametric ansatz. For exponential Lévy models and the BNS model, this leads to the following results.

Example 4.2

1.

For exponential Lévy models as in Example 4.2, plugging the ansatz with for into (4.2) yields

This expression is well-defined because the integrand is of order for small and bounded on the support of by the proof of Lemma 3.4 and [21, Theorem II.1.8].

One then easily verifies that . Indeed, the strictly positive -martingale is a true martingale because it is also the stochastic exponential of a Lévy process.

2.

For the BNS model, one has to make a more general ansatz for . Choosing with smooth functions satisfying as in [26], insertion into 4.2 leads to

(4.3) automatically holds for , because in this case. For , (4.3) is satisfied if

(4.4)

In either case, the true martingale property of the exponentially affine -martingale follows from [24, Corollary 3.9]. This shows that is indeed given by .

Remark 4.3

Part 2 of Example 4.2 shows that in the BNS model the first component of is square-integrable if or (4.4) holds. Hence the measure is well defined with density process in either case.

As motivated in the introduction, the measures and are linked as follows.

Lemma 4.4

Suppose Assumptions 2.2, 2.3 and 3.9 hold. Then the process

satisfies and the density process of with respect to is given by

In particular, and the stochastic logarithm is well-defined.

Proof. The first part of the assertion is trivial, whereas the second follows from . Since , [21, I.2.27] yields and hence the third part of the assertion by [21, II.8.3].

Remark 4.5

is linked to the opportunity process of the pure investment problem and the process from Remark 4.1 via

by the generalized Bayes’ formula, , and because as well as are martingales.

In our examples, this leads to the following.

Example 4.6

1.

Suppose for a non-monotone Lévy process with finite second moments. Then and for and as in Examples 2.5 resp. 4.2.

2.

Let for a BNS model satisfying (4.4) if and, additionally, (2.2) if . Then and, by Itô’s formula,

which coincides with the conditional expectation under the -optimal martingale measure , if the latter exists. Denote by

-differential characteristics of the semimartingale and define

where denotes an arbitrary -semimartingale decomposition of . We then have the following representation of the marginal utility-based hedging strategy and the risk premium in terms of semimartingale characteristics, which is the main result of this paper.

Theorem 4.7

Suppose Assumptions 2.2, 2.3, 3.3, 3.5 and 3.9 hold. Then are well-defined, the strategy given in feedback form as the solution of the stochastic differential equation

is a marginal utility-based hedge, and the corresponding risk premium is

Remark 4.8

As is customary for mean-variance optimal hedges [42, 6], the strategy is described in “feedback form”, i.e., it is computed as the solution of a stochastic differential equation involving its past trading gains , which reduces to a simple recursive formula in discrete time (cf., e.g., [43, Theorem 2.4]). Alternatively, the corresponding linear stochastic differential equation for can be solved [6, Corollary 4.11],

leading to a cumbersome but explicit expression for the hedge .

In view of [6, Theorems 4.10 and 4.12], Theorem 4.7 states that the first-order approximations for and can essentially be computed by solving the mean-variance hedging problem for the claim under the (non-martingale) measure relative to the original numeraire. However, this assertion only holds true literally if the dual minimizer is a martingale and if the optimal strategy in the pure investment problem is admissible in the sense of [6, Corollary 2.5], i.e., if and is a -martingale for any absolutely continuous signed -martingale measure with density process and . More precisely, in this case the strategy is efficient on the stochastic interval in the sense of [6, Section 3.1] and is the corresponding adjustment process in the sense of [6, Definition 3.8]. By [6, Corollary 3.4] this in turn implies that is the opportunity process in the sense of [6, Definition 3.3]. Hence it follows along the lines of [6, Lemma 3.15] that the opportunity neutral measure with density process

exists. By [6, Lemma 3.17 and Theorem 4.10], indeed coincide with the corresponding modified second characteristics of under . Hence [6, Theorems 4.10 and 4.12] yield that relative to the probability measure , the process represents a variance-optimal hedging strategy for while the minimal expected squared hedging error of is given by the -fold of . Moreover, and in particular the marginal utility-based price are given as conditional expectations under the variance-optimal martingale measure with respect to , which coincides with the -optimal martingale measure with respect to .

Proof of Theorem 4.7. An application of Propositions A.3 and A.2 yields the -differential characteristics of the process . Now, since is the density process of with respect to , the -characteristics of can be obtained with Proposition A.4. Another application of Proposition A.2 then allows to compute the -characteristics of .

Since by Assumption 3.9 and by the proof of [33, Lemma 1], the modified second characteristics , and exist and are given by

(4.5)

(4.6)

(4.7)

for . In particular it follows that , and are well defined. By the definition of in Equation (3.7) and [1, Theorem 9.1.6] we have

defines a marginal utility-based hedging strategy. Let

Then it follows from the definition of and (4.10) that

because by [1, Theorem 9.1.6]. In particular, . Since and hence by [21, I.4.61], this implies

(4.11)

For define the predictable sets . By Proposition A.3 and (4.11), we have and hence and . Together with Proposition A.4, this implies that the local characteristics of under the equivalent local martingale measure from Assumption 2.2 vanish by [23, Lemma 3.1]. Hence and it follows from [23, Lemma 2.2] that with . Taking into account the definition of , this shows

i.e., solves the feedback equation

(4.12)

Since and is a vector space, it follows that , too. As in the proof of [6, Lemma 4.9], this in turn yields that is well-defined and in . Evidently, also solves (4.12) and, since the solution is unique by [20, (6.8)], we obtain . Therefore is a marginal utility-based hedging strategy.

We now turn to the risk premium . First notice that by [1, Theorem 9.1.6],

Hence is an increasing predictable process and, by Lemmas 3.11 and A.5,

Since we have shown above, [14, Proposition 2.1] and the proof of Theorem 3.7 yield for . Hence

After inserting , from (4.7) resp. (4.6) and the definition of , this leads to

(4.13)

Now notice that the definition of the stochastic exponential and [21, I.4.36] imply

By [21, I.4.49] the process is a local martingale. If denotes a localizing sequence, this yields

and hence

by monotone convergence. Combining this with (4.13), we obtain

The arguments used to show in the proof of Theorem 4.7 also yield that one obtains a marginal utility-based hedging strategy if the pure hedge coefficient is replaced by any other solution of .

2.

An inspection of the proof of Theorem 4.7 shows that the formulas for and are independent of the specific semimartingale decomposition of that is used. In particular, the not necessarily predictable term disappears in the formula for by [1, Theorem 3.9]. If the semimartingale is -special, one can choose the canonical decomposition [21, II.2.38]. By [21, II.2.29], this yields

If additionally has no fixed times of discontinuity, [21, II.2.9] shows that can be chosen to be continuous, which implies .

3.

For continuous , our feedback representation of coincides with [33, Theorem 3] because the modified second characteristic is invariant with respect to equivalent changes of measure for continuous processes.

5 Semi-explicit formulas in concrete models

We now discuss how Theorem 4.7 can be applied in our concrete examples to yield numerically tractable representations of power utility-based prices and hedging strategies.

5.1 Exponential Lévy models

For exponential Lévy models, Theorem 4.7 indeed leads to a mean-variance hedging problem. Consequently, semi-explicit formulas for the objects of interest are provided by the results of Hubalek et al. [18] for mean-variance hedging in exponential Lévy models.

To this end, we fix a univariate exponential Lévy model , with some non-monotone square-integrable Lévy process . Its Lévy-Khintchine triplet relative to the truncation function is denoted by . Finally, we suppose throughout that the optimal fraction for the pure investment problem lies in the interior of the admissible fractions of wealth in stock , implying that all assumptions of Sections 3 and 4 are satisfied.

Remark 5.1

By [14, Lemma A.8], the stock price can also be written as the ordinary exponential of the Lévy process with Lévy-Khintchine triplet

relative to .

Since the density process of with respect to is an exponential Lévy process, Proposition A.4 shows that is also a Lévy process under with Lévy-Khintchine triplet given by

relative to . This truncation function can be used because is square-integrable under as well by [41, Corollary 25.8] and the proof of Lemma 3.4. Moreover, since the budget constraint is “not binding,” the first-order condition [37, Equation (6.3)] implies that the drift rate can also be written as

(5.1)

Lemma 5.2

The optimal trading strategy in the pure investment problem is admissible in the sense of [6, Corollary 2.5].

Proof. In view of [42, Proposition 13], the mean-variance optimal hedge for the constant claim is for . Hence by (5.1); in particular, is admissible in the sense of Schweizer [42] and therefore in the sense of Černý and Kallsen [6] as well by [6, Corollary 2.9].

Together with the discussion at the end of Section 4, Lemma 5.2 immediately yields

Corollary 5.3

Let be a contingent claim satisfying Assumption 3.5. Then the marginal utility-based price , the marginal utility-based hedging strategy , and the risk premium from Theorem 4.7 coincide with the mean-variance optimal initial capital, the mean-variance optimal hedge and the -fold of the minimal expected squared hedging error for under .

Corollary 5.3 implies that – in first-order approximation – power utility-based hedging corresponds to mean-variance hedging, but for a Lévy process with different drift and jump measure. If , which is equivalent to being a martingale under the physical measure , then and no adjustment is necessary. If in the economically most relevant case of a positive drift, the stock price process is a -submartingale, but turns into a supermartingale under . Moreover, negative jumps become more likely and positive jumps less likely, such that a negative skewness is amplified when passing from to . The magnitude of these effects depends on the investor’s risk aversion . Note that as the latter becomes large, the dynamics of the return process converge to those under the minimal entropy martingale measure (cf., e.g., [15]). Hence, as risk aversion becomes large, asymptotic power utility-based pricing and hedging approaches its counterpart for exponential utility.

The above considerations apply to any contingent claim satisfying Assumption 3.5, i.e., which can be superhedged with respect to the numeraire given by the optimal wealth process in the pure investment problem. To obtain numerically tractable formulas, one has to make additional assumptions. For example, semi-explicit solutions to the mean-variance hedging problem for exponential Lévy models have been obtained in [18] using the Laplace transform approach put forward in [38]. The key assumption for this approach is the existence of an integral representation of the payoff function in the following sense.

Assumption 5.4

Suppose for a function such that

for such that the integral exists for all and such that .

Most European options admit a representation of this kind, see, e.g., [18, Section 4].

Example 5.5

For a European call option with strike we have and, for and ,

By evaluating the formulas of Hubalek et al. [18] under , we obtain the following semi-explicit representations. They are expressed in terms of the Lévy exponent of the log-price under .

Theorem 5.6

For a contingent claim satisfying Assumptions 3.5 and 5.4, the marginal utility-based price and a marginal utility-based hedging strategy are given by

with

Moreover, the corresponding risk premium for can be written as

for and as in Examples 2.5 and 4.2, respectively, and

We now turn to the application of Theorem 4.7 to the BNS model with stochastic volatility. Throughout, we assume that the conditions of Examples 2.4 and 4.2 are satisfied, i.e., either or sufficiently large exponential moments of the subordinator driving the variance process exist. In the first case, we also suppose is integrable. By Proposition A.4, the -dynamics of the variance process and the return process are given by

Here and are the constant drift and mean reversion rates of the BNS model under , is a standard Brownian motion (under both and ), and is an inhomogeneous -Lévy process with characteristics

relative to the truncation function . Hence is an inhomogeneous BNS model under . Note that as for exponential Lévy models, the drift rate of the return process changes its sign when moving from (under ) to (under ). The effect on the volatility process depends on the sign of , which is positive for and negative for . If , i.e., for less risk-averse investors, the mean of (i.e., the average size of the positive volatility jumps) increases because jumps (in particular, large ones) become more likely under . For more risk averse investors with , the frequency of jumps is decreased under , which also leads to a decrease in the average value of volatility. Since decreases resp. increases to as for resp. , the deviation from the -dynamics of is largest at the initial time and tends to zero as . Finally, as the investor’s risk aversion becomes large, the dynamics of again tend to their counterparts under the minimal entropy martingale measure corresponding to exponential utility, which was determined in [4].

With the -dynamics of at hand, we can now provide a sufficient condition for the validity of Assumption 3.9 in the BNS model. More specifically, is square-integrable under by [24, Theorem 5.1] provided that

If, in addition, the conditions of Example 4.2 are satisfied, Assumption 3.9 holds.

We now turn to the computation of semi-explicit representations for the marginal utility-based price (cf. Remark 3.8) as well as the utility-based hedge and the risk premium from Theorem 4.7 for claims admitting an integral representation as in Assumption 5.4. The (inhomogeneous) BNS model is studied from the point of view of mean-variance hedging in [30]. As noted in the introduction, the formulas in Theorem 4.7 formally agree with such a problem under the appropriate probability measure . Therefore the calculations in [30] can be adapted to the present situation. In that paper, admissibility of the candidate solution to the pure investment problem under quadratic utility is not shown. Nevertheless, the results from [30] can be applied here because does not have to be admissible for the application of Theorem 4.7. Put differently, the calculations in [30] can be used without explicitly referring to the quadratic hedging problem studied there. Below, we outline the necessary steps. This sketch could be turned into a rigorous proof, similarly as in [27, Theorems 4.1 and 4.2].

The first step is to determine the mean value process . Since the density process of with respect to is the exponential of an inhomogeneous affine process (cf. [10, 24] for more details), Proposition A.4 shows that is also an inhomogeneous affine process under . Using the integral representation for , Fubini’s theorem, and the affine transform formula for (compare [10, 24]) then leads to

(5.2)

with

In the second step, we turn to the marginal utility-based hedging strategy . The representation (5.2) for and the bilinearity of the predictable quadratic variation yields integral representations for the modified second -characteristics of , too, where the integrands can be computed using Proposition A.2 (cf. the proof of [30, Theorem 3.3] for more details). Plugging these in Theorem 4.7 gives

with

for as above.

Remark 5.7

Provided that differentiation and integration can be interchanged, the pure hedge coefficient in the BNS model is given by the derivative of with respect to . Hence the marginal utility-based hedging strategy is given as the sum of the delta hedge with respect to the marginal utility-based option price and a feedback term. This is a generic result in affine models with continuous asset prices and uncorrelated volatility processes, compare [30].

Finally, in a third step, it remains to consider the risk premium in Theorem 4.7. Plugging in the expression for and , we find

Hence it remains to compute the expectation in the formula for the risk premium . Here, (5.2) again leads to integral representations for . The product of and the integrand once more turns out to be the exponential of an inhomogeneous affine process. Its expectation can therefore again be computed using the affine transform formula for (cf. the proof of [30, Theorem 3.4] for more details). This leads to

for

and

If the volatility process is chosen to be a Gamma-OU process, all expressions involving integrals of the characteristic exponent can be computed in closed form as well. More specifically, let be a Gamma-OU process with mean reversion rate and stationary -distribution and let

for constants . Then if , we have

for and where denotes the distinguished logarithm in the sense of [41, Lemma 7.6]. This follows by inserting the Lévy exponent , which is analytic on , and integration using decomposition into partial fractions.

6 Numerical illustration

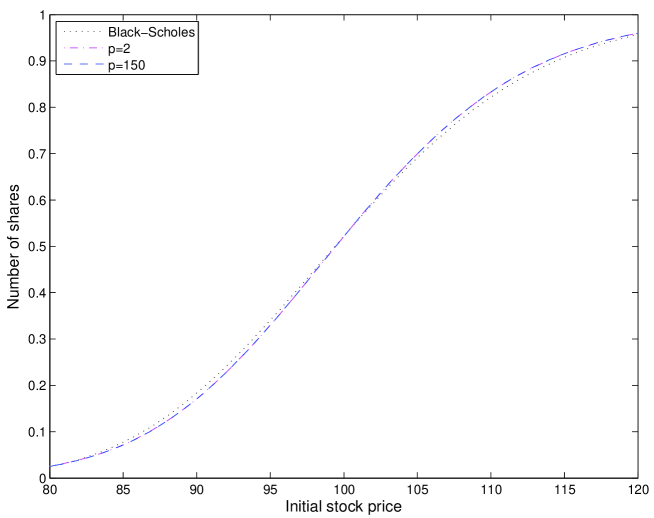

Figure 1: Initial Black-Scholes hedge and initial utility-based BNS-hedges for , and a European call with strike and maturity .

Mean-variance hedging for the BNS Gamma-OU stochastic volatility model is considered in [30]. Since the formulas in the previous section are of the same form, the numerical algorithm applied in [30] can also be used to explore this model from the point of view of utility-based pricing and hedging. Exponential Lévy processes could be treated analogously (compare [18]). Since the corresponding results are very similar, we omit them here.

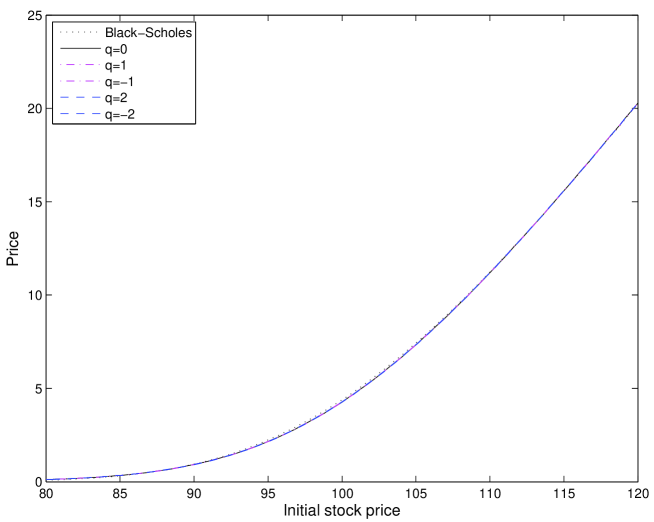

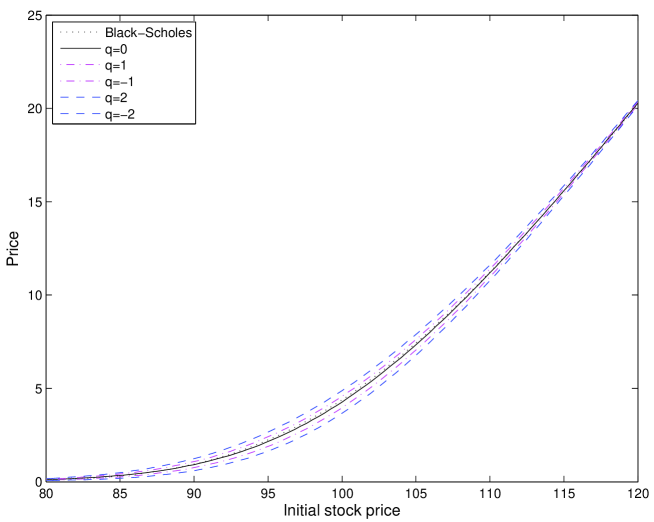

Figure 2: Black-Scholes price and approximate indifference price in the BNS model for and a European call with strike and maturity .Figure 3: Black-Scholes price and approximate indifference price in the BNS model for and a European call with strike and maturity .

As a concrete specification, we consider the discounted BNS-Gamma-OU model with parameters as estimated in [25] from a DAX time series, i.e.,

We let and put , which implies that indifference prices and utility-based hedging strategies exist for and . By our above results, first-order approximations of the utility-indifference price and the utility-based hedging strategy exist for by Lemma 2.10 resp. Theorem 2.11. Moreover, Assumptions 3.5 and 5.4 hold for European call-options by Example 5.5. The formulas from Section 5.2 can now be evaluated using numerical quadrature, where we use .

The initial hedges for and in Figure 1 below cannot be distinguished by eye. Indeed, the maximal relative difference between the two strategies is for , which implies that the utility-based hedging strategy is virtually independent of the investor’s risk aversion. Moreover, both strategies are quite close to the Black-Scholes hedging strategy, the maximal relative difference being about 8.9%.

We now turn to utility-based pricing. First, note that in our specification the marginal utility-based price barely depends on the investor’s risk aversion, and is almost indistinguishable from its Black-Scholes counterpart. For a relative risk aversion of , the effect of the first-order risk adjustment is also very small (cf. Figure 2). This resembles similar findings of [13, 12] on utility-based pricing and hedging for basis risk.

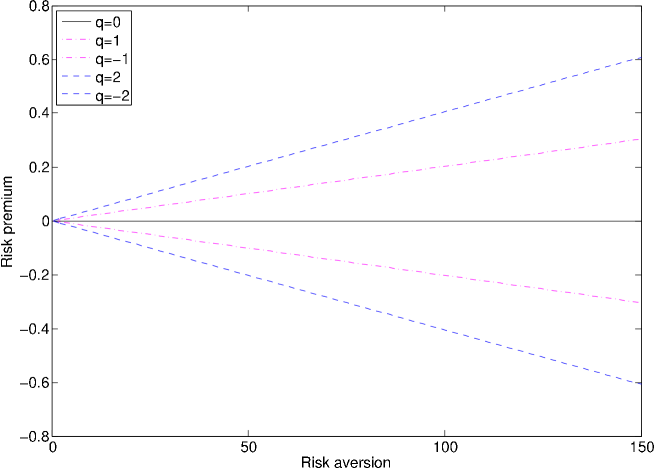

Figure 4: Risk premia for at-the-money European calls with strike and maturity in the BNS model for risk aversions .

In fact, much higher risk aversions as, e.g., in Figure 3 are required to obtain a bid price below and an ask-price above the Black-Scholes price for one option as a result of the first-order risk adjustment. For evidence supporting such high levels of risk aversion, cf., e.g., [22]. Finally, Figure 4 depicts the dependence of the risk premium on the investor’s relative risk aversion , which turns out to be almost linear. Note that since is inversely proportional to the initial endowment , this also implies that is virtually linear in the investor’s absolute risk aversion , which holds exactly for exponential utility (cf. [34, 3, 28]).

Appendix A Appendix

In this appendix we summarize some basic notions regarding semimartingale characteristics (cf. [21] for more details). In addition, we state and prove an auxiliary result which is used in the proof of Theorem 4.7.

To any -valued semimartingale there is associated a triplet of characteristics, where resp. denote - resp. -valued predictable processes and a random measure on (cf. [21, II.2.6]). The first characteristic depends on a truncation function such as . Instead of the characteristics themselves, we typically use the following notion.

Definition A.1

Let be an -valued semimartingale with characteristics relative to some truncation function on . In view of [21, II.2.9], there exist a predictable process , an -valued predictable process , an -valued predictable process and a transition kernel from into such that

where we implicitly assume that is a good version in the sense that the values of are non-negative symmetric matrices, and . We call local characteristics of .

If denote local characteristics of some semimartingale , we write

and call the modified second characteristic of provided that the integral exists. This notion is motivated by the fact that by [21, I.4.52] if the corresponding integral is finite. We write and for the differential characteristics and the modified second characteristic of a semimartingale . Likewise, the joint local characteristics of two semimartingales , are denoted by

and

if the modified second characteristic of exists. The characteristics of a semimartingale under some other measure are denoted by . The following rules for the computation of characteristics are used repeatedly in the proofs of this paper.

Proposition A.2 (-function)

Let X be an -valued semimartingale with local characteristics . Suppose that is twice continuously differentiable on some open subset such that , are -valued. Then the -valued semimartingale has local characteristics , where

as well as

Here, etc. denote partial derivatives and again the truncation function on .

Proof. This follows immediately from [14, Corollary A.6].

Proposition A.3 (Stochastic integration)

Let X be an -valued semimartingale with local characteristics and H an -valued predictable process with for . Then local characteristics of the -valued integral process are given by , where

Here denotes the truncation function which is used on .

Let be a probability measure with density process . Local equivalence yields that and are strictly positive by [21, I.2.27]. Hence the stochastic logarithm is a well-defined semimartingale. For an -valued semimartingale we now have the following result, which relates the local -characteristics of to the local characteristics of under .

Proposition A.4 (Equivalent change of measure)

Local -characteristics of the process are given by , where

The following observation is needed in the proof of Theorem 4.7.

Lemma A.5

Let with density process . Then for any increasing, predictable process with we have

Proof. Since is a -martingale and is predictable and of finite variation, is a local -martingale by [21, I.3.10 and I.4.34]. If denotes a localizing sequence, is a martingale starting at . By [21, III.3.4 and I.4.49], this implies

Hence monotone convergence yields as claimed.

References

[1]Albert, A. (1972). Regression and the Moore-Penrose Pseudoinverse. Academic Press, New York.

[2]Barndorff-Nielsen, O. and Shephard, N. (2001). Non-Gaussian Ornstein-Uhlenbeck-based models and some of their uses in financial economics. J. R. Statist. Soc. B63 167–241.

[3]Becherer, D. (2006). Bounded solutions to backward SDE’s with jumps for utility optimization and indifference hedging.

Ann. Appl. Probab.16 2027–2054.

[4]Benth, F. and Meyer-Brandis, T. (2005). The density process of the minimal entropy martingale measure in a stochastic volatility model with jumps.

Finance Stoch.9 563–575.

[5]Černý, A. (2007). Optimal continuous-time hedging with leptokurtic returns.

Math. Finance17 175–203.

[6]Černý, A. and Kallsen, J. (2007). On the structure of general mean-variance hedging strategies.

Ann. Probab. 35 1479–1531.

[7]Cont, R., Tankov, P., and Voltchkova, E. (2007). Hedging with options in presence of jumps.

Stochastic Analysis and Applications: The Abel Symposium 2005 in honor of Kiyosi Itô (F. Benth et al., eds.) 197–218. Springer, Berlin.

[8]Cvitanić, J., Schachermayer, W., and Wang, H. (2001). Utility maximization in incomplete markets with random endowment.

Finance Stoch.5 259–272.

[9]Delbaen, F. and Schachermayer, W. (1998). The fundamental theorem of asset pricing for unbounded stochastic processes.

Math. Ann.312 215–250.

[10]Filipović, D. (2005). Time-inhomogeneous affine processes. Stochastic Process. Appl.115 639–659.

[11]Föllmer, H. and Sondermann, D. (1986). Hedging of nonredundant contingent claims.

Contributions to Mathematical Economics (W. Hildenbrand and A. Mas-Colell, eds.) 205–223, North-Holland, Amsterdam.

[12]Henderson, V. and Hobson, D. (2002). Real options with constant relative risk aversion. J. Econom. Dynam. Control27 329–355.

[13]Henderson, V. (2002). Valuation of claims on nontraded assets using utility maximization. Math. Finance12 351–373.

[14]Goll, T. and Kallsen, J. (2000). Optimal portfolios for logarithmic utility.

Stochastic Process. Appl.89 31–48.

[15]Fujiwara, T. and Miyahara, Y. (2003). The minimal entropy martingale measures for geometric Lévy processes.

Finance Stoch.7 509–531.

[16]Gourieroux, C., Laurent, J., and Pham, H. (1998). Mean-variance hedging and numéraire.

Math. Finance8 179–200.

[17]Hodges, S. and Neuberger, A. (1989). Optimal replication of contingent claims under transaction costs.

Rev. Futures Markets8 222–239.

[18]Hubalek, F., Krawczyk, L., and Kallsen, J. (2006). Variance-optimal hedging for processes with stationary independent increments.

Ann. Appl. Probab.16 853–885.

[19]Hugonnier, J. and Kramkov, D. (2004). Optimal investment with random endowments in incomplete markets.

Ann. Appl. Probab.14 845–864.

[20]Jacod, J. (1979).

Calcul Stochastique et Problèmes de Martingales.

Springer, Berlin.

[21]Jacod, J. and Shiryaev, A. (2003).

Limit Theorems for Stochastic Processes.

Springer, Berlin, second edition.

[22]Janeček, K. (2004). What is a realistic aversion to risk for real-world

individual investors? Working paper, Carnegie Mellon University.

[23]Kallsen, J. (2004). -localization and -martingales.

Theory Probab. Appl.48 152–163.

[24]Kallsen, J. and Muhle-Karbe, J. (2010). Exponentially affine martingales, affine measure changes and exponential moments of affine processes. Stochastic Process. Appl.120 163–181.

[25]Kallsen, J. and Muhle-Karbe, J. (2011). Method of moment estimation in time-changed Lévy models. Statist. Decisions. 28 169–194

[26]Kallsen, J. and Muhle-Karbe, J. (2010). Utility maximization in affine stochastic volatility models. Int. J. Theor. Appl. Finance13 459–477.

[27]Kallsen, J. and Pauwels, A. (2009). Variance-optimal hedging in general affine stochastic volatility models.

Adv. in Appl. Probab.42 83–105.

[28]Kallsen, J. and Rheinländer, T. (2010). Asymptotic utility-based pricing and hedging for exponential utility. Statist. Decisions. 28 17–36.

[29]Kallsen, J. and Shiryaev, A. (2002). Time change representation of stochastic integrals.

Theory Probab. Appl.46 522–528.

[30]Kallsen, J. and Vierthauer, R. (2009). Quadratic hedging in affine stochastic volatility models.

Rev. Deriv. Res.12 3–27.

[31]Kramkov, D. and Schachermayer, W. (1999). The asymptotic elasticity of utility functions and optimal investment in incomplete markets.

Ann. Appl. Probab.9 904–950.

[32]Kramkov, D. and Sîrbu, M. (2006). The sensitivity analysis of utility based prices and the risk-tolerance wealth processes.

Ann. Appl. Probab.16 2140–2194.

[33]Kramkov, D. and Sîrbu, M. (2007). Asymptotic analysis of utility-based hedging strategies for small number of contingent claims.

Stochastic Process. Appl.117 1606–1620.

[34]Mania, M. and Schweizer, M. (2005). Dynamic exponential utility indifference valuation.

Ann. Appl. Probab.15 2113–2143.

[35]Muhle-Karbe, J. and Nutz, M. (2012). Small-time asymptotics of option prices and first absolute moments. J. Appl. Probab.48 1003–1020.

[36]Nutz, M. (2012). The Bellman equation for power utility maximization with semimartingales. Ann. Appl. Probab.22 363–406.

[37]Nutz, M. (2010). Power utility maximization in constrained exponential Lévy models. Math. Finance22 690–709.

[38]Raible, S: (2000). Lévy Processes in Finance: Theory, Numerics, and Empirical Facts. Dissertation Universität Freiburg i. Br.

[39]Rheinländer, T. and Schweizer, M. (1997). On -projections on a space of stochastic integrals. Ann. Probab.25 1810–1831.

[40]Rockafellar, T. (1970). Convex Analysis.

Princeton University Press, Princeton.

[41]Sato, K. (1999). Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press, Cambridge.

[42]Schweizer, M. (1994). Approximating random variables by stochastic integrals.

Ann. Probab.22 1536–1575.

[43]Schweizer, M. (1995). Variance-optimal hedging in discrete time. Mathematics Oper. Res.20 1–32.