Variational Inducing Kernels for Sparse Convolved Multiple Output Gaussian Processes

Abstract

Interest in multioutput kernel methods is increasing, whether under the guise of multitask learning, multisensor networks or structured output data. From the Gaussian process perspective a multioutput Mercer kernel is a covariance function over correlated output functions. One way of constructing such kernels is based on convolution processes (CP). A key problem for this approach is efficient inference. Álvarez and Lawrence (2009) recently presented a sparse approximation for CPs that enabled efficient inference. In this paper, we extend this work in two directions: we introduce the concept of variational inducing functions to handle potential non-smooth functions involved in the kernel CP construction and we consider an alternative approach to approximate inference based on variational methods, extending the work by Titsias (2009) to the multiple output case. We demonstrate our approaches on prediction of school marks, compiler performance and financial time series.

1 Introduction

Gaussian processes (GPs) are flexible non-parametric models which

allow us to specify prior distributions and perform inference of

functions. A limiting characteristic of GPs is the fact that the

computational cost of inference is in general , being the

number of data points, with an associated storage requirement of

. In recent years a lot of progress

(Csató and Opper, 2001; Lawrence et al., 2003; Seeger et al., 2003; Snelson and Ghahramani, 2006; Quiñonero Candela and Rasmussen, 2005)

has been made with approximations that allow inference in

(and associated storage of , where is a user specified

number. This has made GPs practical for a range of larger scale

inference problems.

In this paper we are specifically interested in developing priors over multiple functions. While such priors can be

trivially specified by considering the functions to be independent,

our focus is on priors which specify correlations between the

functions. Most attempts to apply such priors

so far (Teh et al., 2005; Osborne et al., 2008; Bonilla et al., 2008)

have focussed on what is known in the geostatistics community as

“linear model of coregionalization” (LMC)

(Journel and Huijbregts, 1978; Goovaerts, 1997). In these models the different outputs

are assumed to be linear combinations of a set of one or more “latent

functions” so that the th output of the function,

is given by

| (1) |

where is one of latent functions that, weighted by , sum to form each of the outputs. GP priors are placed, independently, over each of the latent functions inducing a correlated covariance function over . Approaches to multi-task learning arising in the kernel community (see for example Evgeniou et al., 2005) can also be seen to be instances of the LMC framework.

We wish to go beyond the LMC framework, in particular, our focus is convolution processes (Higdon, 2002; Boyle and Frean, 2005). Using CPs for multi-output GPs was proposed by Higdon (2002) and introduced to the machine learning audience by Boyle and Frean (2005). Convolution processes allow the integration of prior information from physical models, such as ordinary differential equations, into the covariance function. Álvarez et al. (2009), inspired by Gao et al. (2008), have demonstrated how first and second order differential equations, as well as partial differential equations, can be accommodated in a covariance function. Their interpretation is that the set of latent functions are a set of latent forces, and they term the resulting models “latent force models”. The covariance functions for these models are derived through convolution processes (CPs). In the CP framework, output functions are generated by convolving latent processes with kernel functions,111Not kernels in the Mercer sense, but kernels in the normal sense. , associated to each output and latent force , so that we have

| (2) |

The LMC can be seen as a particular case of the CP, in which the kernel functions correspond to scaled Dirac -function . In latent force models the convolving kernel, , is the Green’s function associated to a particular differential equation.

A practical problem associated with the CP framework is that in these models inference has computational complexity and storage requirements . Recently, Álvarez and Lawrence (2009) introduced an efficient approximation for inference in this multi-output GP model. The idea was to exploit a conditional independence assumption over the output functions given a finite number of observations of the latent functions . This led to approximations that were very similar in spirit to the PITC and FITC approximations of Snelson and Ghahramani (2006); Quiñonero Candela and Rasmussen (2005). In this paper we build on the work of Álvarez and Lawrence. Their approximation was inspired by the fact that if the latent functions are observed in their entirety, the output functions are conditionally independent of one another (as can be seen in (2)). We extend the previous work presented in Álvarez and Lawrence (2009) in two ways. First, a problem with the FITC and PITC approximations can be their propensity to overfit when inducing inputs are optimized. A solution to this problem was given in recent work by Titsias (2009) who provides a sparse GP approximation that has an associated variational bound. In this paper we show how the ideas of Titsias can be extended to the multiple output case. Second, we notice that if the locations of the inducing points, , are close relative to the length scale of the latent function, the PITC approximation will be accurate. However, if the length scale becomes small the approximation requires very many inducing points. In the worst case, the latent process could be white noise (as suggested by Higdon (2002) and implemented by Boyle and Frean (2005)). In this case the approximation will fail completely. We further develop the variational approximation to allow us to work with rapidly fluctuating latent functions (including white noise). This is achieved by augmenting the output functions with one or more additional functions. We refer to these additional outputs as the inducing functions. Our variational approximation is developed through the inducing functions. There are also smoothing kernels associated with the inducing functions. The quality of the variational approximation can be controlled both through these inducing kernels and through the number and location of the inducing inputs.

Our approximation allows us to consider latent force models with a larger number of states, , and data points . The use of inducing kernels also allows us to extend the inducing variable approximation of the latent force model framework to systems of stochastic differential equations (SDEs). In this paper we apply the variational inducing kernel approximation to different real world datasets, including a multivariate financial time series example.

A similar idea to the inducing function one introduced in this paper, was simultaneously proposed by Lázaro-Gredilla and Figueiras-Vidal (2010). Lázaro-Gredilla and Figueiras-Vidal (2010) introduced the concept of inducing feature to improve performance over the pseudo-inputs approach of Snelson and Ghahramani (2006) in sparse GP models. Our use of inducing functions and inducing kernels is motivated by the necessity to deal with non-smooth latent functions in the convolution processes model of multiple outputs.

2 Multiple Outputs Gaussian Processes

Let , where , be the observed data associated with the output function . For simplicity, we assume that all the observations associated with different outputs are evaluated at the same inputs (although this assumption is easily relaxed). We will often use the stacked vector to collectively denote the data of all the outputs. Each observed vector is assumed to be obtained by adding independent Gaussian noise to a vector of function values so that the likelihood is , where is defined via (2). More precisely, the assumption in (2) is that a function value (the noise-free version of ) is generated from a common pool of independent latent functions , each having a covariance function (Mercer kernel) given by . Notice that the outputs share the same latent functions, but they also have their own set of parameters where are the parameters of the smoothing kernel . Because convolution is a linear operation, the covariance between any pair of function values and is given by

This covariance function is used to define a fully-coupled GP prior over all the function values associated with the different outputs.

The joint probability distribution of the multioutput GP model can be written as

The GP prior has a zero mean vector and a covariance matrix , where , which consists of blocks of the form . Elements of each block are given by for all possible values of . Each of such blocks is either a cross-covariance or covariance matrix of pairs of outputs.

Prediction using the above GP model, as well as the maximization of the marginal likelihood , where , requires time and storage which rapidly becomes infeasible even when only few hundreds of outputs and data are considered. Therefore approximate or sparse methods are needed in order to make the above multioutput GP model practical.

3 PITC-like approximation for Multiple Outputs Gaussian Processes

Before we propose our variational sparse inference method for multioutput GP regression in Section 4, we review the sparse method proposed by Álvarez and Lawrence (2009). This method is based on a likelihood approximation. More precisely, each output function is independent from the other output functions given the full-length of each latent function . This means, that the likelihood of the data factorizes according to

with the set of latent functions. The sparse method in Álvarez and Lawrence (2009) makes use of this factorization by assuming that it remains valid even when we are only allowed to exploit the information provided by a finite set of function values, , instead of the full-length function (which involves uncountably many points). Let , for , be a -dimensional vector of values from the function which are evaluated at the inputs . These points are commonly referred to as inducing inputs. The vector denotes all these variables. The sparse method approximates the exact likelihood function with the likelihood

where and are the mean and covariance matrices of the conditional GP priors . The matrix is a block diagonal covariance matrix where the th block is obtained by evaluating at the inducing inputs . Further, the matrix has entries defined by the cross-covariance function

The variables follow the GP prior and can be integrated out to give the following approximation to the exact marginal likelihood:

| (3) |

Here, is a block-diagonal matrix, where each block in the diagonal is given by for all . This approximate marginal likelihood represents exactly each diagonal (output-specific) block while each off diagonal (cross-output) block is approximated by the Nyström matrix .

The above sparse method has a similar structure to the PITC approximation introduced for single-output regression (Quiñonero Candela and Rasmussen, 2005). Because of this similarity, Álvarez and Lawrence (2009) call their multioutput sparse approximation PITC as well. Two of the properties of this PITC approximation, which can be also its limitations, are:

-

1.

It assumes that all latent functions in are smooth.

-

2.

It is based on a modification of the initial full GP model. This implies that the inducing inputs are extra kernel hyparameters in the modified GP model.

Because of point 1, the method is not applicable when the latent functions are white noise processes. An important class of problems where we have to deal with white noise processes arise in linear SDEs where the above sparse method is currently not applicable there. Because of 2, the maximization of the marginal likelihood in eq. (3) with respect to , where are model hyperparameters, may be prone to overfitting especially when the number of variables in is large. Moreover, fitting a modified sparse GP model implies that the full GP model is not approximated in a systematic and rigorous way since there is no distance or divergence between the two models that is minimized

In the next section, we address point 1 above by introducing the concept of variational inducing kernels that allow us to efficiently sparsify multioutput GP models having white noise latent functions. Further, these inducing kernels are incorporated into the variational inference method of Titsias (2009) (thus addressing point 2) that treats the inducing inputs as well as other quantities associated with the inducing kernels as variational parameters. The whole variational approach provides us with a very flexible, robust to overfitting, approximation framework that overcomes the limitations of the PITC approximation.

4 Sparse variational approximation

In this section, we introduce the concept of variational inducing kernels (VIKs). VIKs give us a way to define more general inducing variables that have larger approximation capacity than the inducing variables used earlier and importantly allow us to deal with white noise latent functions. To motivate the idea, we first explain why the variables can work when the latent functions are smooth and fail when these functions become white noises.

In PITC, we assume each latent function is smooth and we sparsify the GP model through introducing, , inducing variables which are direct observations of the latent function, , at particular input points. Because of the latent function’s smoothness, the variables also carry information about other points in the function through the imposed prior over the latent function. So, having observed we can reduce the uncertainty of the whole function.

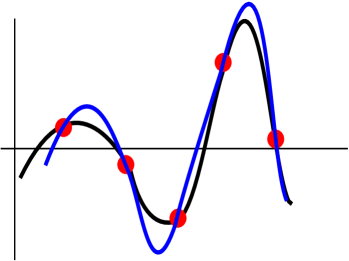

With the vector of inducing variables , if chosen to be sufficiently large relative to the length scales of the latent functions, we can efficiently represent the functions and subsequently variables which are just convolved versions of the latent functions.222This idea is like a “soft version” of the Nyquist-Shannon sampling theorem. If the latent functions were bandlimited, we could compute exact results given a high enough number of inducing points. In general it won’t be bandlimited, but for smooth functions low frecuency components will dominate over high frecuencies, which will quickly fade away. When the reconstruction of from is perfect, the conditional prior becomes a delta function and the sparse PITC approximation becomes exact. Figure 1(a) shows a cartoon description of a summarization of by .

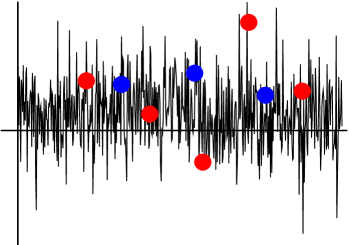

In contrast, when some of the latent functions are white noise processes the sparse approximation will fail. If is white noise333Such a process can be thought as the “time derivative” of the Wiener process. it has a covariance function . Such processes naturally arise in the application of stochastic differential equations (see section 7) and are the ultimate non-smooth processes where two values and are uncorrelated when . When we apply the sparse approximation a vector of “white-noise” inducing variables does not carry information about at any input that differs from all inducing inputs . In other words there is no additional information in the conditional prior over the unconditional prior . Figure 1(b) shows a pictorial representation. The lack of structure makes it impossible to exploit the correlations in the standard sparse methods like PITC.444Returning to our sampling theorem analogy, the white noise process has infinite bandwidth. It is therefore impossible to represent it by observations at a few fixed inducing points.

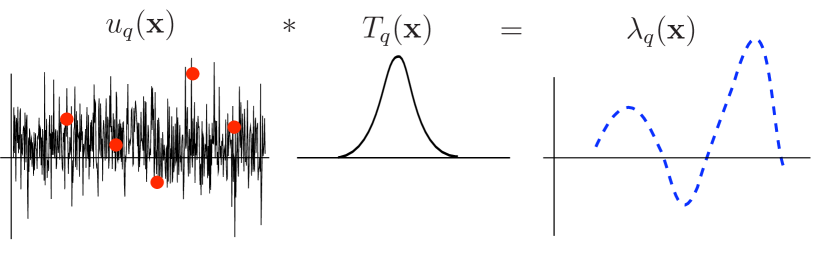

Our solution to this problem is the following. We will define a more powerful form of inducing variable, one based not around the latent function at a point, but one given by the convolution of the latent function with a smoothing kernel. More precisely, let us replace each inducing vector with the variables which are evaluated at the inputs and are defined according to

| (4) |

where is a smoothing kernel (e.g. Gaussian) which we call the inducing kernel (IK). This kernel is not necessarily related to the model’s smoothing kernels. These newly defined inducing variables can carry information about not only at a single input location but from the entire input space. Figure 1(c) shows how the inducing kernel generates the artificial construction , that shares some ligth over the, otherwise, obscure inducing points. We can even allow a separate IK for each inducing point, this is, if the set of inducing points is , then

with the advantage of associating to each inducing point its own set of adaptive parameters in . For the PITC approximation, this adds more hyperparameters to the likelihood, perhaps leading to overfitting. However, in the variational approximation we define all these new parameters as variational parameters and therefore they do not cause the model to overfit. We use the notation to refer to the set of inducing functions .

If has a white noise 555It is straightforward to generalize the method for rough latent functions that are not white noise or to combine smooth latent functions with white noise. GP prior the covariance function for is

| (5) |

and the cross-covariance function between and is

| (6) |

Notice that this cross-covariance function, unlike the case of inducing variables, maintains a weighted integration over the whole input space. This implies that a single inducing variable can properly propagate information from the full-length process into the set of outputs .

5 Variational inference for sparse multiple output Gaussian Processes.

We now extend the variational inference method of Titsias (2009) to deal with multiple outputs and incorporate them into the VIK framework.

We compactly write the joint probability model as . The first step of the variational method is to augment this model with inducing variables. For our purpose, suitable inducing variables are defined through VIKs. More precisely, let be the whole vector of inducing variables where each is a -dimensional vector of values obtained according to eq. (4). The role of is to carry information about the latent function . Each is evaluated at the inputs and has its own VIK, , that depends on parameters . We denote these parameters as .

The variables augment the GP model according to

Here, and is a block diagonal matrix where each block in the diagonal is obtained by evaluating the covariance function in eq. (5) at the inputs . Additionally, where the cross-covariance is computed through eq. (6). Because of the consistency condition , performing exact inference in the above augmented model is equivalent to performing exact inference in the initial GP model. Crucially, this holds for any values of the augmentation parameters . This is the key property that allows us to turn these augmentation parameters into variational parameters by applying approximate sparse inference.

Our method now follows exactly the lines of Titsias (2009) (in appendix A we present a detailed derivation of the bound based on the set of latent functions ). We introduce the variational distribution , where is the conditional GP prior defined earlier and is an arbitrary variational distribution. By minimizing the KL divergence between and the true posterior , we can compute the following Jensen’s lower bound on the true log marginal likelihood:

where is the covariance function associated with the additive noise process and . Note that this bound consists of two parts. The first part is the log of a GP prior with the only difference that now the covariance matrix has a particular low rank form. This form allows the inversion of the covariance matrix to take place in time rather than . The second part can be seen as a penalization term that regulates the estimation of the parameters. Notice also that only the diagonal of the exact covariance matrix needs to be computed. Overall, the computation of the bound can be done efficiently in time.

The bound can be maximized with respect to all parameters of the covariance function; both model parameters and variational parameters. The variational parameters are the inducing inputs and the parameters of each VIK which are rigorously selected so that the KL divergence is minimized. In fact each VIK is also a variational quantity and one could try different forms of VIKs in order to choose the one that gives the best lower bound.

The form of the bound is very similar to the projected process approximation, also known as Deterministic Training Conditional approximation (DTC) (Csató and Opper, 2001; Seeger et al., 2003; Rasmussen and Williams, 2006). However, the bound has an additional trace term that penalizes the movement of inducing inputs away from the data. This term converts the DTC approximation to a lower bound and prevents overfitting. In what follows, we refer to this approximation as DTCVAR, where the VAR suffix refers to the variational framework.

The predictive distribution of a vector of test points, given the training data can also be found to be

with and and . Predictive means can be computed in whereas predictive variances require computation.

6 Experiments

We present results of applying the method proposed for two real-world datasets that will be described in short. We compare the results obtained using PITC, the intrinsic coregionalization model (ICM)666The intrinsic coregionalization model is a particular case of the linear model of coregionalization with one latent function (Goovaerts, 1997). See equation (1) with . employed in (Bonilla et al., 2008) and the method using variational inducing kernels. For PITC we estimate the parameters through the maximization of the approximated marginal likelihood of equation (3) using a scaled-conjugate gradient method. We use one latent function and both the covariance function of the latent process, , and the kernel smoothing function, , follow a Gaussian form, this is

where is a diagonal matrix. For the DTCVAR approximations, we maximize the variational bound . Optimization is also performed using scaled conjugate gradient. We use one white noise latent function and a corresponding inducing function. The inducing kernels and the model kernels follow the same Gaussian form as in the PITC case. Using this form for the covariance or kernel, all convolution integrals are solved analytically.

6.1 Exam score prediction

In this experiment the goal is to predict the exam score obtained by a particular student belonging to a particular school. The data comes from the Inner London Education Authority (ILEA).777Data is available at http://www.cmm.bristol.ac.uk/learning-training/multilevel-m-support/datasets.shtml It consists of examination records from 139 secondary schools in years 1985, 1986 and 1987. It is a random sample with 15362 students. The input space consists of features related to each student and features related to each school. From the multiple output point of view, each school represents one output and the exam score of each student a particular instantiation of that output.

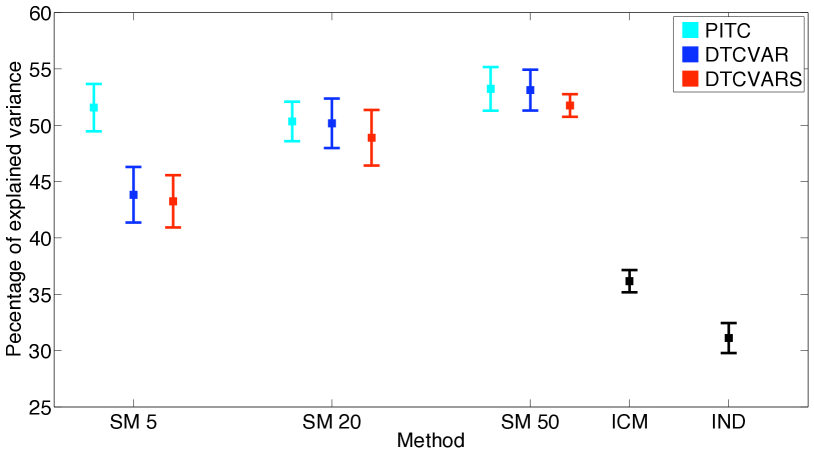

We follow the same preprocessing steps employed in (Bonilla et al., 2008). The only features used are the student-dependent ones (year in which each student took the exam, gender, VR band and ethnic group), which are categorial variables. Each of them is transformed to a binary representation. For example, the possible values that the variable year of the exam can take are 1985, 1986 or 1987 and are represented as , or . The transformation is also applied to the variables gender (two binary variables), VR band (four binary variables) and ethnic group (eleven binary variables), ending up with an input space with dimension . The categorial nature of data restricts the input space to unique input feature vectors. However, two students represented by the same input vector and belonging both to the same school , can obtain different exam scores. To reduce this noise in the data, we follow Bonilla et al. (2008) in taking the mean of the observations that, within a school, share the same input vector and use a simple heteroskedastic noise model in which the variance for each of these means is divided by the number of observations used to compute it. The performance measure employed is the percentage of explained variance defined as the total variance of the data minus the sum-squared error on the test set as a percentage of the total data variance. It can be seen as the percentage version of the coefficient of determination between the test targets and the predictions. The performance measure is computed for ten repetitions with of the data in the training set and of the data in the test set.

Figure 2 shows results using PITC, DTCVAR with one smoothing kernel and DTCVAR with as many inducing kernels as inducing points (DTCVARS in the figure). For inducing points all three alternatives lead to approximately the same results. PITC keeps a relatively constant performance for all values of inducing points, while the DTCVAR approximations increase their performance as the number of inducing points increase. This is consistent with the expected behaviour of the DTCVAR methods, since the trace term penalizes the model for a reduced number of inducing points. Notice that all the approximations outperform independent GPs and the best result of the intrinsic coregionalization model presented in (Bonilla et al., 2008).

6.2 Compiler prediction performance.

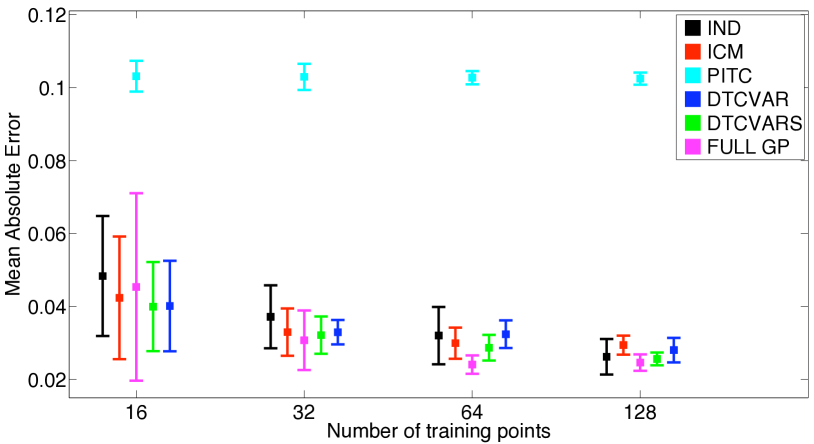

In this dataset the outputs correspond to the speed-up of 11 C programs after some transformation sequence has been applied to them. The speed-up is defined as the execution time of the original program divided by the execution time of the transformed program. The input space consists of 13-dimensional binary feature vectors, where the presence of a one in these vectors indicates that the program has received that particular transformation. The dataset contains 88214 observations for each output and the same number of input vectors. All the outputs share the same input space. Due to technical requirements, it is important that the prediction of the speed-up for the particular program is made using few observations in the training set. We compare our results to the ones presented in (Bonilla et al., 2008) and use , , and for the training set. The remaining observations are used for testing, employing as performance measure the mean absolute error. The experiment is repeated ten times and standard deviations are also reported. We only include results for the average performance over the 11 outputs.

Figure 3 shows the results of applying independent GPs (IND in the figure), the intrinsic coregionalization model (ICM in the figure), PITC, DTCVAR with one inducing kernel (DTCVAR in the figure) and DTCVAR with as many inducing kernels as inducing points (DTCVARS in the figure). Since the training sets are small enough, we also include results of applying the GP generated using the full covariance matrix of the convolution construction (see FULL GP in the figure). We repeated the experiment for different values of , but show results only for . Results for ICM and IND were obtained from (Bonilla et al., 2008).

In general, the DTCVAR variants outperform the ICM method, and the independent GPs for and . In this case, using as many inducing kernels as inducing points improves in average the performance. All methods, including the independent GPs are better than PITC. The size of the test set encourages the application of the sparse methods: for , making the prediction of the whole dataset using the full GP takes in average minutes while the prediction with DTCVAR takes minutes. Using more inducing kernels improves the performance, but also makes the evaluation of the test set more expensive. For DTCVARS, the evaluation takes in average minutes. Time results are average results over the ten repetitions.

7 Stochastic Latent Force Models for Financial Data

The starting point of stochastic differential equations is a stochastic version of the equation of motion, which is called Langevin’s equation:

| (7) |

where is the velocity of the particle, is a systematic friction term, is a random fluctuation external force, i.e. white noise, and indicates the sensitivity of the ouput to the random fluctuations. In the mathematical probability literature, the above is written more rigorously as where is the Wiener process (standard Brownian motion). Since is a Gaussian process and the equation is linear, must be also a Gaussian process which turns out to be the Ornstein-Uhlenbeck (OU) process.

Here, we are interested in extending the Langevin equation to model multivariate time series. The way that the model in (7) is extended is by adding more output signals and more external forces. The forces can be either smooth (systematic or drift-type) forces or white noise forces. Thus, we obtain

| (8) |

where is the th output signal. Each can be either a smooth latent force that is assigned a GP prior with covariance function or a white noise force that has a GP prior with covariance function . That is, we have a composition of latent forces, where of them correspond to smooth latent forces and correspond to white noise processes. The intuition behind this combination of input forces is that the smooth part can be used to represent medium/long term trends that cause a departure from the mean of the output processes, whereas the stochastic part is related to short term fluctuations around the mean. A model that employs and was proposed by Lawrence et al. (2007) to describe protein transcription regulation in a single input motif (SIM) gene network.

Solving the differential equation (8), we obtain

where arises from the initial condition. This model now is a special case of the multioutput regression model discussed in sections 1 and 2 where each output signal has a mean function and each model kernel is equal to . The above model can be also viewed as a stochastic latent force model (SLFM) following the work of Álvarez et al. (2009).

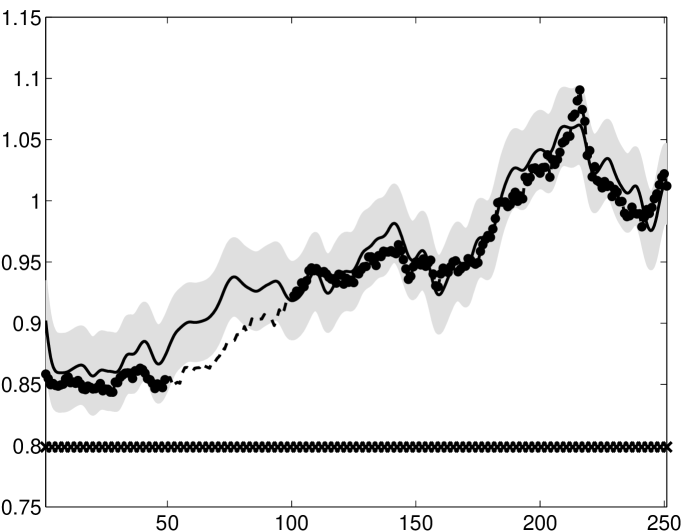

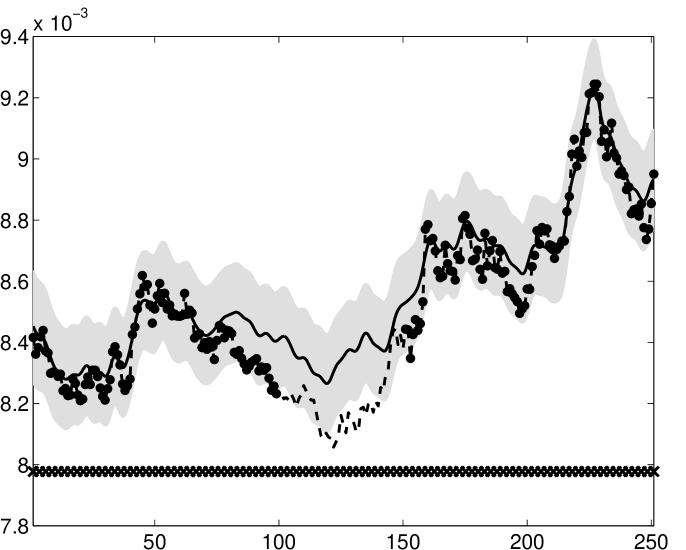

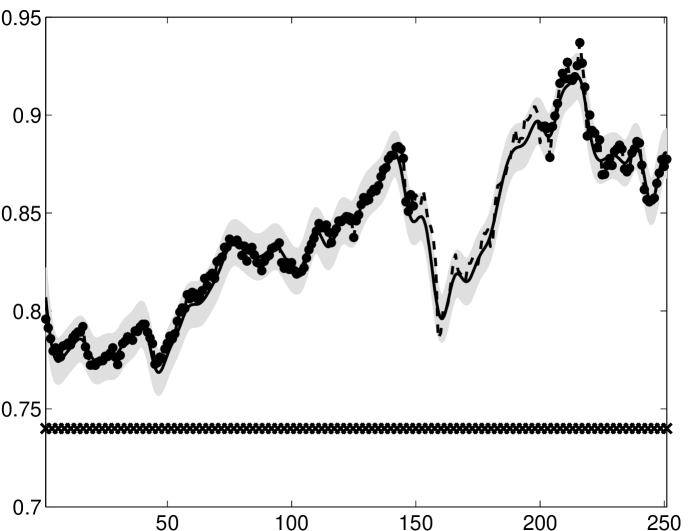

Latent market forces

The application considered is the inference of missing data in a multivariate financial data set: the foreign exchange rate w.r.t. the dollar of 10 of the top international currencies (Canadian Dollar [CAD], Euro [EUR], Japanese Yen [JPY], Great British Pound [GBP], Swiss Franc [CHF], Australian Dollar [AUD], Hong Kong Dollar [HKD], New Zealand Dollar [NZD], South Korean Won [KRW] and Mexican Peso [MXN]) and 3 precious metals (gold [XAU], silver [XAG] and platinum [XPT]).888Data is available at http://fx.sauder.ubc.ca/data.html). We considered all the data available for the calendar year of 2007 (251 working days). In this data there are several missing values: XAU, XAG and XPT have 9, 8 and 42 days of missing values respectively. On top of this, we also introduced artificially long sequences of missing data. Our objective is to model the data and test the effectiveness of the model by imputing these missing points. We removed a test set from the data by extracting contiguous sections from 3 currencies associated with very different geographic locations: we took days 50–100 from CAD, days 100–150 from JPY and days 150–200 from AUD. The remainder of the data comprised the training set, which consisted of 3051 points, with the test data containing 153 points. For preprocessing we removed the mean from each output and scaled them so that they all had unit variance.

It seems reasonable to suggest that the fluctuations of the 13 correlated financial time-series are driven by a smaller number of latent market forces. We therefore modelled the data with up to six latent forces which could be noise or smooth GPs. The GP priors for the smooth latent forces are assumed to have a squared exponential covariance function,

where the hyperparameter is known as the lengthscale.

We present an example with . For this value of , we consider all the possible combinations of and . The training was performed in all cases by maximizing the variational bound using the scale conjugate gradient algorithm until convergence was achieved. The best performance in terms of achiving the highest value for was obtained for and . We compared against the LMC model for different values of the latent functions in that framework. While our best model resulted in an standardized mean square error of , the best LMC (with =2) resulted in . We plotted predictions from the latent market force model to characterize the performance when filling in missing data. In figure 4 we show the output signals obtained using the model with the highest bound ( and ) for CAD, JPY and AUD. Note that the model performs better at capturing the deep drop in AUD than it does at capturing fluctuations in CAD and JPY.

8 Conclusions

We have presented a variational approach to sparse approximations in convolution processes. Our main focus was to provide efficient mechanisms for learning in multiple output Gaussian processes when the latent function is fluctuating rapidly. In order to do so, we have introduced the concept of inducing function, which generalizes the idea of inducing point, traditionally employed in sparse GP methods. The approach extends the variational approximation of Titsias (2009) to the multiple output case. Using our approach we can perform efficient inference on latent force models which are based around stochastic differential equations, but also contain a smooth driving force. Our approximation is flexible enough and has been shown to be applicable to a wide range of data sets, including high-dimensional ones.

Acknowledgements

The authors would like to thank Edwin Bonilla for his valuable feedback with respect to the exam score prediction example and the compiler dataset example. We also thank the authors of Bonilla et al. (2008) who kindly made the compiler dataset available. DL has been partly financed by Comunidad de Madrid (project PRO-MULTIDIS-CM, S-0505/TIC/0233), and by the Spanish government (CICYT project TEC2006-13514-C02-01 and researh grant JC2008-00219). MA and NL have been financed by a Google Research Award “Mechanistically Inspired Convolution Processes for Learning” and MA, NL and MT have been financed by EPSRC Grant No EP/F005687/1 “Gaussian Processes for Systems Identification with Applications in Systems Biology”.

A Variational Inducing Kernels

Recently, a method for variational sparse approximation for Gaussian processes learning was introduced in Titsias (2009). In this appendix, we apply this methodology to a multiple output Gaussian process where the outputs have been generated through a so called convolution process. For learning the parameters of the kernels involved, a lower bound for the true marginal can be maximized. This lower bound has similar form to the marginal likelihood of the Deterministic Training Conditional (DTC) approximation plus an extra term which involves a trace operation. The computational complexity grows as where is the number of data points per output, is the number of outputs and the number of inducing variables.

A.1 Computation of the lower bound

Given target data and inputs , the marginal likelihood of the original model is given by integrating over the latent function999Strictly speaking, the distributions associated to correspond to random signed measures, in particular, Gaussian measures.

The prior over is expressed as

The augmented joint model can then be expressed as

With the inducing function , the marginal likelihood takes the form

Using Jensen’s inequality, we use the following variational bound on the log likelihood,

where we have introduced as the variational approximation to the posterior. Following Titsias (2009) we now specify that the variational approximation should be of the form

We can write our bound as

To compute this bound we first consider the integral

Since this is simply the expectation of a Gaussian under a Gaussian we can compute the result analytically as follows

We need to compute and . is a vector with elements

Assuming that the latent functions are independent GPs, . Then

can be expressed as

On the other hand, is a matrix with elements

With independent GPs the term can be expressed as

In this way

with .

The expression for is given as

The variational lower bound is now given as

| (9) |

A free form optimization over could now be performed, but it is far simpler to reverse Jensen’s inequality on the first term, we then recover the value of the lower bound for optimized without ever having to explicitly optimise . Reversing Jensen’s inequality, we have

The form of which leads to this bound can be found as

with and .

A.2 Predictive distribution

The predictive distribution for a new test point given the training data is also required. This can be expressed as

Using the Gaussian form for the we can compute

Which allows us to write the predictive distribution as

with and .

A.3 Optimisation of the Bound

Optimisation of the bound (with respect to the variational parameters and the parameters of the covariance functions) can be carried out through gradient based methods. We follow the notation of Brookes (2005) obtaining similar results to Lawrence (2007). This notation allows us to apply the chain rule for matrix derivation in a straight-forward manner. The resulting gradients can then be combined with gradients of the covariance functions with respect to their parameters to optimize the model.

Let’s define , where is the vectorization operator over the matrix . For a function the equivalence between and is given through . The log-likelihood function is given as

where . Using the matrix inversion lemma and its equivalent form for determinants, the above expression can be written as

up to a constant. We can find and applying the chain rule to obtaining expressions for , and and combining those with the relevant derivatives of the covariances wrt , and the parameters associated to the model kernels,

| (10) |

where the subindex in stands for those terms of which depend on , is either , or and is zero if is equal to and one in other case. For convenience we have used . Next we present expressions for each partial derivative

where , and is a vectorized transpose matrix (Brookes, 2005) and we have not included its dimensions to keep the notation clearer. We can replace the above expressions in (10) to find the corresponding derivatives, so

We also have

Finally, results for and are obtained as

References

- Álvarez and Lawrence (2009) Mauricio Álvarez and Neil D. Lawrence. Sparse convolved Gaussian processes for multi-output regression. In NIPS, volume 21, pages 57–64. MIT Press, Cambridge, MA, 2009.

- Álvarez et al. (2009) Mauricio Álvarez, David Luengo, and Neil D. Lawrence. Latent Force Models. In van Dyk and Welling (2009), pages 9–16.

- Bishop (2006) Christopher M. Bishop. Pattern Recognition and Machine Learning. Information Science and Statistics. Springer, 2006.

- Bonilla et al. (2008) Edwin V. Bonilla, Kian Ming Chai, and Christopher K. I. Williams. Multi-task Gaussian process prediction. In John C. Platt, Daphne Koller, Yoram Singer, and Sam Roweis, editors, NIPS, volume 20, Cambridge, MA, 2008. MIT Press.

- Boyle and Frean (2005) Phillip Boyle and Marcus Frean. Dependent Gaussian processes. In Lawrence Saul, Yair Weiss, and Léon Bouttou, editors, NIPS, volume 17, pages 217–224, Cambridge, MA, 2005. MIT Press.

- Brookes (2005) Michael Brookes. The matrix reference manual. Available on-line., 2005. http://www.ee.ic.ac.uk/hp/staff/dmb/matrix/intro.html.

- Csató and Opper (2001) Lehel Csató and Manfred Opper. Sparse representation for Gaussian process models. In Todd K. Leen, Thomas G. Dietterich, and Volker Tresp, editors, NIPS, volume 13, pages 444–450, Cambridge, MA, 2001. MIT Press.

- Evgeniou et al. (2005) Theodoros Evgeniou, Charles A. Micchelli, and Massimiliano Pontil. Learning multiple tasks with kernel methods. Journal of Machine Learning Research, 6:615–637, 2005.

- Gao et al. (2008) Pei Gao, Antti Honkela, Magnus Rattray, and Neil D. Lawrence. Gaussian process modelling of latent chemical species: Applications to inferring transcription factor activities. Bioinformatics, 24:i70–i75, 2008. doi: 10.1093/bioinformatics/btn278.

- Goovaerts (1997) Pierre Goovaerts. Geostatistics For Natural Resources Evaluation. Oxford University Press, USA, 1997.

- Higdon (2002) David M. Higdon. Space and space-time modelling using process convolutions. In C. Anderson, V. Barnett, P. Chatwin, and A. El-Shaarawi, editors, Quantitative methods for current environmental issues, pages 37–56. Springer-Verlag, 2002.

- Journel and Huijbregts (1978) Andre G. Journel and Charles J. Huijbregts. Mining Geostatistics. Academic Press, London, 1978. ISBN 0-12391-050-1.

- Lawrence (2007) Neil D. Lawrence. Learning for larger datasets with the Gaussian process latent variable model. In Marina Meila and Xiaotong Shen, editors, AISTATS 11, San Juan, Puerto Rico, 21-24 March 2007. Omnipress.

- Lawrence et al. (2003) Neil D. Lawrence, Matthias Seeger, and Ralf Herbrich. Fast sparse Gaussian process methods: The informative vector machine. In Sue Becker, Sebastian Thrun, and Klaus Obermayer, editors, NIPS, volume 15, pages 625–632, Cambridge, MA, 2003. MIT Press.

- Lawrence et al. (2007) Neil D. Lawrence, Guido Sanguinetti, and Magnus Rattray. Modelling transcriptional regulation using Gaussian processes. In Bernhard Schölkopf, John C. Platt, and Thomas Hofmann, editors, NIPS, volume 19, pages 785–792. MIT Press, Cambridge, MA, 2007.

- Lázaro-Gredilla and Figueiras-Vidal (2010) Miguel Lázaro-Gredilla and Aníbal Figueiras-Vidal. Inter-domain Gaussian processes for sparse inference using inducing features. In NIPS, volume 22, pages 1087–1095. MIT Press, Cambridge, MA, 2010.

- Osborne et al. (2008) Michael A. Osborne, Alex Rogers, Sarvapali D. Ramchurn, Stephen J. Roberts, and Nicholas R. Jennings. Towards real-time information processing of sensor network data using computationally efficient multi-output Gaussian processes. In Proceedings of the International Conference on Information Processing in Sensor Networks (IPSN 2008), 2008.

- Quiñonero Candela and Rasmussen (2005) Joaquin Quiñonero Candela and Carl Edward Rasmussen. A unifying view of sparse approximate Gaussian process regression. Journal of Machine Learning Research, 6:1939–1959, 2005.

- Rasmussen and Williams (2006) Carl Edward Rasmussen and Christopher K. I. Williams. Gaussian Processes for Machine Learning. MIT Press, Cambridge, MA, 2006. ISBN 0-262-18253-X.

- Seeger et al. (2003) Matthias Seeger, Christopher K. I. Williams, and Neil D. Lawrence. Fast forward selection to speed up sparse Gaussian process regression. In Christopher M. Bishop and Brendan J. Frey, editors, Proceedings of the Ninth International Workshop on Artificial Intelligence and Statistics, Key West, FL, 3–6 Jan 2003.

- Snelson and Ghahramani (2006) Edward Snelson and Zoubin Ghahramani. Sparse Gaussian processes using pseudo-inputs. In Yair Weiss, Bernhard Schölkopf, and John C. Platt, editors, NIPS, volume 18, Cambridge, MA, 2006. MIT Press.

- Teh et al. (2005) Yee Whye Teh, Matthias Seeger, and Michael I. Jordan. Semiparametric latent factor models. In Robert G. Cowell and Zoubin Ghahramani, editors, AISTATS 10, pages 333–340, Barbados, 6-8 January 2005. Society for Artificial Intelligence and Statistics.

- Titsias (2009) Michalis K. Titsias. Variational learning of inducing variables in sparse Gaussian processes. In van Dyk and Welling (2009), pages 567–574.

- van Dyk and Welling (2009) David van Dyk and Max Welling, editors. AISTATS, Clearwater Beach, Florida, 16-18 April 2009. JMLR W&CP 5.