∎

Nonparametric estimation for a stochastic volatility model.

Abstract

Consider discrete time observations of the process satisfying , with a one-dimensional positive diffusion process independent of the Brownian motion . For both the drift and the diffusion coefficient of the unobserved diffusion , we propose nonparametric least square estimators, and provide bounds for their risk. Estimators are chosen among a collection of functions belonging to a finite dimensional space whose dimension is selected by a data driven procedure. Implementation on simulated data illustrates how the method works.

Keywords:

Diffusion coefficient Drift Mean square estimator Model selection Nonparametric estimation Penalized contrast Stochastic volatilityMSC:

62G08 62M05 62P05Corresponding author: F. Comte, MAP5 UMR 8145,

Université Paris Descartes,

45 rue des Saints-Pères,

75270 Paris cedex 06, FRANCE.

email: fabienne.comte@univ-paris5.fr

1 Introduction

In this paper, we consider a bivariate process with dynamics described by the following equations:

| (1) |

where is a standard bidimensional Brownian motion and is independent of . Our aim is to propose and study nonparametric estimators of and on the basis of discrete time observations of the process only.

Model (1) was introduced by Hull and White (1987) under the name of Stochastic Volatility model. It is often adopted in finance to model stock prices, stock indexes or short term interest rates: see for instance Hull and White (1987), Anderson and Lund (1997), the review of Stochastic Volatility models in Ghysels et al. (1996) or the recent book by Shephard (2005) and the references therein. See also an econometric analysis of the subject in Barndorff-Nielsen and Shephard (2002).

The approach to study model (1) is often parametric: the unknown functions are specified up to a few unknown parameters, see the popular examples of Heston (1993) or Cox, Ingersoll and Ross (1985). General statistical parametric approaches of the problem are studied in Genon-Catalot et al. (1999), Hoffmann (2002), Gloter (2007), Aït-Sahalia and Kimmel (2007). A nonparametric estimation of the stationary density of is studied in Comte and Genon-Catalot (2006). A recent proposal for nonparametric estimation of the drift and diffusion coefficients of can be found in Renó (2006), who studies the empirical performance of a Nadaraya-Watson kernel strategy on two parametric simulated examples. Our approach is new and different, and it is based on a nonparametric mean square strategy. We consider the same probabilistic and sampling settings as Gloter (2007) and follow the ideas developed in Comte et al. (2006, 2007), where direct or integrated discrete observations of the process are considered. Here, our assumptions ensure that is stationary and we consider discrete time observations of the process in the so-called high frequency context: is small, is large and , the time interval where observations are taken, is large.

We assume that and define as it is usual, for , the realized quadratic variation associated with :

Setting , provides an approximation of the integrated volatility:

| (2) |

which in turn may be, for well chosen , a satisfactory approximation of . We have in mind to obtain regression-type equations, for :

where

| (3) |

Choosing a collection of finite dimensional spaces, we use the regression-type equations to construct estimators on these spaces. Then, we propose a data driven procedure to select a relevant estimation space in the collection. As it is usual with these methods, the risk of an estimator of or is measured via where . We obtain risk bounds which can be interpreted as tend to infinity, tend to 0 and tends to infinity. These bounds are compared with Hoffmann’s (1999) minimax rates in the case of direct observations of . For what concerns , our method leads to the best rate that can be expected. For what concerns , no benchmark is available in this asymptotic framework. Indeed, Gloter (2000) and Hoffmann (2002) only treat the case of observations within a fixed length time interval, in a parametric setting. As it is always the case, the rates are different for the two functions.

The paper is organized as follows. Section 2 describes the assumptions on the model and the collection of estimation spaces. In Section 3, the estimators are defined and their risks are studied. Section 4 completes the procedure by the data driven selection of the estimation space. Examples of models and simulation results are presented in Section 5. Lastly, proofs are gathered in Section 6.

2 The assumptions

2.1 Model assumptions.

Let be given by (1) and assume that only discrete time observations of , are available. We want to estimate the drift function and the square of the diffusion coefficient when is stationary and exponentially -mixing. We assume that the state space of is a known open interval of and consider the following set of assumptions.

-

[A1

] , , with , for all . Let . The function belongs to , is bounded on , , is Lipschitz on I, is bounded on and for all in .

-

[A2

] For all , the scale density satisfies , and the speed density satisfies .

-

[A3

] and , where .

-

[A4

] The process is exponentially -mixing, i.e., there exist constants , such that, for all , .

Under [A1]-[A3], is strictly stationary with marginal distribution , ergodic and -mixing, i.e. . Here, denotes the -mixing coefficient of and is given by

The norm is the total variation norm and denotes the transition probability of (see Genon-Catalot et al. (2000)). To prove our main result, we need the stronger mixing condition [A4], which is satisfied in most standard examples. Under [A1]-[A4], for fixed , is a strictly stationary process. And we have:

Proposition 2.1

Under [A1]-[A4], for fixed and , is strictly stationary and for all .

2.2 Spaces of approximation

The functions and are estimated only on a compact subset of the state space . For simplicity and without loss of generality, we assume from now on that

| (4) |

To estimate , we consider a family of finite dimensional subspaces of and compute a collection of estimators where for all , belongs to . Afterwards, a data driven procedure chooses among the collection of estimators the final estimator .

We consider here simple projection spaces, namely trigonometric spaces, . The space is linearly spanned in by with , for even ’s and for odd ’s larger than 1. We have and . The largest space in the collection has maximal dimension , which is subject to constraints appearing later.

Actually, the theory requires smooth bases and regular wavelet bases would also be adequate.

In connection with the collection of spaces , we need an additional assumption on the marginal density of the stationary process :

-

[A5

] The process admits a stationary density and there exist two positive constants and (independent of ) such that , ,

(5)

3 Mean squares estimators of the drift and volatility

3.1 Regression equations

Reminding of (3), we first prove the developments, for :

| (7) |

where the ’s are noise terms (with martingale properties) and the ’s are negligible residual terms given in Section 6. For the noise terms, we have, for ():

with

| (8) |

and

Note that .

On the other hand, for (), we have with

where is given in (8), and

3.2 Mean squares contrast

Equation (7) gives a natural regression equation to estimate . In light of this, we consider the following contrast, for a function where is a space of the collection and for :

| (9) |

Then the estimators are defined as

| (10) |

The minimization of over usually leads to several solutions. In contrast, the random -vector is always uniquely defined. Indeed, let us denote by the orthogonal projection (with respect to the inner product of ) onto the subspace of , , then where . This is the reason why we consider a properly defined risk for based on the design points, i.e.

Thus, the error is measured via the risk where

Let us mention that for a deterministic function

. Moreover, under Assumption [A5],

the norms and are equivalent for functions in (see notations (6)).

The following decomposition of the contrast holds:

In view of (7), we define the centered empirical processes, for :

and the residual process:

Then we obtain that

Let be the orthogonal projection of on . Write simply that by definition of the estimator, and therefore that . This yields

The functions and being -supported, we can cancel the terms that appears in both sides of the inequality. Therefore, we get

| (11) |

Taking expectations and finding upper bounds for

will give the rates for the risks of the estimators.

3.3 Risk for the collection of drift estimators

For the estimation of , we obtain the following result.

Proposition 3.1

Assume that and . Assume that [A1]-[A5] hold and consider a model in the collection of models with where is the maximal dimension (see Section 2.2). Then the estimator of is such that

| (12) |

where and and are some positive constants.

Note that the condition on implies that must be large enough.

It follows from (12) that it is natural to

select the dimension that leads to the best

compromise between the squared bias term

(which decreases when increases) and the variance term of

order .

Now, let us consider the classical high frequency data setting: let , and be, in addition, such that , , when and that . Assume for instance that belongs to a ball of some Besov space, , , and that , then , for (see Lemma 12 in Barron et al. (1999)). Therefore, if we choose , we obtain

| (13) |

The first term is the optimal nonparametric rate proved by Hoffmann (1999) for direct observation of .

Now, let us find conditions under which the last term is negligible. For instance, under the standard condition , the term is negligible with respect to .

Now, consider the choices and . Let us see if there are possible choices of for which all our constraints are fulfilled. To have requires . As , we have and . Thus, and . Finally, the last constraint to fulfill is that . Thus for , the dominating term in (13) is , i.e. the minimax optimal rate. We have obtained a possible “bandwidth” of steps .

3.4 Risk for the collection of volatility estimators

For the collection of volatility estimators, we have the result

Proposition 3.2

Assume that [A1]-[A5] hold and consider a model in the collection of models with maximal dimension . Assume also that and , . Then the estimator of is such that

| (14) |

where the residual term is given by

| (15) |

where , and , are some positive constants.

The discussion on rates is much more tedious. Consider the asymptotic setting described for . Assume that belongs to a ball of some Besov space, , and that , then , for . Therefore, if we choose , and , we obtain

| (16) |

The first term is the optimal nonparametric rate proved by Hoffmann (1999) when discrete time observations of are available.

For the second term, let us set , , , and recall that and , so that and . We look for such that

For this, we take which implies . We get

Then we impose which is equivalent to

Next leads to

Lastly holds for , i.e. .

The optimal dimension has also to fulfill i.e. which implies . Finally, we must have

This interval is nonempty as soon as .

In terms of the initial number of observations, the rate is now where is at most , when . This is consistent with Gloter’s (2000) result: in the parametric case, he obtains instead of for the quadratic risk.

4 Data driven estimator of the coefficients

The second step is to ensure an automatic selection of , which does not use any knowledge on , and in particular which does not require to know the regularity . This selection is standardly done by setting

| (17) |

with pen a penalty to be properly chosen. We denote by the resulting estimator and we need to determine pen such that, ideally,

with a constant which should not be too large.

4.1 Result for the data driven estimator of

We almost reach this aim for the estimation of .

Theorem 4.1

Assume that [A1]-[A5] hold, , and . Consider the collection of models with maximal dimension . Then the estimator of where is defined by (17) with

| (18) |

where is a universal constant, is such that

| (19) |

For comments on the practical calibration of the penalty, see Section 5.2.

It follows from (19) that the adaptive estimator automatically realizes the bias-variance compromise, provided that the last terms can be neglected as discussed above. Here, the bandwidth for the choices of is slightly narrowed because of a stronger constraint. More precisely, we choose (instead of 1 previously), that is , so that . Therefore and if , then . Also, , , . Hence if , we have altogether: , tend to infinity with , , tend to zero.

In that case, whenever belongs to some Besov ball (see (13)), and if , then achieves the optimal corresponding nonparametric rate. Note that, in the parametric framework, Gloter (2007) obtains an efficient estimation of in the same asymptotic context.

4.2 Result for the data driven estimator of the volatility

We can prove the following Theorem.

Theorem 4.2

Assume that [A1]-[A5] hold, , and . Consider the collection of models with maximal dimension . Then the estimator of where is defined by (17) with

| (20) |

where is a universal constant, is such that

| (21) |

where

| (22) |

Now, if belongs to a ball of some Besov space, , then automatically,

without requiring the knowledge of . Therefore,

It remains to study the residual term. Notice that we do not know the optimal minimax rate for estimating , under our set of assumptions on the models and on the asymptotic framework. However, Gloter (2000) and Hoffmann (2002), with observations within a fixed length time interval, obtain the parametric rate (in variance). Taking this as a benchmark, we try to make the residual less than . Let us set , , hence and . This yields that must all be less than or equal to , in association with and . This set of constraint is not empty (e.g. fits).

5 Examples and numerical simulation results

In this section, we consider examples of diffusions and implement the estimation algorithm on simulated data for the stochastic volatility model given by (1).

5.1 Simulated paths

We consider the processes for specified by the couples of functions , :

-

1.

which corresponds to for an Ornstein-Uhlenbeck process, . Whatever the chosen step, is exactly simulated as an autoregressive process of order 1. We took and .

-

2.

, , where and are the diffusion coefficients of the process (th, with the same parameters as for case . The process corresponds to th which is a positive bounded process.

-

3.

and which corresponds to the process .

-

4.

which corresponds to the Cox-Ingersoll-Ross process. A discrete time sample is obtained in an exact way by taking the Euclidean norm of a -dimensional Ornstein-Uhlenbeck process with parameters and . We took , and .

We obtain samples of discrete observations of the processes for with , , from which we generate , by using that

with i.i.d. independent of . Approximations of the integrated processes are computed by discrete integration (with a trapeze method).

The generated , samples have length , for a step , and the integrated process is computed using 10 data, therefore, we obtain and , for . Different values of are used, but the best value, , corresponds to and data for the same .

5.2 Estimation algorithms and numerical results

| mean | ||||||

|---|---|---|---|---|---|---|

| (std) | () | () | () | () | () | |

| mean | ||||||

| (std) | () | () | () | () | () |

| Process | [T] | [T] | [T] | [T] | [GP] | |

|---|---|---|---|---|---|---|

| mean | ||||||

| (std) | () | () | () | () | () | |

| mean | ||||||

| (std) | () | () | () | () | () |

We use the algorithm of Comte and Rozenholc (2004). The precise calibration of penalties is difficult and done for the trigonometric basis but also for a general piecewise polynomial basis, described in detail in Comte et al (2006). Additive correcting terms are involved in the penalty. Such terms avoid under-penalization and are in accordance with the fact that the theorems provide lower bounds for the penalty. The correcting terms are asymptotically negligible and do not affect the rate of convergence. For the trigonometric polynomial collection (denoted by [T]), the drift penalty and the diffusion penalty are given by

For the penalty when considering general piecewise polynomial bases (denoted by [GP]), we refer the reader to Comte et al. (2006).

|

|

The constants and in both drift and diffusion penalties have been set equal to 2. The term replaces for the estimation of and replaces for the estimation of . Let us first explain how is obtained. We run once the estimation algorithm of with the basis [T] and with a preliminary penalty where is taken equal to . This gives a preliminary estimator . Afterwards, we take equal to twice the 99.5%-quantile of . The use of the quantile is here to avoid extreme values. We get . We use this estimate and set for the penalty of .

|

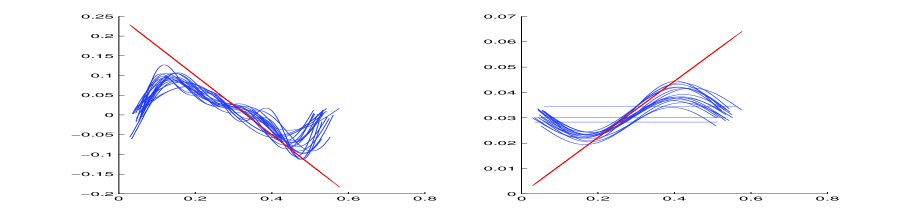

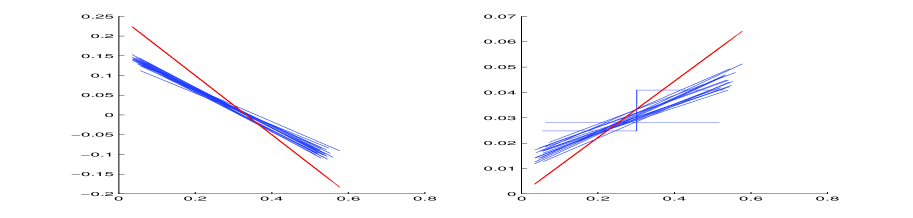

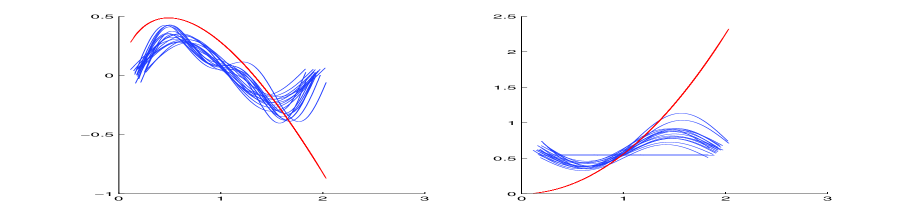

The results given by our algorithm are described in Figure 1 and 2. We plot in Figure 1 the true function (thick curve) and 20 estimated functions (thin curves) in the case and when using first the basis [T] and then the basis [GP], in the case of the CIR process. We can see that the trigonometric basis finds the right slope in the central part of the interval, whereas the basis [GP] in general selects only one bin and a straight curve, but with a slightly too small slope. The same type of result holds in Figure 2 for the exponential Orsntein Uhlenbeck process. For comparison with direct or integrated observations of , we refer to Comte et al. (2006,2007). It is not surprising that in the case of a stochastic volatility model, empirical results are less satisfactory and require a large number of observations.

We also give in Tables 1 and 2 results of Monte-Carlo type experiments. In Table 1, we show the results of the estimation procedure with the basis [T] and the CIR process when choosing different values of for building the quadratic variation. Clearly, there is an optimal value. If is too large, there are not enough observations left for the estimation algorithm. If is too small, bias phenomena appear, related to the violation of the theoretical assumptions (mainly ). We repeated the experiment for the other processes and obtained analogous results. In general, for this sample size, the choice seems to be relevant. In Table 2, we can see from the last two columns that the basis [GP] seems to be better than [T], at least for the CIR process. The errors are computed as the mean over 100 simulated paths of the empirical errors (e.g. for ).

6 Discussion on the assumptions and proofs

6.1 Proof of Proposition 2.1

We start with some preliminaries. Let . The joint process is a two dimensional diffusion satisfying:

Under regularity assumptions on and , this process admits a transition density, say for the conditional density of given , . This density is w.r.t. the Lebesgue measure on (see Rogers and Williams (2000)). We assume that these assumptions hold.

Now, let us set

| (23) |

The discrete time process is strictly stationary and Markov. Its one step transition operator is given by the density:

Its stationary density is given by .

Let us set, for ,

| (24) |

and define by the relation: . Conditionally on , the random variables (r.v.) are independent and has distribution . Consequently, the r.v are i.i.d. with distribution and the sequence is independent of . Hence and are strictly stationary processes.

From the preliminaries and the above remarks, we deduce that the process is stationary Markov. Its -step transition operator is given by:

where is the -step transition density of and is the standard gaussian density. The stationary density of is . Hence

We may now use the representation of the -mixing coefficient of strictly stationary Markov processes (see e.g. Genon-Catalot et al. (2000)) to compute

Now, we have . Finally,

6.2 Discussion on the assumptions

Actually, Assumption [A3] is too strong. We only need the existence of moments up to a certain order. Let us now discuss [A5]. Using the representation

we see that has a conditional density given . Integrating this density w.r.t. the distribution of , we get that has a density . However the formula for is untractable.

On the other hand, we can obtain (5) by another approach. We have

Now we use that, for any , there exists some constant such that

Noting that , we get . On the other hand,

It follows that . Next,

By Gloter’s (2007) Proposition 3.1, we have and . Hence

Since

As there exist two positive constants , such that , , we obtain

Under the constraint that , we get (5) for large enough. This constraint is compatible with the other ones, see the discussion after Theorem 4.1.

6.3 Definition of the residuals and their properties

We have

where is the residual term for studied in Comte et al. (2006, Proposition 3.1) and defined by

On the other hand,

where is the residual term for studied in Comte et al. (2006, Propositions 4.1, 4.2 and 4.3) defined by with

where . This decomposition is

obtained by applying Ito’s formula and Fubini’s theorem.

We may now summarize the following useful results, proved in Comte et

al. (2006, Propositions 3.1, 4.1, 4.2 and 4.3):

Lemma 6.1

Under Assumptions [A1]-[A2]-[A3],

-

1.

For , for , for all , where is a constant.

-

2.

Let . For all , .

-

3.

For all , and .

We also need the following result:

Lemma 6.2

Under assumptions [A1]-[A3], for any integer , and .

Proof of Lemma 6.2. This follows from Proposition 3.1 p.504 in Gloter (2007).

6.4 Proof of Propositions 3.1 and 3.2

For sake of brevity, we give both proofs at the same time. The main difference lies in the orders of the expectations and in the appearance of a specific term in the study of the estimator of . Let us thus define for as and

Moreover let and

Let us consider the set

| (25) |

On , . From (11), we deduce

In the last line above, we use the lower bound introduced in [A5].

Setting and

, the following holds on the set :

We have the following result:

Lemma 6.3

Under assumptions [A1]-[A3] and [A5], if , we have, for

with .

The Lipschitz condition on and Lemma 6.2 imply that

Consequently, there exists a constant such that

Thus

By gathering all bounds, we find

Next we need to bound . This is obtained in the following Lemma:

Lemma 6.4

Under the Assumptions of Proposition 3.2 and if , there exists a constant such that

We can use Lemma 6.1 in Comte et al. (2005) to obtain that, if , then

This enables to check that using the same lines as the analogous proof given p.532 in Comte et al. (2007). For this reason, details are omitted.

6.5 Proof of Lemma 6.3.

Case . Next, let us define We can use martingale properties to see that, ,

because the last conditional expectation is zero. Moreover, the same tool shows that the covariance term for is also null by inserting a conditional expectation given . Consequently, it is now easy to see that

Now, Lemma 6.2 implies that . Then, applying also Lemma 6.1 , it follows that, with

Case . Next, for the martingale terms, we write

Both terms are bounded separately. For the first one, we use that, for

if , by inserting a conditional expectation with respect to . Now, for ,

by using Lemma 6.1.

For the second part, let us define the filtration generated by and the whole path of , i.e.

Now we observe that

as . Moreover for any ,

by inserting a conditional expectation with respect to . The last remark is that one can easilty see that

Now we have

The second part of this term can be treated in the same way, and it follows that if , then this term is less than .

6.6 Proof of Lemma 6.4.

Let us recall that we know from Comte et al. (2006) that

is such that

Here, we write that with

We shall use the following decompositions obtained by the Taylor formula:

with and if is bounded, and , because . Now, the three terms can be studied as follows. First

and we bound each term successively. Clearly by Schwarz inequality applied to each term, we find,

using that ,

and

Therefore, if , .

Next, we write that

We obtain easily that

a term which is negligible with respect to the previous ones.

Then is a martingale increment with respect to the filtration , for any measurable function . In particular,

since . In the same way, for ,

by inserting a conditional expectation with respect to . Therefore

For the last term, we write where

Moreover, we know from Comte et al. (2006) that . Now, for , we proceed as for since both have the same martingale property w.r.t. . We get

as . Using and implies . On the other hand, , as .

By gathering and comparing all terms and assuming that , we obtain the bound given in Lemma 6.4.

6.7 Proof of Theorem 4.1

The proof of this theorem relies on the following Bernstein-type Inequality:

Lemma 6.5

Under the assumptions of Theorem 4.1, for any positive numbers and , we have

Proof of Lemma 6.5: Noting that is a Brownian motion with respect to the augmented filtration , the proof is obtained as the analogous proof in Comte et al. (2007), Lemma 2 p.533.

Now we turn to the proof of Theorem 4.1.

As in the proof of Proposition 3.1, we have to split

. For the study on

, the end of the proof of Proposition 3.1 can

be used.

Now, we focus on what happens on . From the definition of , we have, , . We proceed as in the proof of Proposition 3.1 with some additional penalty terms and obtain

The difficulty here is to control the supremum of on a random ball (which depends on the random ). This is done by setting , with

We use the martingale property of and a rough bound for as follows.

For , we simply write, as previously

For , let us denote by

the quantity to be studied. Introducing a function , we first write

Then pen is chosen such that . More precisely, the next Proposition determines the choice of which in turn will fix the penalty.

Proposition 6.1

Under the assumptions of Theorem 4.1, there exists a numerical constant such that, for , we have

6.8 Proof of Theorem 4.2

The lines of the proof are the same as the ones of Theorem 4.1. Moreover, they follow closely the analogous proof of Theorem 2 p.524 in Comte et al. (2007), see also Comte et al. (2006). Therefore, we omit it.

References

- (1) Aït-Sahalia, Y. and Kimmel,R.: Maximum likelihood estimation of stochastic volatility models. J. Finance Econ. 83, 413-452 (2007).

- (2) Andersen, T., Lund, J.: Estimating continuous-time stochastic volatility models of the short-term interest rate. J. Econom. 77, 343-377 (1997).

- (3) Barndorff-Nielsen, O. E., Shephard, N.: Econometric analysis of realized volatility and its use in estimating stochastic volatility models. J. R. Stat. Soc. Ser. B Stat. Methodol. 64, 253–280 (2002).

- (4) Barron, A.R., Birgé, L., Massart, P.: Risk bounds for model selection via penalization. Probab. Theory Related Fields 113, 301–413 (1999).

- (5) Comte, F., Genon-Catalot, V. Penalized projection estimator for volatility density. Scand. J. Statist. 33, 875-893 (2006).

- (6) Comte, F., Genon-Catalot, V., Rozenholc, Y.: Penalized nonparametric mean square estimation of the coefficients of diffusion processes. Bernoulli 13, 514-543 (2007).

- (7) Comte, F., Genon-Catalot, V., Rozenholc, Y.: Nonparametric estimation for a discretely observed integrated diffusion model. Preprint MAP5, 2006-11 (2006).

- (8) Comte, F., Rozenholc, Y.: A new algorithm for fixed design regression and denoising. Ann. Inst. Statist. Math. 56, 449-473 (2004).

- (9) Cox, J. C., Ingersoll, J. E., Jr., Ross, S. A.: A theory of the term structure of interest rates. Econometrica 53, 385-407 (1985).

- (10) Genon-Catalot, V., Jeantheau, T., Larédo, C.: Parameter estimation for discretely observed stochastic volatility models . Bernoulli 5, 855-872 (1999).

- (11) Genon-Catalot, V., Jeantheau, T., Larédo, C.: Stochastic volatility models as hidden Markov models and statistical applications. Bernoulli, 6, 1051-1079 (2000).

- (12) Ghysels, E., Harvey, A., Renault, E.: Stochastic volatility. In: Maddala, G. (Ed.) Handbook of Statistics, vol. 14, North-Holland, Amsterdam, 119-191 (1996).

- (13) Gloter, A.: Estimation of the volatility diffusion coefficient for a stochastic volatility model. (French) C. R. Acad. Sci. Paris, S r. I Math. 330, 3, 243-248 (2000).

- (14) Gloter, A.: Efficient estimation of drift parameters in stochastic volatility models. Finance Stoch., 11, 495-519 (2007).

- (15) Heston, S.: A closed-form solution for options with stochastic volatility with applications to bond and currency options. Rev. Financial Stud. 6, 327-343 (1993).

- (16) Hoffmann, M.: Adaptive estimation in diffusion processes. Stochastic Process. Appl. 79, 135-163 (1999).

- (17) Hoffmann, M.: Rate of convergence for parametric estimation in a stochastic volatility model. Stochastic Process. Appl. 97, 147-170 2002.

- (18) Hull, J., White, A.: The pricing of options on assets with stochastic volatility. J. of Finance 42, 281-300 (1987).

- (19) Renò, R.: Nonparametric estimation of stochastic volatility models. Economic Letters 90, 390-395 (2006).

- (20) Rogers, L.C.G., Williams, D.: Diffusions, Markov processes, and martingales. Vol. 2, Reprint of the second (1994) edition, Cambridge Univ. Press, Cambridge (2000).

- (21) Shephard, N.: Stochastic volatility. Selected readings. (Advanced texts in Econometrics). Oxford University Press, London (2005).