Non-Regular Likelihood Inference for Seasonally Persistent Processes

Abstract

The estimation of parameters in the frequency spectrum of a seasonally persistent stationary stochastic process is addressed. For seasonal persistence associated with a pole in the spectrum located away from frequency zero, a new Whittle-type likelihood is developed that explicitly acknowledges the location of the pole. This Whittle likelihood is a large sample approximation to the distribution of the periodogram over a chosen grid of frequencies, and constitutes an approximation to the time-domain likelihood of the data, via the linear transformation of an inverse discrete Fourier transform combined with a demodulation. The new likelihood is straightforward to compute, and as will be demonstrated has good, yet non-standard, properties. The asymptotic behaviour of the proposed likelihood estimators is studied; in particular, -consistency of the estimator of the spectral pole location is established. Large finite sample and asymptotic distributions of the score and observed Fisher information are given, and the corresponding distributions of the maximum likelihood estimators are deduced. Asymptotically, the estimator of the pole after suitable standardization follows a Cauchy distribution, and for moderate sample sizes, we can use the finite large sample approximation to the distribution of the estimator of the pole corresponding to the ratio of two Gaussian random variables, with sample size dependent means and variances. A study of the small sample properties of the likelihood approximation is provided, and its superior performance to previously suggested methods is shown, as well as agreement with the developed distributional approximations. Inspired by the developments for full likelihood based estimation procedures, usage of profile likelihood and other likelihood based procedures are also discussed. Semi-parametric estimation methods, such as the Geweke-Porter-Hudak estimator of the long memory parameter, inspired by the developed parametric theory are introduced.

KEYWORDS: Periodogram; Seasonal persistence; likelihood inference, Whittle likelihood.

1 Introduction

In this paper, we develop likelihood estimation of the parameters of a stationary stochastic process that exhibits seasonal persistence, that is, long memory behaviour associated with a stationary, quasi-seasonal dependence structure. We introduce a new frequency-domain likelihood approximation which is computed using demodulation and which, for the first time, facilitates maximum likelihood estimation. We consider joint estimation of the seasonality and persistence parameters, and establish the asymptotic and large sample properties of the likelihood and its associated maximum likelihood estimators. This is in direct contrast with previously suggested procedures, where the distribution of the estimator of the seasonality parameter could not be established (Giraitis et al., 2001). The estimators are demonstrated to have good small sample properties compared with estimators based on the classic Whittle likelihood, and other non-likelihood derived estimators. Our non-standard asymptotic results rely on the appropriate renormalization of the score and Fisher information, and utilize a parameter-dependent linear transformation of the data. This transformation enables an efficient approximation to the likelihood. The transformation also introduces a number of interesting and non-regular features into the likelihood surface: jumps, local oscillations, and non-regular large sample theory. Despite these issues the large sample theory can be determined, and appropriate finite large sample approximations provided, as will be demonstrated. It transpires that the small sample properties of the estimators are competitive with existing methods, as well be discussed in later sections.

The contributions of this paper thus include new theory for non-regular maximum likelihood problems. In similarly motivated work, Cheng and Taylor (1995) discussed problems associated with maximum likelihood estimation for unbounded likelihoods: in contrast we discuss problems associated with distributions of non-identically distributed, weakly dependent variables with highly compressed and for increasing sample sizes unbounded variances. Given the importance of compressed linear decompositions in modern statistical theory, our work has implications for the distribution of sparseness-inducing transformations much beyond the analysis of seasonal processes and Fourier theory, and forms a contribution to developing methodology for inference of stochastically compressible processes.

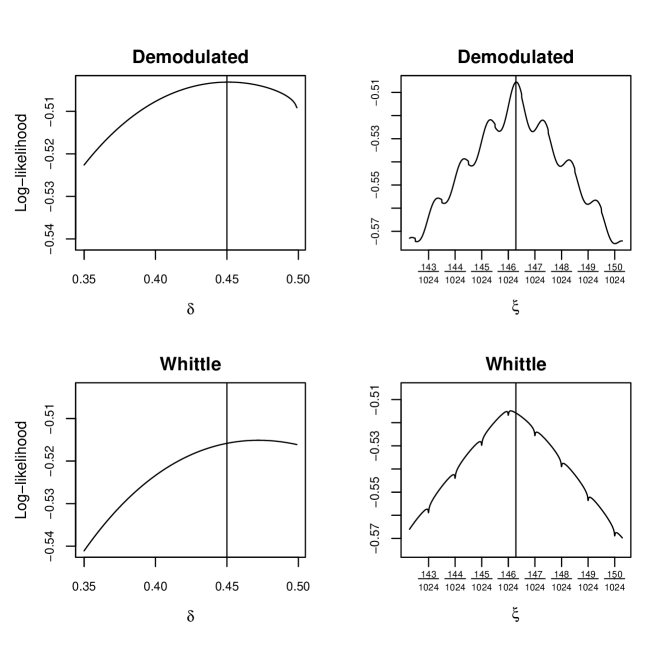

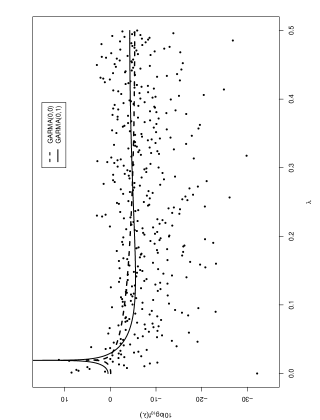

One of the concrete and substantive conclusions of our new estimation procedures is illustrated in Figure 1; this figure illustrates that whereas a standard estimation procedure, based on the Whittle likelihood (see Section 1.3), produces estimates that are, on average, biased even in large samples, our new procedure, based on a carefully constructed likelihood (see Sections 2.2 and 3), produces estimators that exhibit no such bias. Full details of this Figure are given in Section 4.1.

1.1 Seasonally Persistent Processes

Stationary time-series models with long range dependence describe a wide range of physical phenomena; see for general discussion Andel (1986) and Gray et al. (1989), and also applications in econometrics (Porter-Hudak, 1990; Gil-Alana, 2002), biology (Beran, 1994) and hydrology (Ooms, 2001). Dependence in a stationary time series is parameterized via the autocovariance sequence, . We are concerned with the estimation of parameters that specify under an assumption of seasonal persistence. Specifically, of particular importance is the seasonality of the data characterized by a frequency, , termed the pole, and an associated degree of dependence, characterized by a persistence (or long memory) parameter . Whereas inference for the persistence parameter in the context of poles at frequency zero has been much studied (Beran, 1994), the theoretical behaviour of estimators of the persistence parameter remains largely uninvestigated when the underlying seasonality of the process is unknown.

Let be a zero-mean, second-order stationary time series with autocovariance (acv) sequence , and spectral density function (sdf), ,

| (1) |

The process exhibits seasonal or periodic persistence if there exist real numbers and , and a bounded function such that

or equivalently if there exist and and a bounded function such that

Following convention, we parameterize the persistence parameter via . In line with this definition, a process is considered to be a seasonally persistent process (SPP) if, in a neighbourhood of ,

| (2) |

where , is bounded above.

Parameters determine the dominant long term behaviour of the process; typically, corresponds to the location of an unbounded but integrable singularity in the sdf. In this paper we consider a parametric family of sdfs consistent with (2), that is, the parametric model of Giraitis et al. (2001), where

| (3) |

where is bounded above and below at , with some linear process assumptions, given for instance in Hannan (1973); for example, could be the sdf for a stationary and invertible ARMA process, such is the case for GARMA processes, see Gray et al. (1989). We consider behaviour near the pole in such models by defining , where

| (4) |

The results in this paper will also be applicable to nearly non-stationary unit root AR processes, when the roots of the AR process approach unity at a suitable rate in the sample size, this quantifying issues with near unit root processes.

1.2 Estimation for Seasonally Persistent Processes

We consider maximum likelihood estimation of and , and denote the true values of these parameters by . Joint estimation of the seasonality and persistence parameters is of importance, as inaccurate estimation of will affect the estimation of , and any other parameters of the sdf – quantifies the rate of decay of the dependence, and thus determines the long-term behaviour of the series. Note also that, even in cases where is believed to be known (for calendar data, equal to 1/12, or 1/7, or 1/4 say), there may on occasion be finite sample advantage in estimating rather than using its known value, in terms of estimation of the other parameters of the system. For example, if is regarded as a nuisance parameter, then may be more efficiently estimated after conditioning on rather than ; see, for example, Robins et al. (1994) and Rathouz et al. (2002) for supporting theory. This issue goes beyond the scope of this paper, but gives further indication that estimation of is intrinsically important.

We will examine inference for the parameters of an SPP based on a realization of the process of length . Throughout this paper, for convenience and with minimal loss of generality, we will assume is even, say. We establish asymptotic results for these estimators , and provide practically useful large sample approximations to the distribution of the estimators. In particular, we define a large sample approximation to the log-likelihood of the periodogram evaluated at a full set of frequencies spaced apart. At a local scale the variational structure of the log-likelihood in remains appreciable over distances; however the magnitude of these variations becomes negligible compared to the total accumulated magnitude of the log-likelihood for increasing sample sizes. We demonstrate that this variation prevents standard likelihood results being valid for the estimator of , although standard asymptotic results can be established for the estimator of the , which is in agreement with previous results, see (Hidalgo and Soulier, 2004; Giraitis et al., 2001). We discuss in detail the large sample behaviour of and establish its approximate large sample distribution, as well as a moderate sample size approximation. Finally we demonstrate that our likelihood-based estimators have good small sample properties on simulated series compared with other, non-likelihood estimators, and consider estimation of the system parameters in a econometric example, using a data set with weekly gasoline sales in the United States, and two meteorological examples, monthly temperature data from a Californian shore-station, and the Southern Oscillation Index data set.

1.3 The Periodogram, Likelihoods and Approximations

We consider a sample from a stationary Gaussian time series, , as defined in section 1.1, with covariance matrix with element . The exact log likelihood, , of the finite time-domain sample is given by

| (5) |

This likelihood is often approximated due to the computational complexity associated with the calculation of . The standard approximation approach was introduced by Whittle (1951), and the resulting, much studied, discretized approximate likelihood is commonly known as the discrete Whittle likelihood. The Whittle likelihood gives an approximation to the likelihood of the time domain data in the frequency domain via the Fourier coefficients, under assumptions as specified by Beran (1994, p. 109–113, and 116–7). Problems associated with the usage of Whittle’s approximation for non-Gaussian and small sample size Gaussian time series has been discussed by Contreras-Cristan et al. (2006).

The final two terms in equation (5) are approximated using results of Whittle (1951) and Grenander and Szegö (1984). It follows that the Whittle likelihood for and is given by:

| (6) |

where is the periodogram, defined as the modulus square of the discrete Fourier transform (DFT), , of the realized time series.

At the Fourier frequencies , , the periodogram, , is given by, where

| (7) |

so that

For short memory data, the periodogram is an asymptotically unbiased but inconsistent estimator of that is commonly used as the basis of more sophisticated estimation procedures. The use of (6) for parameter estimation has been discussed in detail by Walker (1964, 1965) and Hannan (1973) under the assumption that the log spectrum integrates to zero. Hosoya (1974) added a second term of to the integral to deal with more general processes.

For the likelihood in equation (6) to have desirable asymptotic properties, it is assumed that the process is linear, and satisfies certain regularity conditions, thus ensuring good large sample properties of the likelihood based estimators. Note that (6) is an approximation to the log-likelihood of based on the periodogram, but that (6) is not a likelihood for the periodogram. The approximation of the likelihood in equation (5) by equation (6), performs well when the process is Gaussian and the covariance of the time series is either rapidly decaying or exactly periodic.

A Riemann approximation to the integral in equation (6) yields the discrete analogue

| (8) |

and we could also adjust this to allow for more general processes:

| (9) |

following Hosoya’s proposal. By defining the vector where and , and as the exact covariance of , we may consider the exact log-likelihood, of the DFT of observed and Gaussian data via:

| (10) |

in direct analogue with equation (5), acknowledging finite sample effects of the DFT. The difference between this equation and the discrete Whittle likelihood is that it involves the exact covariance matrix, , of the FFT coefficients. Analysis based on the likelihood of the Fourier coefficients (in general) involves the inversion of the large, non-sparse covariance matrix, and is thus equally inefficient as the basis of likelihood procedures as equation (5).

Having specified these various likelihood functions that could be used for inference, some justification must be used to motivate their usage. Equation (10) is a natural choice for analysis of seasonal time series, given the compression of the variables of the seasonal effects. We shall use the compression to approximate the likelihood more carefully, acknowledging large finite sample effects related to the compression explicitly.

1.4 Contributions of the Paper

We introduce an approximation to equation (10), and use this as the basis of a maximum likelihood procedure. We focus on the distribution and other properties of the periodogram, given an underlying SPP with sdf . We focus on Gaussian processes, and do not consider here the non-Gaussian case. However, for other processes, such as those in Brillinger (1975), where asymptotic normality of the DFT holds, our distributional results are still valid.

Specifically, we consider estimation of parameters of spectra with spectral poles away from frequency zero. We consider an adjustment to the standard DFT that simplifies the technical developments of this paper. A simple (but parameter dependent) modification of the choice of grid, conditional on a known spectral pole location, leads to simple approximations to the likelihood of the periodogram at a new set of frequencies spaced at a distance apart. In particular

-

1.

We propose a new demodulated Whittle discrete likelihood for seasonal processes (sections 2 & 3). We show that the proposed likelihood approximates the distribution of the discrete Fourier transform for any posited value of the true parameters (see Theorem 1). The key idea is to use a different orthogonal transformation of the data conditional on each fixed value of the location of the pole (specification of a compressed representation). This is a non-standard situation.

-

2.

To establish the properties of the likelihood we calculate the large finite sample distribution of the periodogram at the pole itself (Section 2.3).

-

3.

We bound the covariance of the demodulated periodogram at different frequencies spaced apart (noted in Section 3), and note its asymptotically negligible contribution to the normalized log-likelihood. Furthermore, the choice of approximation to the likelihood is not everywhere continuous. However, we demonstrate (Section 3) that the discontinuities in the likelihood surface represent a negligible contribution for finite large samples.

-

4.

We prove consistency of the MLEs (see Theorem 2), and determine the large sample first order properties of the score and observed Fisher information (Theorem 3).

-

5.

We determine the asymptotic distribution of the score and observed Fisher information (see Theorem 4) and the asymptotic distribution of the MLEs (see Theorem 5).

-

6.

We give a large finite sample approximation to the distribution of the pole estimator (see Proposition 6).

To derive the appropriate large sample theory, some care is required. It transpires that the score and Fisher information do not exhibit the usual large sample behaviour. Our results are based on a Taylor expansion of the log-likelihood; we adopt the normalization of the observed Fisher information adopted by Sweeting (1980, 1992). We thus renormalize the observed Fisher information appropriately with a suitable power of . The renormalized score and observed Fisher information converge in law to Gaussian random variables that are asymptotically uncorrelated. The distribution of converges slowly to the asymptotic distribution, and so alternate finite large sample approximations are also given.

These results establish a new large sample theory for seasonally persistent processes, and utilize the data-dependent transformation of the time-domain data that facilitate the computation of the distribution of different random variables for each posited value of the pole, and appropriate normalisation techniques for the score and Fisher information when the data is modelled as highly compressed in the Fourier domain.

1.5 Connections with Recent Work

In connections with other related work, we distinguish between likelihood-based methods and semi-parametric methods for processes exhibiting seasonal persistence. Giraitis et al. (2001) consider fully parametric models, and constrain the maximization over the location to a grid of frequencies spaced apart. Hidalgo and Soulier (2004) consider semi-parametric models, and the theoretical properties of the extended Geweke-Porter-Hudak estimator, basing their analysis on estimating the location of the singularity as the Fourier coefficient of the maximum periodogram value in a given frequency interval; in their simulation study, the true location of the singularity is aligned with the Fourier frequency grid. Hidalgo and Soulier (2004) evaluate the Fourier coefficients at the Fourier frequency grid, and restrict the estimate of the location of the pole to a grid of frequencies spaced apart. Hidalgo (2005) used semi-parametric methods to estimate the location of the pole, as well as the long memory parameter. By using a two-step procedure he is able to develop large sample theory for the estimator of the singularity, whereas in contrast we focus on full likelihood methods. More recently, Whitcher (2004) used a wavelet packet analysis approach for estimation of seasonally persistent processes.

In terms of asymptotic properties, our rate of convergence matches that of Giraitis et al. (2001). However, in addition, we obtain the large sample distributional results for the estimator of the pole, which they fail to do, having produced a different estimator. Similarly to Giraitis’ et al., Beran and Gosh (2000) estimate the location of the pole using the coefficient which maximises the periodogram. Our estimator is again different although asymptotically equivalent with the same rate of convergence, and it has a determinable asymptotic, as well as large finite sample approximate, distribution.

Our work also has a connection with, but is different in spirit from, hidden frequency estimation, in which the seasonal structure is modelled as deterministic, corresponding to a single sinusoid. In this case, the Fourier coefficient which maximizes the periodogram converges to the true coefficient with a faster rate than the convergence of the MLE of the pole. Such rates were improved by secondary analysis, and the corresponding analysis using data tapers, see for example Chen et al. (2000); Hannan (1973, 1986); v. Sachs (1993). Secondary analysis corresponds to partitioning the time series into several groups of data, and using regression to estimate the so-called hidden frequency. Thomson (1990) used multitaper methods to improve the detection of a set of hidden frequencies, and use least squares methods over a given bandwidth. Neither the model we use, nor our proposed inferential method, is equivalent to the above mentioned procedures. Secondary analysis can be considered to ‘zoom in’ on local structure near the pole, and may be philosophically related to our procedure, but we implement full likelihood for a full set of Fourier coefficients. Conditionally for each fixed value for the pole, we calculate the distribution of a different set of random variables, but as each set is a linear and orthogonal transformation of the original data, and with a constant and equal Jacobian, this is appropriate.

Finally, we note that the inferential issues are of importance beyond seasonally persistent processes. The inherent non-regularity arises due to a parameter dependent transformation of the time-domain data. Whenever the process is modelled using a suitable parametric linear transformation of the data that will give decomposition coefficients that are non-negligible only for a few sets of indices, our methods will be applicable with some minor modifications. In a more general setting we would write the variances of a set of basis coefficients as satisfying a power-law decay, and we refer to such processes as second order compressive processes. Power-law decay in a suitable basis is an relatively common phenomenon - see for example the discussion in Donoho (2006); Abramovich et al. (2006); Candès and Tao (2004) - and our developments will carry across to this setting if the compression is stochastic rather than deterministic, once the location and decay parameters have been incorporated in the arbitrary basis. Issues of alignment, and/or shift-variance, akin to results that arise for misspecified location of the pole, are very well-documented in other basis expansions (Coifman and Donoho, 1995). Note that the equivalent to the decay parameter discussed by the aforementioned authors will be . Only for are we in their mode of decay, corresponding to extreme regimes of long memory behaviour.

2 Distributional results for the Periodogram

2.1 Large Sample Properties

The large sample properties of the periodogram of seasonally persistent processes were determined in Olhede et al. (2004). We summarize and extend these results below; in particular we compute the statistical properties of the periodogram itself at the pole , as this specific Fourier coefficient will contribute substantively to the subsequent likelihood calculation.

Theorem 1 in Olhede et al. (2004) gives the following result concerning the relative bias at frequency , , of the periodogram for all ,

This notation makes explicit the dependence of the relative bias on and . For frequencies , we have, for large and a fixed value of , with ,

| (11) |

where denotes times the distance between the Fourier frequency and the pole at . For the case , the large sample value of is given in Lemma 1 in Section 2.4.

For the second order moment properties, let

Then, for from (7), Olhede et al. (2004) gives

These results specify the large sample first and second order structure of the periodogram. We now extend these results to the demodulated periodogram described in section 2.2. Note that a direct implication of these results is that the distribution of the periodogram is highly dependent on the distances between the pole and the Fourier frequencies .

2.2 The Demodulated Discrete Fourier Transformation

The Discrete Fourier Transform of is not constrained to be evaluated at , but in fact any grid could be considered. This fact leads us to consider demodulation, a grid realignment technique, which for any fixed value of produces a new grid aligned with the pole. Demodulation ensures that the large sample behaviour of the demodulated periodogram is similar to that of the periodogram of a standard long memory process (where ). Specifically, the large sample bias is the same but the distribution of the periodogram is rather than a sum of unequally weighted random variables (see Hurvich and Beltrao, 1993; Olhede et al., 2004, p. 621).

The Demodulated Discrete Fourier Transform (DDFT) or offset DFT (Pei and Ding, 2004) of a sample of size from time series with demodulation via a fixed frequency is denoted , and is defined for Fourier frequency by

| (12) |

The demodulated periodogram at frequency with demodulation via is denoted , and is defined via the ordinary periodogram by

Hence is simply the periodogram evaluated at frequency or We will consider evaluating this expression at arbitrary frequency . We define in analogue to in equation (10). For Gaussian data we then find:

| (13) |

Note that due to the demodulation, in general, unlike the imaginary component of the DFT at frequency zero. To efficiently formulate the likelihood, we need to explicitly consider the computation of , the covariance of the DDFT coefficients.

2.3 Extending the Olhede et al. (2004) result

The results in Olhede et al. (2004) do not cover the case of demodulation, and to enable calculation of the new likelihood, further results are required. For example needs to be explicitly determined. To minimize the bias in the demodulated periodogram, and simplify the covariance structure, we shift the Fourier grid so that the closest Fourier frequency to the pole in the original grid coincides exactly with the pole in the demodulated version. For a pole at , we denote by where indicates the nearest integer to We furthermore let and specify in (12) as . The approach introduces a new grid of frequencies, namely

| (14) |

We exclude Fourier frequencies and , and taking we have . For example, if and , then , , and . Note that for , then

so that the covariance properties of the DDFT can be easily determined.

Under this demodulation, the DDFT yields the original periodogram evaluated at frequencies and takes the form

| (15) |

so that, for , The DDFT can be computed efficiently by applying the DFT to the new series defined for by . Demodulation both simplifies the mathematical calculations considerably, and improves estimation of the persistence parameter Naturally the operation is very straightforward to implement. The parameter dependent choice of will need careful analysis when deriving properties of the parameter estimators.

2.4 Expectation of the Periodogram at the Pole

The result in (11) gives the relative bias of periodogram. The expectation of the periodogram is given in the following Lemma.

Lemma 1

The expected value of the periodogram evaluated at the pole , after demodulation by , is

Proof: See Appendix A.1.

3 Asymptotic Properties of the Likelihood and Estimators

In this section we utilize demodulation, and the large sample approximations described above, to present three theorems that characterize the asymptotic behaviour of the likelihood, the corresponding MLEs for and the associated Fisher information to obtain their large sample properties. Specifically, we establish -consistency for the estimator of the location of the pole, thus matching the result of Giraitis et al. (2001).

3.1 Large-sample Likelihood Approximation

For a periodogram demodulated to align the Fourier grid with pole , we have the following asymptotic result.

Theorem 2

Approximating the Likelihood Function.

For a Gaussian series from a periodic long memory model as described by

(3), where is twice partially differentiable

with respect to , the log-likelihood of the discrete Fourier

transform can be approximated by

| (16) |

accurate to , where

| (17) |

for , where is the indicator function for event ,

and is the asymptotic relative bias given by Lemma 1.

Proof: See the Appendices A.2-A.4.

Note I :

The approximation to the likelihood is equivalent to that of independent exponential random variables with rate parameters that depend on and but not on . In equation (17), the function appropriately scales the periodogram contribution from the Fourier frequency aligned with . is monotonically increasing in , with , and is bounded away from zero. As the function is monotonic the derivatives of are also bounded away from zero. If is also bounded away from zero, then the log likelihood is bounded in and . Thus it is possible to find efficiently the MLEs of and numerically.

Note II :

This likelihood is not differentiable with respect to at all values of ; although is available in simple form, the dependence of and on renders the overall function discontinuous. However, the discontinuities are in magnitude, and the log likelihood is uniformly at least , so in fact the discontinuities are negligible, but motivate us to look, in standard fashion, at the -standardized likelihood function . See Appendix A.4 for further details.

Note III :

The formulation in Theorem 2 summarizes the data in the frequency domain via the demodulated periodogram for a given . We avoid the introduction of the substantial bias and covariance terms found in Olhede et al. (2004), as the demodulated periodogram is perfectly aligned with this singularity. When other demodulations are chosen the likelihood cannot be approximated in such a fashion. Even for frequencies of sufficient distance from any irregular behaviour, the results of Olhede et al. (2004) cannot be applied directly, and to find the approximate Whittle likelihood we additionally need to make assumptions about the spectral density function, and its smoothness (see Dzhamparidze and Yaglom (1983) and Taniguchi and Kakizawa (2000)).

Note IV :

The result differs with that of Hurvich and Beltrao (1993) in a number of ways. The ordinates subscripted and in the DFT are no longer complex conjugates, and the likelihood at evaluated at is now approximately (rather than a mixture of two different terms) even for those coefficients closest to the pole. Strictly, the definition for in equation (17) has an additional term for , but these terms can be bounded appropriately, and thus contribute in a negligible fashion. The bias at the pole reported in Hurvich and Beltrao (1993) is (identically) present in our formulation, but is , and is thus subsumed into the final term – see Hurvich et al. (1998) for relevant supporting arguments.

3.2 Existence and Consistency of the ML estimators

We now use the results of the previous section to construct likelihood-based estimators of and and establish their properties. The following theorem establishes the existence and consistency of the ML estimators derived from the likelihood in Theorem 2.

Theorem 3

Existence and Consistency

For the

likelihood of Theorem 2, the ML estimators of and

, and , exist and are consistent, with

convergence rates and respectively.

Proof: See Appendix A.5.

The -consistency of matches the convergence rate of Giraitis et al. (2001). It is unusual to find superconsistent estimators in likelihood based procedures. An intuitive understanding of the rate can be found in the time domain. As we collect full periods of the data the periodicity of the data is determined to an accuracy of . The reason why this rate is achieved is that the log-likelihood is varying (see proposition 14) over distances in of near the value However, the convergence rate is different to that of Chen et al. (2000). The latter model the seasonality as a deterministic seasonal component embedded in stationary noise. In Chen et al. a regression model is employed to estimate the amplitude and locations of the seasonality, and a rate of rather than is achieved. We employ a different model and hence do not expect the same convergence rates as is achieved by Chen et al..

3.3 Properties of The Fisher Information Matrix

Theorem 4

The Fisher Information.

For a series from a periodic long memory model as described by

(3), for large , the components of the Fisher information

are given by

where , and are constants independent of but are functions of the true values of and .

For a full analysis in a regular ML setting, the second order properties of the MLEs can in a general setting be deduced from the above quantities. Large sample properties, specifically consistency and asymptotic variance, may be considered via a Taylor expansion of the log-likelihood, see for example Cheng and Taylor (1995). However, we note that we are not in a standard setting; even if we may expand the log-likelihood near the true value of the parameter, because of the non-standard behaviour of the derivatives of the log-likelihood, the observed Fisher information does not converge to a diagonal matrix with constant entries, but rather the (appropriately standardized) observed Fisher information for converges to a random variable with order one variance. We will discuss the interpretation of the Fisher information in this context, in the appendix. For the derivatives involving the location of the pole, extra terms of magnitude are introduced and thus the variance of the observed Fisher information in is The magnitude of the variance of the observed Fisher information in implies that a standardization of the random variable must be employed that results in a negligible expectation of the restandardized random variable. We also therefore discuss the large sample theory of the observed Fisher information.

3.4 The Asymptotic Properties of the MLEs

We now consider the use of the Fisher information to determine the asymptotic variance. Consider a Taylor expansion of the score near the true value of the parameters evaluated at the MLE . We denote the observed Fisher information by , and let lie between and . We denote by the score in , noting that the score is well defined if the log-likelihood is evaluated ignoring the dependence of and , see section A-4:

| (18) |

Then using a first-order expansion of the log likelihood in the usual way for sufficiently large, we have the (vector) score function:

Thus the difference between and , when appropriately scaled by the random matrix corresponds to the value of the score at in the usual fashion. The statistical properties of are not straightforward in this non-regular problem, and require further investigation. Following Sweeting (1992), we define a suitable standardization matrix and the standardized observed Fisher information by

| (19) |

as the large sample properties of are tractable, and their determination is an important step to finding the large sample properties of the MLE. Specifically, we let

so that

The latter expression defines the standardized score See the Appendix for a full discussion of these quantities. Note that is the large approximation to the Fisher information matrix for and corresponds to an appropriate order normalisation for thus is the observed Fisher information renormalized by .

We note that for large enough, the expected value of is the identity matrix for the entry, but the expectation of the first entry of is whilst the variance of the first entry is In a standard setting the expectation is and the variance .

Theorem 5

Distribution of the Score and Observed Fisher Information.

For the likelihood of Theorem 2 the standardized score

and the standardized Observed Fisher information matrix

asymptotically have the following properties:

| (20) |

where the entries of and are uncorrelated and

| (21) |

Proof: An outline of the proof given in the Appendix, see Proposition 12, Section A.8.3 and Proposition 15.

Theorem 6

Distribution of the MLE.

For the likelihood of Theorem 2, the ML estimators of

and , and have distributions that for large

sample approximately take the form:

where is distributed according to the standard Cauchy distribution, and

| (22) |

An estimator of the asymptotic variance is formed via . The forms of and are given in the Appendix.

Note :

Giraitis et al. (2001) do not find the limiting distribution of their estimator, , of . They note that this is an artefact of the maximization over the specified grid. This constraint is not enforced in our approach. Note that but that is not constrained to be zero or even to have a tractable distribution, this result is demonstrated empirically in the simulations. The convergence to the Cauchy for extreme values of is quite slow, we provide, in the Appendix, a second approximation to the distribution of the renormalized estimator of the pole, via more carefully approximating the dominant contributions to the mean and variance of the numerator and denominator that define the random variable the estimator follows.

To compare the two large sample and asymptotic forms of the distributions, we refer to Figure 2 (a) and (b). As increases in magnitude it takes longer for the large sample approximation to be close the asymptotic distribution, as is obvious from these plots. For a list of critical values of the distribution see Table 10.

The likelihood of the data changes in magnitude dramatically depending on the value of and its alignment with the grid of frequencies at which the periodogram is evaluated, determination of the best value of is pivotal for characterizing the system, and must be the first stage of any analysis. For completeness we now discuss the estimation of the additional parameters, i.e. and .

3.5 White Noise Variance and Nuisance Parameters

We now consider the estimation of the white noise component and regular spectral component. We model the sdf parametrically by

| (23) |

Differentiating from equation (16) with respect to we obtain that:

| (24) |

Thus it follows that (Taylor expanding the other MLEs and using their rates of convergence):

| (25) |

for sufficiently large. This follows as the estimators of the other parameters of the sdf are nearly unbiased for sufficiently large values of . We note that the covariance of with and can be treated analogously to the results deriving the covariance of and or using standard results for and/or and . Denoting by

we determine that

and

which is Thus we find that

| (26) |

This then provides the required score equations. Furthermore using regular ML theory, we have that:

| (27) |

where contains the Fisher information, and . This allows us to fit the more general class of GARMA rather than Gegenbauer models, see Gray et al. (1989).

4 Examples

4.1 Analysis of Simulated Data

For our simulation studies we examine the performance of our adjusted Whittle likelihood-based estimators in comparison with those derived from the classic Whittle likelihood. Data were simulated in the time domain using the covariance recursion formulae given in Lapsa (1997) for a seasonally persistent Gegenbauer process with corresponding to an weekly cycle in daily data, and and . We generate 2000 replicate series of lengths and 8192. Tables 1 to 4 demonstrate the performance of the ML estimators of and , in terms of bias, variance, and the relative efficiency () of our estimators compared with those derived using the classic Whittle likelihood. For the demodulated estimator significantly improves the bias present in the Whittle estimators for both and . As increases and the spacing in the Fourier grid decreases, both estimators for perform well, however, the bias in the Whittle estimator for is still present even for , and becomes more severe as increases.

To illustrate the problems with the Whittle likelihood for smaller and large , Figure 1 shows the mean conditional likelihoods evaluated at the ML estimates. The improvement gained by demodulation is evident, the scale of the improvement will be dependent on the distance of the pole from the Fourier grid. The plots also demonstrate the discontinuities in the likelihood for , as discussed in Section 3.

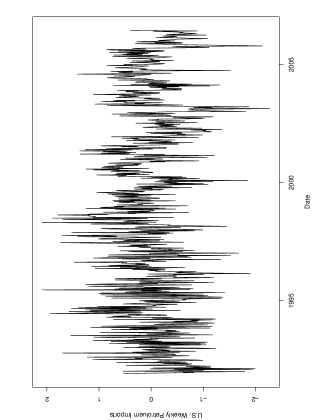

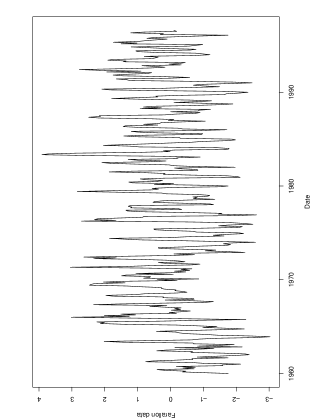

4.2 U.S. Weekly Crude Oil Imports

The first real data set comprises 756 observations of U.S. Weekly Crude Oil Imports (in millions of barrels per day) from 6th December 1991 to 26th May 2006, downloaded from

The data were detrended using a linear trend, and are displayed in Figure 3. Periodic behaviour is evident in the raw detrended data.

For these data, we fitted a low order Gegenbauer-ARMA (GARMA) model; the process is represented as the unique stationary solution of

where is the backshift operator, and polynomial operators and define an ARMA process in the usual way, and where is a pure Gegenbauer process as defined by the sdf in equation (3) with the identity function. We consider at most ARMA(1,1) models, so that and where, under the assumptions of stationarity and invertibility, . Using standard results, the parametric sdf that we consider takes the form

In our notation, a GARMA(1,1) model has both and non-zero; for GARMA(1,0), , whereas for GARMA(0,1), . GARMA(0,0) corresponds to the Gegenbauer model with no ARMA component.

Results : Using numerical methods (the optim function in R), each model was fitted using our demodulation approach and also using the standard Whittle likelihood, and the results compared using BIC. The results are presented in Table 5. The best model is the overall is the GARMA(0,1) model fitted under demodulation, indicating that the use of a non-standard Fourier grid can improve the quality of fit, that is, the fit of the model under the standard derivation (we term this the standard Whittle model) is inferior.

For the selected model, the parameter estimates and approximate standard errors are displayed in Table 6.

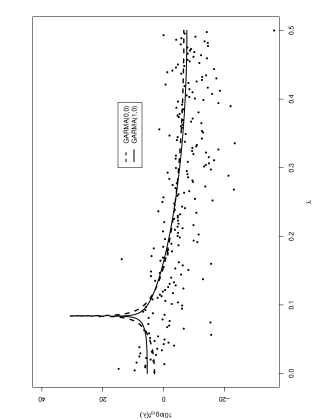

4.3 Farallon temperature data

The second real data set is a surface temperature series for the shore station at the Farallon Islands, California, United States. Daily temperature data were obtained from the ftp site

and formed monthly averages for the period 1960-1996; missing daily quantities were omitted from the monthly averages, whole missing months (there were six in the period of study) were imputed by taking averages for that calendar month across the 37 years of study. In total there were 444 monthly average observations.

We analyze these data in two ways to compare the Whittle maximum likelihood estimates with our demodulation approach. First, we take the 444 data in their entirety, then we perform a second analysis using only the last 440 observations. As the expected annual periodicity would induce a pole in the spectrum at frequency 1/12, and 12 divides 444, the pole will lie at a Fourier frequency when the whole data set is analyzed. However 12 does not divide 440, so for the second analysis, the pole will not lie at a Fourier frequency.

Results : Each of the low order GARMA models were fitted and compared using BIC. The two cases, and were analyzed. The results are presented in Table 7, and the raw time series as well as fitted models are plotted in Figure 4. The model with the highest BIC is, in both cases, the GARMA(1,0), but for the two values of , the different approaches are favoured in the two cases. For , the classic Whittle approach yields a higher log-likelihood, but for the demodulated model performs better, yielding a higher log-likelihood. Parameter estimates from the model are presented in Table 6 for the two values of .

This data set and analysis illustrates perfectly another of the advantages of using the demodulated likelihood with the bias-adjustment procedured outlined in Section 3 and Theorem 2. In the classic Whittle likelihood, when a Fourier frequency exactly coincides with the pole, the on-the-pole likelihood contribution erases the contribution of that periodogram element. Note first that the omission of a data point from the likelihood causes the likelihood to increase (that is, become less negative) and this explains the higher likelihood value for the classic Whittle likelihood. For the Farallon data set, this omission also leads the remaining periodogram appearing as if it corresponded to a short memory process, hence the low estimated value of that is essentially no different from zero. The conclusion of such an analysis would be that the underlying process has a pure seasonality at the estimated , in this case , and the seasonally differenced series was essentially a white noise process. However, seasonal first differencing of the original series leads to a new series that is not a white noise process; in fact the differenced series appears over-differenced. Hence, such a model does not provide an adequate explanation of the data. When is changed to 440, inferences using the classic Whittle method change dramatically. Note, however, that for the new demodulated likelihood, parameters estimates are closely comparable across different values of .

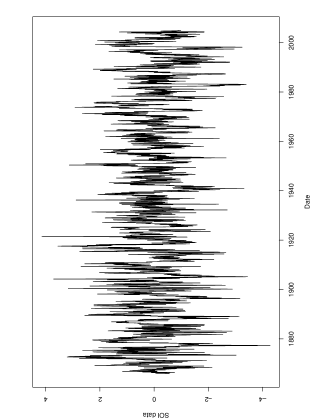

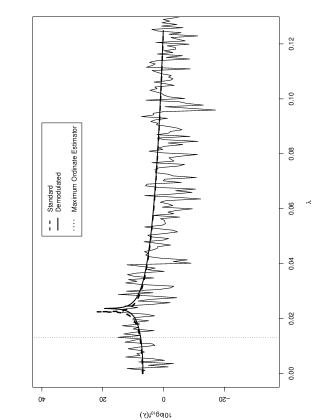

4.4 Southern Oscillation Index

We consider the Southern Oscillation Index (SOI) data analyzed by, for example, Huerta and West (1999). The version of the data we consider has , the data and fitted spectrum are presented in Figure 5. For this large sample size, the difference between the two approaches is minimal; the BIC values are negligibly different, and the estimates and estimated 95 % intervals are presented in Table 9. In this case, the estimates of the pole position obtained from the likelihood approaches are markedly different from the naive estimate obtained by taking the ordinate corresponding to the maximum of the periodogram (shown as a dotted line in Figure 5(b)).

5 Implications for Non-Likelihood Approaches

The results derived in previous sections focus explicitly on likelihood based procedures. However, they motivate the use of adjusted versions of currently existing estimation procedures that improve the performance of those procedures when applied to seasonally persistent series. Given the special role of the location of the singularity when formulating the likelihood, we propose a series of procedures that profit on the simplified distribution that arises by using the demodulation by the (estimated) pole.

5.1 Profile Likelihood

The profile likelihood of is a pseudo-likelihood function given, for each possible , by

| (28) |

may be maximized, yielding a maximum pseudo-likelihood (MPL) estimate of , denoted . Then the values of and which maximize the conditional likelihood given , are computed. Specifically, the ML estimate of based on the demodulated likelihood for all values of is computed. Finally, the estimate based on demodulation at is obtained.

In many cases the MPL and ML estimators agree closely; in given applications, the MPL approach may potentially be more readily implemented. Note that some care must in generality be used when applying profile likelihood estimation, (see, for example, Berger et al. (1999)), but given the rate of convergence of the MLE of such problems are unlikely to arise.

5.2 A Semi-Parametric Analysis: The Geweke-Porter-Hudak Estimator

The Geweke-Porter-Hudak (GPH) procedure (Geweke and Porter-Hudak, 1983) implements semiparametric estimation of for the case which can be adapted to incorporate a demodulation procedure and profile marginalization. The GPH procedure examines the behaviour of the periodogram on the log scale near frequency zero, and estimates the long memory parameter using ordinary least squares and a linear regression. We omit full details for brevity, but outline a possible adjustment based on a recent formulation given by Hidalgo and Soulier (2004). It is sufficient to say that the GPH procedure relies on distributional properties of the periodogram near the presumed pole.

In light of the results of earlier sections of this paper, to obtain an improved estimate of the using GPH we could take two alternative approaches. First, we could adjust the GPH to the demodulated setting, taking the distribution of the periodogram at the singularity fully into account. Alternatively, we could utilize large sample arguments and consider the score function. We consider frequencies indexed whose likelihood contributions are influenced by the singularity. The log-likelihood then has three parameters; , , and which can be treated as a constant, if the included are chosen judiciously.

Hidalgo and Soulier (2004, p. 58-59) consider the modified GPH by introducing the following notation:

where periodogram ordinates on either side of the pole are included in the regression. They also define (with slightly different notation) , and define the estimator to be:

| (29) |

Hidalgo and Soulier note that the asymptotic distribution of is not known, and that estimation of the pole is an open problem. In their simulation studies, 5000 replications of series length 256, 512 and 1024 are used, with , and thus there is grid alignment with the pole. They implement the GPH procedure, assuming is correct on the demodulated periodogram, excluding the contribution from the pole itself. Notice also that they chose , and , i.e .

Having found the distribution of the periodogram at the pole in Lemma 1, we can adjust the GPH estimator using a similar profile likelihood approach. Assume that is known, and consider such that

As is known we are on the grid, and . Thus we may ignore the contributions of the term, and omit this from the procedure as the terms sum to a negligible contribution. Based on these values of , least squares is then used to estimate . This requires knowledge of ; note that Hidalgo and Soulier estimate as the Fourier frequency at which the periodogram is maximized, and therefore are restricted to an grid. In contrast, for any , we demodulate the periodogram by giving

where is calculated for the specified , not necessarily on the Fourier grid; in practice it is straightforward to use a finer grid over which to do a systematic search. More generally we may allow continuously across the interval , and to use numerical routines, and choose to minimize the residual sum of squares after a least squares fit. Not that we can approximate the distribution of the log periodogram accordingly only if we demodulate, as otherwise the distribution is shifted in location by a constant depending on . In this case the correlation between the periodogram at frequencies spaced apart is non-negligible, thus necessitating usage of weighted least squares.

6 Discussion

This paper has illustrated the inherent problems with seasonally persistent processes and approximation based on the periodogram. We have demonstrated that realigning the grid of frequencies at which the periodogram is evaluated will simplify the distributional properties and enables us to specify a useful approximation to a likelihood function. Analysis of seasonal persistence will usually be based on frequency domain descriptions. For the usual Fourier grid, the distributional properties of the periodogram are generally not useful for SPPs, if given by previously derived theory Olhede et al. (2004). This paper shows how a small technical adjustment to the DFT to the DDFT alters the distributional properties substantially, making analytic investigation of the properties of the MLEs possible. The theoretical and practical utility of this adjustment is apparently under-appreciated in the literature. Potentially, even for short memory models (with bounded but highly peaked spectra) for moderate values of , there will be an advantage in demodulation.

In this paper, attempts have been made to fill the gaps of current theory. To avoid the problems associated with the location of the singularity, Giraitis et al. (2001) constrained the maximization of the Whittle likelihood to a set of frequencies spaced apart, where the likelihood performs well under the assumption that the true value of location of the singularity is constrained to this set. Their important result states that . In fact, this is ensured (informally) by picking a Fourier frequency a distance from the singularity, hence not even necessarily the closest Fourier frequency. In contrast, we have studied the sensitivity of the likelihood of the periodogram to perturbations in , and found that the estimate of for large finite sample sizes is very sensitive to such variation, thus clarifying that despite the very rapid convergence of to the potential misalignment of the Fourier grid with the unknown must be acknowledged. We also derive the large sample form of the distribution of and where the latter when re-normalised appropriately has a scaled Cauchy distribution.

Our results relate to frequency domain based analysis at some grid of frequencies. For processes with absolutely convergent autocovariance sequences for large samples, no gain is made by a particular choice of Fourier domain gridding, however for processes with seasonal persistence it is of fundamental importance to chose the correct grid alignment, even in large samples, as this simplifies the distributional results substantively.

Simulated examples show the superiority of our approach in finite sample situations. Furthermore, the methodology has the philosophical advantage of acknowledging the estimation of . While other methods do well asymptotically for estimation of the long memory parameter, it is worth noting that for any fixed (maybe large) sample-size, improvements can usually be found by explicitly considering the estimation of separately. The profile likelihood methods can be simply employed in the extended GPH estimator discussed by Hidalgo and Soulier (2004), extending the ideas to semi-parametric models, and facilitating a tractable analysis.

References

- Abramovich et al. (2006) Abramovich, F., Benjamini, Y., Donoho, D. L., and Johnstone, I. M. (2006). Adapting to unknown sparsity by controlling the false discovery rate. Ann. Statist., 34, 584–653.

- Andel (1986) Andel, J. (1986). Long memory time series models. Kybernetika, 22, 105–23.

- Beran (1994) Beran, J. (1994). Statistics for Long-Memory Processes. Chapman and Hall, London.

- Beran and Gosh (2000) Beran, J. and Gosh, S. (2000). Estimation of the dominating frequency for stationary and nonstationary fractional autoregressive models. J. Time Ser. Anal., 21, 517–533.

- Berger et al. (1999) Berger, J. O., Liseo, B., and Wolpert, R. L. (1999). Integrated likelihood methods for eliminating nuisance parameters. Statistical Science, 14, 1–28.

- Brillinger (1975) Brillinger, D. (1975). Time Series, Data Analysis and Theory. New York, USA: Holt, Rhinehart and Winston.

- Candès and Tao (2004) Candès, E. and Tao, T. (2004). Near optimal signal recovery from random projections: Universal encoding strategies. Technical report, Caltech.

- Chen et al. (2000) Chen, Z. G., Wu, K. H., and Dahlhaus, R. (2000). Hidden frequency estimation with data tapers. J. Time Ser. Anal., 21, 113–142.

- Cheng and Taylor (1995) Cheng, R. C. H. and Taylor, L. (1995). Non-regular maximum likelihood problems. J. Roy. Statist. Soc. B, 57, 3–44.

- Coifman and Donoho (1995) Coifman, R. R. and Donoho, D. L. (1995). Translation-invariant denoising. In A. Antoniadis and G. Oppenheim (Eds.), Wavelets and Statistics (Lecture Notes in Statistics, Volume 103), pp. 125–150. New York: USA: Springer-Verlag.

- Contreras-Cristan et al. (2006) Contreras-Cristan, A., Gutierrez-Pena, E., and Walker, S. G. (2006). A note on Whittle’s likelihood. Comm. Stats. – Sim. Comp., 35, 857–875.

- Coursol and Dacunha-Castelle (1982) Coursol, J. and Dacunha-Castelle, R. (1982). Remarks on the approximation on the likelihood function of a stationary Gaussian process. Theory Prob. Appl, 27, 162–67.

- Donoho (2006) Donoho, D. L. (2006). Compressed sensing. IEEE Transactions on Information Theory, 52, 1289–1306.

- Dzhamparidze and Yaglom (1983) Dzhamparidze, K. O. and Yaglom, A. M. (1983). Spectrum parameter estimation in time series analysis. In P. Krishnaiah (Ed.), Developments in Statistics, Volume 4, pp. 1–181. New York: Academic Press.

- Geweke and Porter-Hudak (1983) Geweke, J. and Porter-Hudak, S. (1983). The estimation and application of long memory time series models. J. Time Ser. Anal. 4(4), 221–238.

- Gil-Alana (2002) Gil-Alana, L. A. (2002). Seasonal long memory in the aggregate output. Econ. Lett. 74(3), 333–7.

- Giraitis et al. (2001) Giraitis, L., Hidalgo, J., and Robinson, P. M. (2001). Gaussian estimation of parametric spectral density with unknown pole. Ann. Statist., 29, 987–1023.

- Gradshteyn et al. (1994) Gradshteyn, I. S., Ryzhik, I. M., and Jeffrey, A. (1994). Table of Integrals, Series, and Products. New York: Academic Press.

- Gray et al. (1989) Gray, H. L., Zhang, N. F., and Woodward, W. (1989). On generalized fractional processes. J. Time Ser. Anal., 10, 233–57.

- Grenander and Szegö (1984) Grenander, U. and Szegö, G. (1984). Toeplitz Forms and their Applications (2 ed.). Chelsea Publishing Company, New York.

- Hannan (1973) Hannan, E. J. (1973). Estimation of frequency. J. Appl. Prob., 10, 510–519.

- Hannan (1986) Hannan, E. J. (1986). A law of the iterated logarithm for an estimate of frequency. Stochastic Processes And Their Applications, 22, 103–109.

- Hidalgo (2005) Hidalgo, J. (2005). Semiparametric estimation for stationary processes whose spectra have an unknown pole. Ann. Statist. 33(4), 1843–1889.

- Hidalgo and Soulier (2004) Hidalgo, J. and Soulier, P. (2004). Estimation of the location and exponent of the spectral singularity of a long memory process. J. Time Ser. Anal. 25(1), 55–81.

- Hosoya (1974) Hosoya, Y. (1974). Estimation Problems on Stationary Time-Series Models. Ph. D. thesis, Yale University.

- Huerta and West (1999) Huerta, G. and West, M. (1999). Priors and component structure in autoregressive time series models. J. Roy. Statist. Soc. B 61(4), 881–99.

- Hurvich and Beltrao (1993) Hurvich, C. M. and Beltrao, K. (1993). Asymptotics for the low frequency ordinates of the periodogram of a long memory time series. J. Time Ser. Anal., 14, 455–472.

- Hurvich et al. (1998) Hurvich, C. M., Deo, R., and Brodsky, J. (1998). The mean square error of Geweke and Porter-Hudak’s estimator of the memory parameter of a long-memory time series. J. Time Ser. Anal., 19, 19–46.

- Isserlis (1918) Isserlis, L. (1918). On a formula for the product-moment coefficient of any order of a normal frequency distribution in any number of variables. Biometrika, 12, 134–139.

- Johnson and Kotz (1970) Johnson, N. I. and Kotz, S. (1970). Continuous Univariate Distributions, Vol. 2. New York, USA: Wiley.

- Lapsa (1997) Lapsa, P. (1997). Determination of Gegenbauer-type random process models. Sig. Proc., 63, 73–90.

- Olhede et al. (2004) Olhede, S. C., McCoy, E. J., and Stephens, D. A. (2004). Large sample properties of the periodogram estimator of seasonally persistent processes. Biometrika 91(3), 613–628.

- Ooms (2001) Ooms, M. (2001). A seasonal periodic long memory model for monthly river flows. Env. Modell. Soft., 16, 559–69.

- Pei and Ding (2004) Pei, S. C. and Ding, J. J. (2004). Generalized eigenvectors and fractionalization of offset dfts and dcts. IEEE Trans. Sig. Proc., 52, 2032–2046.

- Porter-Hudak (1990) Porter-Hudak, S. (1990). An application of the seasonal fractionally differenced model to the monetary aggregates. J. Amer. Statist. Assoc., 85, 338–344.

- Rathouz et al. (2002) Rathouz, P. J., Satten, G. A., and Carroll, R. J. (2002). Semiparametric inference in matched case-control studies with missing covariate data. Biometrika 89(4), 905–916.

- Robins et al. (1994) Robins, J. M., Rotnitsky, A., and Zhao, L. P. (1994). Estimation of regression coefficients when some regressors are not always observed. J. Amer. Statist. Assoc., 89, 846–866.

- Robinson (1995) Robinson, P. M. (1995). Log-periodogram regression of time-series with long-range dependence. Ann. Statist., 23, 1048–72.

- Sweeting (1980) Sweeting, T. J. (1980). Uniform asymptotic normality of the maximum likelihood estimator. Ann. Statist., 8, 1375–81.

- Sweeting (1992) Sweeting, T. J. (1992). Asymptotic ancillarity and conditional inference for stochastic processes. Ann. Statist., 20, 580–589.

- Taniguchi and Kakizawa (2000) Taniguchi, M. and Kakizawa, Y. (2000). Asymptotic Theory of Statistical Inference for Time Series. New York: Springer.

- Thomson (1990) Thomson, D. J. (1990). Time-series analysis of holocene climate data. Phil. Trans. Roy. Statist. Soc. Lond. A, 330, 601–616.

- v. Sachs (1993) v. Sachs, R. (1993). Detecting periodic components in stationary time series by an improved non-parametric procedure. In Proceedings of the International Conference on Applications of Time Series in Astronomy and Meteorology, pp. 115–118. University of Padova.

- Walker (1964) Walker, A. M. (1964). Asymptotic properties of least squares estimates of the spectrum of a stationary non-deterministic time series. J. Austr. Math. Soc., 4, 363–384.

- Walker (1965) Walker, A. M. (1965). Some asymptotic results for the periodogram of a stationary time series. J. Austr. Math. Soc., 5, 107–128.

- Whitcher (2004) Whitcher, B. (2004). Wavelet-based estimation for seasonal long-memory processes. Technometrics 46(2), 225–238.

- Whittle (1951) Whittle, P. (1951). Prediction and regulation by linear least-square methods. Almquist & Wicksell, Uppsala, Sweden.

| N | bias () | sd() | 95% interval | ||

|---|---|---|---|---|---|

| 1024 | 0.30 | 0.8125 | 1.0218 | 0.7793 | (0.1406, 0.1453) |

| 1024 | 0.40 | 1.2402 | 0.5829 | 0.8262 | (0.1416, 0.1442) |

| 1024 | 0.45 | 0.6699 | 0.3574 | 0.6424 | (0.1421, 0.1435) |

| 2048 | 0.30 | -4.4170 | 0.5355 | 0.7461 | (0.1414, 0.1439) |

| 2048 | 0.40 | 0.1699 | 0.3011 | 0.6511 | (0.1422, 0.1435) |

| 2048 | 0.45 | 0.7178 | 0.1958 | 0.5286 | (0.1425, 0.1433) |

| 4096 | 0.30 | 1.1035 | 0.2770 | 0.9237 | (0.1422, 0.1436) |

| 4096 | 0.40 | 0.4150 | 0.1459 | 0.9518 | (0.1426, 0.1432) |

| 4096 | 0.45 | -0.5254 | 0.0941 | 1.0443 | (0.1426, 0.1431) |

| 8192 | 0.30 | 0.9830 | 0.2031 | 0.9516 | (0.1424, 0.1433) |

| 8192 | 0.40 | 0.2851 | 0.1450 | 0.9986 | (0.1426, 0.1432) |

| 8192 | 0.45 | 0.1254 | 0.0722 | 1.0283 | (0.1426, 0.1431) |

| N | bias() | sd() | 95% interval | |

|---|---|---|---|---|

| 1024 | 0.30 | -2.3159 | 1.1575 | (0.1406,0.1455) |

| 1024 | 0.40 | -9.8354 | 0.6413 | (0.1416,0.1445) |

| 1024 | 0.45 | -17.3549 | 0.4460 | (0.1416,0.1436) |

| 2048 | 0.30 | -1.7787 | 0.6196 | (0.1411,0.1440) |

| 2048 | 0.40 | 3.5435 | 0.3731 | (0.1421,0.1436) |

| 2048 | 0.45 | 7.6451 | 0.2694 | (0.1426,0.1436) |

| 4096 | 0.30 | 0.2720 | 0.2882 | (0.1423,0.1436) |

| 4096 | 0.40 | -1.7299 | 0.1495 | (0.1426,0.1433) |

| 4096 | 0.45 | -3.4389 | 0.0920 | (0.1426,0.1431) |

| 8192 | 0.30 | -0.1842 | 0.2082 | (0.1424,0.1433) |

| 8192 | 0.40 | -0.2633 | 0.1451 | (0.1426,0.1432) |

| 8192 | 0.45 | -1.1890 | 0.0712 | (0.1426,0.1431) |

| N | mean | bias () | sd () | 95% interval | ||

|---|---|---|---|---|---|---|

| 1024 | 0.30 | 0.2990 | -9.6364 | 1.9200 | 0.8662 | (0.2642,0.3370) |

| 1024 | 0.40 | 0.3995 | -4.9333 | 1.8672 | 0.7150 | (0.3600,0.4334) |

| 1024 | 0.45 | 0.4492 | -8.4182 | 1.6481 | 0.5222 | (0.4136,0.4773) |

| 2048 | 0.30 | 0.2998 | -1.7333 | 1.3862 | 0.8898 | (0.2709,0.3267) |

| 2048 | 0.40 | 0.3999 | -0.9515 | 1.3914 | 0.6902 | (0.3715,0.4249) |

| 2048 | 0.45 | 0.4499 | -0.8000 | 1.2573 | 0.4348 | (0.4246,0.4736) |

| 4096 | 0.30 | 0.3001 | 1.3333 | 0.9528 | 0.9523 | (0.2818,0.3200) |

| 4096 | 0.40 | 0.4003 | 2.9515 | 0.9475 | 0.8964 | (0.3812,0.4188) |

| 4096 | 0.45 | 0.4505 | 5.0612 | 0.9173 | 0.7909 | (0.4316,0.4663) |

| 8192 | 0.30 | 0.3001 | 1.0872 | 0.5028 | 1.0068 | (0.2912,0.3124) |

| 8192 | 0.40 | 0.3997 | -2.5643 | 0.4655 | 0.9099 | (0.3906,0.4088) |

| 8192 | 0.45 | 0.4497 | -3.0083 | 0.4056 | 0.9313 | (0.4414,0.4576) |

| N | mean | bias () | sd() | 95% interval | |

|---|---|---|---|---|---|

| 1024 | 0.30 | 0.3004 | 4.0909 | 2.0630 | (0.2606,0.3436) |

| 1024 | 0.40 | 0.4076 | 76.1111 | 2.2083 | (0.3636,0.4505) |

| 1024 | 0.45 | 0.4677 | 176.915 | 2.2807 | (0.4209,0.4997) |

| 2048 | 0.30 | 0.3015 | 14.9899 | 1.4696 | (0.2717,0.3293) |

| 2048 | 0.40 | 0.4077 | 76.8081 | 1.6748 | (0.3737,0.4414) |

| 2048 | 0.45 | 0.4680 | 180.012 | 1.9068 | (0.4324,0.4997) |

| 4096 | 0.30 | 0.3004 | 4.0204 | 0.9764 | (0.2816,0.3204) |

| 4096 | 0.40 | 0.4018 | 17.5306 | 1.0008 | (0.3816,0.4205) |

| 4096 | 0.45 | 0.4537 | 36.8571 | 1.0285 | (0.4337,0.4745) |

| 8192 | 0.30 | 0.3003 | 3.3474 | 0.5011 | (0.2874,0.3133) |

| 8192 | 0.40 | 0.4009 | 9.3895 | 0.4880 | (0.3900,0.4131) |

| 8192 | 0.45 | 0.4522 | 21.9531 | 0.4203 | (0.4401,0.4651) |

| Method | Model | BIC |

|---|---|---|

| Demodulated | GARMA(0,0) | 71.246 |

| GARMA(1,0) | 32.211 | |

| GARMA(0,1) | 27.153 | |

| GARMA(1,1) | 30.921 | |

| Standard Whittle | GARMA(0,0) | 73.330 |

| GARMA(1,0) | 42.794 | |

| GARMA(0,1) | 38.905 | |

| GARMA(1,1) | 42.021 |

| Estimate | 1.918 | 0.295 | -0.517 | 0.372 |

|---|---|---|---|---|

| Approx 95 % CI | (1.762,1.956) | (0.221,0.384) | (-0.675,-0.360) | (0.337,0.412) |

| Method | Model | BIC | BIC |

|---|---|---|---|

| Demodulated | GARMA(0,0) | 274.918 | 272.710 |

| GARMA(1,0) | 257.080 | 254.612 | |

| GARMA(0,1) | 266.528 | 262.589 | |

| GARMA(1,1) | 262.474 | 259.754 | |

| Standard | GARMA(0,0) | 278.567 | 281.290 |

| GARMA(1,0) | 243.009 | 260.035 | |

| GARMA(0,1) | 265.769 | 274.484 | |

| GARMA(1,1) | 246.742 | 265.129 |

| Demodulated | Estimate | 8.358 | 0.221 | 0.628 | 0.431 | |

|---|---|---|---|---|---|---|

| 95 % CI | (8.206,8.438) | (0.157,0.314) | (0.558,0.726) | (0.266,0.562) | ||

| Estimate | 8.295 | 0.234 | 0.644 | 0.401 | ||

| 95 % CI | (8.290,8.391) | (0.156,0.311) | (0.558,0.728) | (0.252,0.556) | ||

| Standard | Estimate | 8.409 | 0.156 | 0.629 | 0.520 | |

| 95 % CI | (8.222,8.497) | (0.133,0.305) | (0.562,0.736) | (0.286,0.594) |

| Demodulated | Estimate | 2.366 | 0.237 | 0.782 |

|---|---|---|---|---|

| Approx 95 % CI | (1.452,2.399) | (0.215,0.254) | (0.728,0.833) | |

| Standard | Estimate | 2.247 | 0.235 | 0.778 |

| Approx 95 % CI | (1.402,2.381) | (0.215,0.255) | (0.730,0.833) |

A Appendix: Proofs

A.1 Expectation of the Periodogram at the Pole

Starting with the same method of calculation as in Olhede et al. (2004, p. 623) we find a large approximation to the expected value of the periodogram at , after demodulation via . We have

| (A-1) | |||||

This result implicitly defines . The final line follows from Gradshteyn et al. (1994, §3.823). From equation (3),

as . Thus after demodulation, the expectation at the singularity is given by equation (A-1):

A.2 Bounding the Covariance Contributions

Under Gaussianity of the original time series, the DDFT will also be jointly proper complex Gaussian, thus we only need only to approximate for large the first and second order joint properties of these variables; the zeroth order properties are given in Appendix A.1, in conjunction with the results in Olhede et al. (2004).

We consider the discontinuities of the likelihood of the DDFT coefficients explicitly, and also the effects of ignoring the weak correlation between the Fourier coefficients near the pole (see Robinson (1995)). It is easier to deal with the demodulated sequence only, and so we shall only evaluate the frequency domain quantities at frequencies from (14). Let and take and As we only consider demodulation by we in this section suppress the subscript . We note that with for even and for odd, and similarly for , then

Let , and let Twice the log-likelihood based on the sample takes the form:

| (A-3) | |||||

where

Note that Also, The latter statement holds as the magnitude of this object can be bounded by considering the trace of the matrix and the fact that for the covariance terms can be bounded by (cf Robinson (1995)). If, for , we consider the terms in the log-likelihood involving and , then these are . The higher order terms are obtained by inverting the covariance matrix, and the second term coming directly from the order of the contributions. We write , for and let .

When summing the covariance terms we need to split up the terms indexed by negative and positive into two sum. Consider one of the two sums, and sum the contributions over indices , denoting the sum . To formally derive this for contributions to the left and right of the pole, we can use twice this term, and the order of the contributions are the most important result. Then we note that using Minkowski inequality arguments:

Note that is for any choice of and , . Thus as is we can ignore the covariance contributions. Asymptotically, using the likelihood from equation (16) yields equivalent results to using the likelihood constructed from independent exponential random variables with non-equal variances, due to the weak correlation between the Fourier coefficients.

A.3 Additional Notation

Define and denote the true values of the parameters by We suppress the dependence on other parameters, i.e. the dependence on and . Consider first expansions of the log-likelihood defined by equation (16), . Let

denote the matrix of second partial derivatives. Furthermore, it is convenient to introduce additional random variables, required to study the properties of the score and the observed Fisher information. We denote by and the quantities and respectively, and by and the standardized periodogram, derivative of the periodogram wrt the and the second derivative of the periodogram wrt to the all evaluated on the shifted grid. Then

These quantities can be written in terms of the real and imaginary part of the DDFT and its derivatives, and so we define for

| (A-4) |

for , where the sum over ranges over . Also, let

be the corresponding suitably standardized quantities. We shall also derive expressions for the expectation of and and these will be denoted and respectively. Their variances take quite complicated forms, and we denote the theoretical constants that give their forms for and via and where the first of these terms is a rough approximation to the variance of More details follow later in the text when appropriate. Furthermore, the covariances of the th and th DDFT coefficients and their derivatives, are denoted by , and respectively.

A.4 Zeroth Order Properties

To acknowledge the dependence of the likelihood on the indices and , and the fact that these indices depend on , we thus in this section write explicitly . Note that For any finite value of this dependence introduces a discontinuity in the log-likelihood in the form of a jump when the demodulation makes the range to the left decrease by one, and the range on the right increase by one, or vice-versa. This fact is inconvenient for our calculations, as it makes the log-likelihood discontinuous and hence not differentiable. However, it transpires that the magnitude of the discontinuities are of an order that can be ignored for large sample sizes, as will be shown by the first proposition, so that subsequent calculations will be in terms of where and are treated as fixed with respect to and of order

Proposition 7

Consider the log-likelihood at and assume that Without loss of generality, assume that so that . Let

be the magnitude of the discontinuity introduced by perturbing Then

and for every

Proof: (Sketch) It is straightforward to show that the discontinuities, , in the likelihood are random quantities with mean and variance that are , so after standardization it follows from the weak law of large numbers that and the result follows. Full details are omitted.

This difference between the log-likelihoods at different values of that induce a change of the grid is We can therefore apply arguments such as those developed by Coursol and Dacunha-Castelle (1982), to justify the usage of a form of the likelihood which ignores the the jump in the indices, when deriving the properties of using a form of the likelihood that does experience discontinuities as the value of alters. We may from the above calculations note that for large samples it is equivalent to use or in the analysis of the data; see also detailed discussion by Dzhamparidze and Yaglom (1983). For our weak convergence result, we standardize the log-likelihood by a factor of as the log-likelihood terms are both The log-likelihoods are constructed from a data-sample of size and so we can ignore any contribution of order Then will be , and we shall discuss limits of properties expressed in terms of this standardized quantity. Finally, informally, whilst any individual term is contributing to the likelihood, on differentiating the log-likelihood, this is no longer true - the individual contributions to the score in will be near the pole, and away from the pole. This effect renders the discontinuities even of lesser importance. Note that we can establish a large sample approximation to the distribution of the standardized log likelihood. We approximate the sum by an integral and as the correlation between the Fourier coefficients is sufficiently weak we have

These results for the entire log likelihood at any fixed value of the parameters agree with standard likelihood theory. We shall see that the behaviour of the pole is such that subsequently no result for the estimation of the pole follows as standard likelihood theory would make us anticipate. However, with a suitable standardization, the properties of the MLEs and the likelihood are still tractable.

A.5 Existence and Consistency Proof

The existence of the ML estimators is guaranteed as it is easy to show that the log-likelihood is everywhere bounded on the parameter space. The proof of consistency proceeds very similarly to Giraitis et al. (2001), who assume that the maximisation over is over a grid of frequencies, where is each grid-point is spaced apart. This is a sensible choice as the estimation is most often carried out over the Fourier frequency grid via the DFT. Define

and note that this constrains to integrate to zero. Giraitis et al. (2001) show strong convergence of the estimated location of the singularity to the point on the grid closest to the true value of the pole, using the likelihood defined by equation (8).

The likelihood approximation defined in Theorem 2 cannot be treated identically to the function of defined in (8), as the Fourier transform in the former likelihood is calculated at a different set of frequencies whenever a different value of is picked. However to compare the magnitude of the log-likelihood at and at we need to compare likelihood based on different Fourier grids. This may seem problematic, but recall that the DDFT is a linear orthogonal transform, and so both likelihoods may be directly related to the likelihood of the time domain sample whatever grid is used. It is hence suitable to compare the magnitude of the likelihood of the DDFT at different grids. To be able to do this, we introduce some extra notation. Recall the demodulated grid First, define Thus at any value of when the true value of the pole is but the likelihood is evaluated at a grid evenly spaced around is then the index of the frequency on the grid demodulated by that is closest to . Thus , and we define uniquely by taking the least of possible values is the pole is evenly spaced between two demodulated Fourier frequencies. Similarly define and . Thus is the demodulated Fourier frequency corresponding to whilst is the demodulated Fourier frequency closest to Note that using the triangle inequality

| (A-5) |

This allows us to consider the properties of the log-likelihood at the same grid explicitly, as . If we establish the result for we can redefine to derive the same result for In the vein of Giraitis et al. (2001), to show consistency, we fix and consider choosing such that

| (A-6) |

Let

We may obtain a bound for (A-6), , by considering

| (A-7) |

Define a subset of the parameter space defined for each fixed constant by

Let . Analogous to Giraitis et al., we bound (A-7) by

| (A-8) |

Note that the constant (see equation (A-1)) does not explicitly depend on or (although the bias is computed at a fixed ). Also denote the Kronecker-delta by as usual. Consider first

where

where in (1) we have defined and as in Giraitis et al. (2001). We can bound the probability in (A-8), in a similar fashion:

Most terms are the same as in Giraitis et al. (2001), and bound in an identical fashion, apart from and Clearly

Hence the result follows, see Theorem 3.1 in Giraitis et al. (2001). The proof follows Giraitis et al.’s and thus for a fixed grid with even spacing from shows that the maximiser in terms of of becomes close to the point on the grid closest to which by the properties of the grid has to be at most from This obviously is not the distance between the maximiser and but can be used to show convergence in probability. This strategy lets us avoid dealing with problems in the singularity of the likelihood, as well as the local periodic ripples.

A.6 First Order Properties of Derivatives of the Likelihood

Proposition 8

For an SPP with parameters , the expectation of the score evaluated at the is zero, that is .

Proof: To deal with the statistical properties, we first note the expectation of the standardized periodogram as given in Olhede et al. (2004), and Lemma 1 in this proof, so that

by results derived from Robinson (1995). For large , the second order properties of the score is dominated by the terms, that are distributed like quadratic forms of correlated normal random variables. We start by deriving the expectation of in terms of the trigonometrical forms defined in equation (A-4). We find that:

| (A-9) | |||||

this defining . From this expression it is obvious that . For large we have that where to derive this result, consider the decomposition

As in Robinson (1995) we bound the individual contributions of these integrals. Using identical arguments, we find for ,

as the integral is zero. Thus when ,