On the One-Dimensional Optimal Switching Problem

Abstract.

We explicitly solve the optimal switching problem for one-dimensional diffusions by directly employing the dynamic programming principle and the excessive characterization of the value function. The shape of the value function and the smooth fit principle then can be proved using the properties of concave functions.

Key words and phrases:

Optimal switching problems, optimal stopping problems, Itô diffusions.2000 Mathematics Subject Classification:

60G40, 60J60, 93E201. Introduction

Stochastic optimal switching problems (or starting and stopping problems) are important subjects both in mathematics and economics. Switching problems were introduced into the study of real options by Brennan and Schwarz Brennan and Schwarz (1985) to determine the manager’s optimal decision making in resource extraction problems, and by Dixit Dixit (1989) to analyze production facility problems. A switching problem in the case of a resource extraction problem can be described as follows: The controller monitors the price of natural resources and wants to optimize her profit by operating an extraction facility in an optimal way. She can choose when to start extracting this resource and when to temporarily stop doing so, based upon price fluctuations she observes. The problem is concerned with finding an optimal starting/stopping (switching) policy and the corresponding value function.

There has been many recent developments in understanding the nature of the optimal switching problems. When the underlying state variable is geometric Brownian motion and for some special reward/cost structure Brekke and Øksendal Brekke and Øksendal (1994), Duckworth and Zervos Duckworth and Zervos (2001), Zervos Zervos (2003) apply a verification approach for solving the variational inequality associated with the optimal switching problem. By using a viscosity solution approach, Pham and Ly Vath Pham and Vath (2007) generalize the previous results by solving the optimal switching problem for more general reward functions. They do not assume a specific form but only Hölder continuity of the reward function. In contrast, our aim is to obtain general results that applies to all one-dimensional diffusions (in some switching problems a mean reverting process might be more reasonable model for the underlying state process). Also, we will not assume the Hölder continuity of the running reward function.

The verification approach applied in the above papers is indirect in the sense that one first conjectures the form of the value function and the switching policy and next verifies the optimality of the candidate function by proving that the candidate satisfies the variational inequalities. In finding the specific form of the candidate function, appropriate boundary conditions, including the smooth-fit principle, are employed. This formation shall lead to a system of non-linear equations that are often hard to solve and the existence of the solution to these system of equations is difficult to prove. Moreover, this indirect solution method is specific to the underlying process and reward/cost structure of the problem. Hence a slight change in the original problem often causes a complete overhaul in the highly technical solution procedures.

Our solution method is direct in the sense that we work with the value function itself. First we characterize the value function as the solution of two coupled optimal stopping problems. In other words we prove a dynamic programming principle. A proof of a dynamic programming principle for switching problems was given by Tang and Yong Tang and Yong (1993) assuming a Hölder continuity condition on the reward function. We give a new proof using a sequential approximation method (see Lemma 2.1 and Proposition 2.1) and avoid making this assumption. The properties of the essential supremum and optimal stopping theory for Markov processes play a key role in our proof. Second, we give a sufficient condition which guarantees that the switching regions hitting times of certain closed sets (see Proposition 2.2). Next, making use of our sequential approximation we show when the optimal switching problem reduces to an ordinary stopping problem (see Proposition 2.3). Finally, in the non-degenerate cases we construct an explicit solution (see Proposition 2.5) using the excessive characterization of the value functions of optimal stopping problem (which corresponds to the concavity of the value function after a certain transformation) Dayanik and Karatzas Dayanik and Karatzas (2003) (also see Dynkin Dynkin (1965), Alvarez Alvarez (2001, 2003)), see Lemma 2.3. In Proposition 2.5, we see that the continuation regions do not necessarily have to be connected. We give two examples, one of which illustrates this point. In the next example, we consider an problem in which the underlying state variable is an Ornstein-Uhlenbeck process.

It is worth mentioning the work of Pham Pham (2007), which provides another direct method to solve optimal switching problems through the use of viscosity solution technique. Pham shows that the value function of the optimal switching problem is continuously differentiable and is the classical solution of its quasi-variational inequality under the assumption that the reward function is Lipschitz continuous. Johnson and Zervos Johnson and Zervos (2009), on the other hand, by using a verification theorem, determine sufficient conditions that guarantee that the problem has connected continuation regions or is degenerate (see Section 5 and Theorem 7 of that paper). A somewhat related problem to the optimal switching problem we study here is the infinite horizon optimal multiple stopping problem of Carmona and Dayanik Carmona and Dayanik (2008), which was introduced to give a complete mathematical analysis of energy swing contracts. This problem is posed in the context of pricing American options when the holder of the option has multiple exercise rights. To make the problem non-trivial it is assumed that the holder chooses the consecutive stopping times with a strictly positive break period (otherwise the holder would use all his rights at the same time). It is difficult to explicitly determine the solution and Carmona and Dayanik describe a recursive algorithm to calculate the value of the American option. In the switching problems, however, there are no limits on how many times the controller can switch from one state to another and one does not need to assume a strictly positive break period. Moreover, we are able to construct explicit solutions. Other related works include, Hamadène and Jeanblanc Hamadène and Jeanblanc (2007), which analyzes a finite time horizon optimal switching problem with a general adapted observation process using the recently developed theory of reflected stochastic backward differential equations. Carmona and Ludkovski Carmona and Ludkovski (2008) focus on a numerical resolution based on Monte-Carlo regressions. Recently an interesting connection between the singular and the switching problems was given by Guo and Tomecek Guo and Tomecek (2008).

The rest of the paper is organized as follows: In Section 2.1 we define the optimal switching problem. In Section 2.2 we study the problem in which the controller only can switch finitely many times. Using the results of Section 2.2, in Section 2.3 we give a characterization of the optimal switching problem as two coupled optimal stopping problems. In Section 2.4, we show that the usual hitting times of the stopping regions are optimal. In Section 2.5 we give an explicit solution. In Section 2.6 we give two examples illustrating our solution.

2. The Optimal Switching Problem

2.1. Statement of the Problem

Let be a complete probability space hosting a Brownian motion . Let be natural filtration of . The controlled stochastic processes, with state space (), is a continuous process, which is defined as the solution of

| (2.1) |

in which the right-continuous switching process is defined as

| (2.2) |

where and for all . Here, the sequence is an increasing sequence of -stopping times with , almost surely (a.s.). Here, . The stopping time when both and are natural boundaries. We will denote the set of such sequences by . We will assume that the boundaries are either absorbing or natural.

We are going to measure the performance of a strategy

by

| (2.3) |

in which is the immediate benefit/cost of switching from to . We assume that is continuous in its first variable and

| (2.4) |

for some strictly positive constants . Moreover, we assume that

| (2.5) |

We also assume that the running benefit is a continuous function and satisfies the linear growth condition:

| (2.6) |

for some strictly positive constant . This assumption will be crucial in what follows, for example it guarantees that

| (2.7) |

for some , if we assume that the discount rate is large enough, which will be a standing assumption in the rest of our paper (see page 5 of Pham Pham (2007)).

The goal of the switching problem then is to find

| (2.8) |

and also to find an optimal if it exists.

2.2. When the Controller Can Switch Finitely Many Times

For any stopping time let us define

| (2.9) |

In this section, we will consider switching processes of the form

| (2.10) |

in which the stopping times . By we will denote the solution of (2.1) when we replace with . So with this notation we have that

| (2.11) |

We assume a strong solution to (2.11) exits and that

| (2.12) |

for some positive constant , which guarantees the uniqueness of the strong solution. We should note that

| (2.13) |

The value function of the problem in which the controller chooses switches is defined as

| (2.14) |

We will denote the value of making no switches by , which we define as

| (2.15) |

which is well defined due to our assumption in (2.7).

Let be the first hitting time of by , and let be a fixed point of the state space. We set:

It should be noted that and consist of an increasing and a decreasing solution of the second-order differential equation in where is the infinitesimal generator of when in (2.11). They are linearly independent positive solutions and uniquely determined up to multiplication. For the complete characterization of the functions and corresponding to various types of boundary behavior see Itô and McKean Itô and McKean (1974). For future use let us define the increasing functions

| (2.16) |

In terms of the Wronskian of and by

| (2.17) |

we can express as

| (2.18) |

, see e.g. Karlin and Taylor Karlin and Taylor (1981) pages 191-204 and Alvarez Alvarez (2004) page 272.

Now, consider the following sequential optimal stopping problems:

| (2.19) |

where , and .

Lemma 2.1.

For , we have that , for all and . Moreover, is continuous in the -variable.

Proof.

See Appendix ∎

2.3. Characterization of the Optimal Switching Problem as Two Coupled Optimal Stopping Problems

Using the results of the previous section, here we will show that the optimal switching problem can be converted into two coupled optimal stopping problems.

Corollary 2.1.

For all and , the increasing sequence converges:

| (2.20) |

Moreover, is continuous in the -variable.

Proof.

Since , it follows that is a non-decreasing sequence and

| (2.21) |

Assume that . Let us fix and . For a given , let be an -optimal strategy, i.e.,

| (2.22) |

Note that depends on . Now , and

| (2.23) |

Let be the smallest time that reaches or , and be the smallest time reaches or .

Since as , almost surely, it follows from the growth assumptions on and that

| (2.24) |

and

| (2.25) |

for large enough . It follows from (2.24) and (2.25) that

| (2.26) |

Therefore, using (2.22) we get

| (2.27) |

Since is arbitrary, this along with (2.21) yields the proof of the corollary when .

When , then for each positive constant , there exists such that . Then, if we choose as before with , we get , which leads to

| (2.28) |

Since is arbitrary, we have that

| (2.29) |

It is clear from our proof that converges to locally uniformly. Since is continuous, the continuity of follows.

∎

The next result shows that the optimal switching problem is equivalent to solving two coupled optimal stopping problems.

Proposition 2.1.

The value function of the optimal switching problem has the following representation for any and :

| (2.30) |

which can also be written as

| (2.31) |

due to the strong Markov property of .

Proof.

First note that

| (2.32) |

as a result of Proposition 2.1 and Lemma 2.1. Therefore, it follows from (2.19) that

| (2.33) |

To obtain the opposite inequality let us choose such that

| (2.34) |

Then by the monotone convergence theorem

| (2.35) |

This proves the statement of the proposition. ∎

Remark 2.1.

-

(i)

It is clear that the result of the previous proposition holds even for finite horizon problems, which can be shown by making slight modifications (by setting the cost functions to be equal to zero after the maturity) to the proofs above.

-

(ii)

Also, if there are more than two regimes the controller can choose from (2.31) can be modified to read

(2.36) where

(2.37) and is the set of regimes.

2.4. A Class of Optimal Stopping Times

In this section, using the classical theory of optimal stopping times, we will show that hitting times of certain kind are optimal. We will first show that the assumed growth condition on and leads to a growth condition on the value function , from which we can conclude that is finite on .

Lemma 2.2.

There exists a constant such that

| (2.38) |

In fact, the same holds for all , .

Proof.

As in Pham Pham (2007) due to the linear growth condition on and , the process defined in (2.1) satisfies the second moment estimate

| (2.39) |

for some positive constant . Due to the linear growth assumption on we have that

| (2.40) |

for some large enough constant . Here the second inequality follows from the Jensen’s inequality and the fact that . Also recall that we have assumed the discount factor to be large enough. (This is similar to the assumption in Pham Pham (2007)). Taking the supremum over in (2.40) we obtain that

| (2.41) |

The linear growth of can be shown similarly. ∎

Proposition 2.2.

Let us define

| (2.42) |

Let us assume that and and the following one of the two hold:

-

(1)

is absorbing, and is natural,

-

(2)

Both and are natural.

Then if for , , the stopping times

| (2.43) |

are optimal. Note that in (2.11) depends on , through its drift and volatility.

Proof.

Let us prove the statement for Case 1. First, we define

| (2.44) |

By Lemma 2.2 and satisfy a linear growth condition. We assumed that also satisfies a linear growth condition. Therefore the assumption on guarantees that , for . But then from Proposition 5.7 of Dayanik and Karatzas Dayanik and Karatzas (2003) the result follows.

For Case 2, we will also need to show that

| (2.45) |

and use Proposition 5.13 of Dayanik and Karatzas Dayanik and Karatzas (2003). But the result is immediate since , and are bounded in a neighborhood of and , since is a natural boundary.

∎

Remark 2.2.

If both and are absorbing it follows from Proposition 4.4 of Dayanik and Karatzas Dayanik and Karatzas (2003) that the stopping times in (2.43) are optimal, since , and are continuous. Also, observe that when is absorbing (2.45) still holds since , . Similarly, when is absorbing in (2.44) is equal to zero.

Remark 2.3.

Since is strictly positive, it can easily seen from the definition that .

2.5. Explicit Solutions

In this section, we let and , and assume that is either natural or absorbing, and that is natural.

Proposition 2.3.

Let us introduce the functions

| (2.46) |

-

(i)

If for all we have that and , then .

-

(ii)

Let us assume that the dynamics of (2.1) do not depend on (as a result and we will denote by ). Then for all implies that . Similarly, if for all , then . (Observe that, in this case, the optimal switching problem reduces to an ordinary optimal stopping problem.)

Proof.

(i) For any , let us introduce

| (2.47) |

Using the strong Markov property of and (2.19) we can write

| (2.48) |

Since and , it follows from (2.48) that

If we assume that for we have that , , ; it follows from (2.48) that , , . For a given , we can carry out this induction argument to show that

Now using Lemma 2.1 and Corollary 2.1 we have that , which yields the desired result.

(ii) We will only prove the first statement since the proof of the second statement is similar. As in the proof of (i) for all implies that . On the other hand,

Let us assume that for

Since we have that , which in turn implies that

| (2.49) |

Using (2.49) we can write

| (2.50) |

The second equality in the above equation follows from the assumption that the dynamics of (2.1) do not depend on : Indeed, since the function is a value function of an optimal stopping problem, then it is positive and concave (see e.g. Proposition 5.11 of Dayanik and Karatzas Dayanik and Karatzas (2003)). On the other hand, by the same proposition of Dayanik and Karatzas Dayanik and Karatzas (2003) we note that is the smallest non-negative concave majorant of the function , which is non-negative and -concave, it follows that

Since the function is non-negative, it follows from (2.50) that . On the other hand,

thanks to our induction hypothesis. Using this induction on , we see that

for any given . At this point applying Lemma 2.1 and Corollary 2.1 we obtain that

∎

In the rest of this section we will assume that the dynamics of (2.1) do not depend on . We will denote by and by . We will also assume that , is continuously differentiable for .

Proposition 2.4.

Let us define

| (2.51) |

and

| (2.52) |

Here and are functional inverses of and , respectively. If is non-negative concave on then and . Similarly, if is non-negative concave on then and .

Proof.

Lemma 2.3.

Let us define

| (2.53) |

and

| (2.54) |

| (2.55) |

Then the following statements hold:

-

(i)

and are the smallest positive concave majorants of

(2.56) and

(2.57) respectively.

-

(ii)

.

-

(iii)

is piecewise linear on and

(2.58) Moreover, the function is concave on .

-

(iv)

is piecewise linear on and

(2.59) The function is concave on .

Proof.

(i). It follows from (2.31) that satisfies

| (2.60) |

The statement follows from Theorem 16.4 of Dynkin Dynkin (1965) (also see Proposition 5.11 of Dayanik and Karatzas Dayanik and Karatzas (2003)).

(iii), (iv). First, we want to show that is concave on . It is enough to show that

is concave on . But this can be shown using item (i). Now the rest of the statement follows since is the smallest concave majorant of . Proof of (iv) follows similarly. ∎

In the next proposition we will give sufficient conditions under which the switching regions are connected and provide explicit solutions for the value function of the switching problem. We will also show that the value functions of the switching problem , are continuously differentiable under our assumptions.

In what follows we will assume that , .

Proposition 2.5.

Let us assume that the function and defined in Proposition 2.3 satisfy

| (2.61) |

and that for some . Then

| (2.62) |

for some positive constants , and . Moreover the following statements hold:

-

(i)

If for some , then has the following form

(2.63) for a positive constant .

-

(ii)

If , for some , is of the form

(2.64) for positive constant and .

In both cases the value functions are continuously differentiable. As a result the positive , and can be determined from the continuous and the smooth fit conditions.

Before, we give the proof we will make two quick remarks.

Remark 2.4.

Note that for all . So when , we have that . The assumption that ensures that the controller prefers state 0 to state 1, which can also be seen from the form of the value function in (2.62).

Remark 2.5.

The following two identities can be checked to see when the functions , are concave:

| (2.65) |

and

| (2.66) |

where is the infinitesimal generator of .

Proof of Proposition 2.5. The proof is a corollary of Lemma 2.3. Let us denote . We will argue that . If we assume that , then it follows that and hence , where the last identity follows from Remark 2.3. Since , we obtain that for all . This contradicts our assumption on in (2.61).

Since and is concave on (by Lemma 2.3 (iii)) it follows that , due to the fact that is the smallest concave majorant of . As a result, thanks also to Lemma 2.3 (ii), we have that

| (2.67) |

for some constants that satisfies

| (2.68) |

which proves (2.62).

(i) Similarly, if we let , then we have that this quantity is a finite negative number and that . As a result,

| (2.69) |

for some constant that satisfies

| (2.70) |

Next, we are going to determine , , and making use of the fact that and are smallest non-negative majorants of and further. First observe that is continuously differentiable since by (2.18), is continuously differentiable. Second, by using (2.53) and (2.54) we obtain

| (2.71) |

and

| (2.72) |

It follows from Remark 2.3 that

| (2.73) |

As a result, we have that the function is differentiable on , for some . Along with the differentiability of the function , this observation yields that

| (2.74) |

for some . Similarly, the differentiability of on implies that

| (2.75) |

for some . ¿From (2.74) and (2.75) together with the fact that and are the smallest non-negative majorants of and , we can determine , , and from the following additional equations they satisfy

| (2.76) |

Using (2.53) we can write the value functions , as

| (2.77) |

and

| (2.78) |

Now, a direct calculation shows that the left derivative and the right derivative of are equal at . Similarly, one can show the same holds for the function at . This completes the proof of (i).

(ii) Let us denote and . The function is concave on the interval , by Lemma 2.3 (iv). Moreover, because is the smallest non-negative majorant of it follows that . Using the facts that is piecewise linear on , and , the last being equivalent to (this follows from our assumption on in (2.61), the relation between and pointed out in Remark 2.4, and our assumption on the set ), we can write as

from which (2.64) follows. Note that since the function is the smallest positive concave majorant of the function . The proof that the smooth fit property is satisfied at the boundaries follows similar line of arguments to the proof of item (i).

2.6. Examples

Example 2.1.

In this example we will show how changing the switching costs we can move from having one continuation regions (item (i) in Proposition 2.5) to disconnected continuation regions (item (ii) in Proposition 2.5). Let the running reward function in (2.3) be given by for with and . We assume that dynamics of the underlying state variable follow

where and are some given constants and

| (2.79) |

Case 1. A Connected continuation region. We assume that and . (Recall that .) Observe that our assumptions in Section 2.1, (2.12), (2.4) and (2.6) are readily satisfied. In what follows we will check the assumptions in item (i) of Proposition 2.5 hold. First, let us obtain functions, , , , , , , in terms of which we stated our assumptions. The increasing and decreasing solutions of the ordinary differential equation are given by and , where

Note that under the assumption , we have and . Observe that , (the main assumption of Proposition 2.2). It follows that and , in which

We can calculate , explicitly:

where since and . On the other hand,

and

The limits

| (2.80) |

Let us show that and for some . Remark 2.5 will be used to achieve this final goal.

| (2.81) |

which is negative only for large enough (since we assumed (2.79)). On the other hand,

| (2.82) |

which is negative only for small enough non-negative .

Thanks to Proposition 2.5 the value function is given by

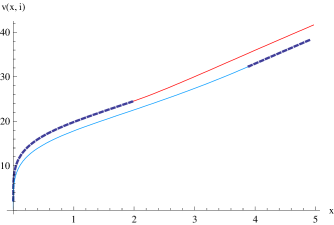

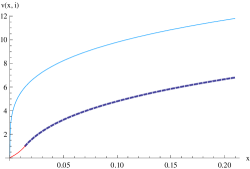

in which the positive constants , , and can be determined from continuous and smooth fit conditions. Figure 2.1 illustrates a numerical example. Note that since the closing cost is negative, for all .

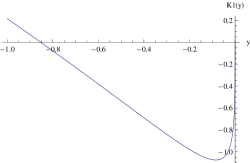

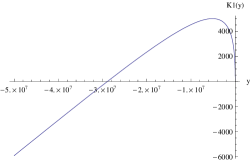

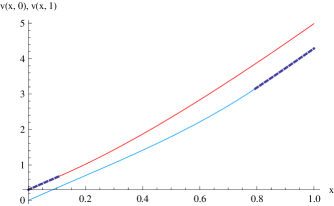

Case 2. Multiple continuation regions. We will change the value of switching from 1 to 0 and assume that it is positive, i.e., while we keep the assumption that . Clearly, . Moreover, the analysis of (2.82) easily shows that and . As a result has two real roots. This fact translates into the fact that for some . See Figure 2.2 for the shape of for a particular set of parameters.

(a)

(b)

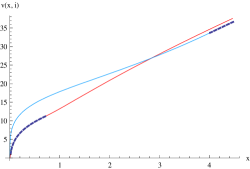

Thanks to Proposition 2.5, the value function is given by (2.64). Figure 2.3 displays the solution for a particular set of parameters.

(a)

(b)

Example 2.2.

Ornstein-Uhlenbeck process. The purpose of this exercise is to solve give an example of an optimal switching problem for a mean-reverting process. Let the dynamics of the state variable be given by

Let the value function be defined by

in which . Our assumptions in Section 2.1, (2.12), (2.4) and (2.6) are satisfied by our model. Let us introduce

| (2.83) |

where is the parabolic cylinder function; (see Borodin and Salminen Borodin and Salminen (2002)(Appendices 1.24 and 2.9), which is given in terms of the Hermite function as

| (2.84) |

Recall that Hermite function of degree and its integral representation

| (2.85) |

(see for example, Lebedev Lebedev (1972) (pages 284, 290)). In terms of the functions in (2.83) the fundamental solutions of and are given by

Observe that (the main assumption of Proposition 2.2). Since , we have

| (2.86) |

Note that the limits of the functions

and

are given by

When , then .

Let us show that and for some . For this purpose we will again use Remark 2.5.

| (2.87) |

which implies that the function is concave only , for some . On the other hand,

| (2.88) |

which implies that is concave only on for some . Now, as a result of Proposition 2.5, we have that

in which

and

The parameters, , , and can now be obtained from continuous and smooth fit since we know that the value functions , are continuously differentiable. See Figure 2.4 for a numerical example.

Appendix A Proof of Lemma 2.1

We will approximate the switching problem by iterating optimal stopping problems. This approach is motivated by Davis Davis (1993) (especially the section on impulse control) and Øksendal and Sulem Øksendal and Sulem (2005). To establish our goal we will use the properties of the essential supremum (see Karatzas and Shreve Karatzas and Shreve (1998), Appendix A) and the optimal stopping theory for Markov processes in Fakeev Fakeev (1971). A similar proof, in the context of “multiple optimal stopping problems”, is carried out by Carmona and Dayanik Carmona and Dayanik (2008).

For any stopping time , let us define

| (A.1) |

for , and

| (A.2) |

We will perform the proof of the lemma in four steps.

Step 1. If we can show that the family

| (A.3) |

is directed upwards, it follows from the properties of the essential supremum (see Karatzas and Shreve (1998,Appendix A)) that for all

| (A.4) |

for some sequence . Here, is the solution of (2.1) when we replace by which is defined as

| (A.5) |

We will now argue that (A.3) is directed upwards (see Karatzas and Shreve Karatzas and Shreve (1998) Appendix A for the definition of this concept ): For any , let us define the event

| (A.6) |

and the stopping times

| (A.7) |

Then and

| (A.8) |

and therefore is directed upwards.

Step 2. In this step we will show that

| (A.9) |

Let us fix . It follows from Step 1 that there exists a sequence such that

| (A.10) |

Here, is the solution of (2.1) when we replace by which is defined as

| (A.11) |

For every , we have that , and that

| (A.12) |

in which we take and is the solution of (2.1) when we replace by which is defined as

| (A.13) |

We can then write

| (A.14) |

Here, the first equality follows from the Monotone Convergence Theorem (here we used the boundedness assumption on , see (2.4)). Since is arbitrary this implies that the left-hand-side of (A.14) is greater than the right-hand-side of (A.9). Let us now try to show the reverse inequality. Let for any let be given by (2.10) and let be the solution of (2.1) when is replaced by . And let us define by

| (A.15) |

and let be the solution of (2.1) when is replaced by . Then

| (A.16) |

now taking the essential supremum on the right-hand-side over all the sequences in we establish the desired inequality. Our proof in this step can be contrasted with the approach of Hamadéne and Jeanblanc Hamadène and Jeanblanc (2007) which uses the recently developed theory of Reflected Backward Stochastic Differential Equations to establish a similar result. The proof method we use above is more direct. On the other hand, as pointed out on page 14 of Carmona and Ludkovski Carmona and Ludkovski (2008), it may be difficult to generalize the method of Hamadéne and Jeanblanc Hamadène and Jeanblanc (2007) to the cases when there are more than two regimes.

Step 3.

In this step we will argue that

| (A.17) |

in which , and that is continuous in the -variable. We will carry out the proof using induction. First, let us write as

| (A.18) |

Let be the shift operator . The third inequality in (A.18) follows from the strong Markov property of and and the fact that

| (A.19) |

for any , using which we can write

| (A.20) |

and

| (A.21) |

It is well known in the optimal stopping theory that (A.17) holds for , if

| (A.22) |

and

| (A.23) |

see Theorem 1 of Fakeev Fakeev (1971). (Fakeev requires continuity of . But this requirement is readily satisfied in our case since is continuous and since is continuous, by the continuity assumption of and (2.18).

Now let us assume that (A.17) when is replaced by and that is continuous in the -variable and show that (A.17) holds and is continuous in the -variable. ¿From Step 2 and the induction hypothesis we can write as

| (A.24) |

where the third equality follows since for , and the last equality can be derived using the strong Markov property of and . The functions and are continuous in the -variable and is assumed to satisfy the same property. On the other hand, we have that

| (A.25) |

satisfies , in which is defined in (A.22), since is an increasing sequence of functions. Therefore, Theorem 1 of Fakeev Fakeev (1971) implies that (A.17) holds. On the other hand, Lemma 4.2, Proposition 5.6 and Proposition 5.13 of Dayanik and Karatzas (2003) guarantee that is continuous. This concludes our induction argument and hence Step 3.

Step 4. In this step we will show that the statement of the lemma holds using the results proved in the previous steps.

By definition we already have that

| (A.26) |

Let us assume that the statement holds for replaced by . From the previous step and the induction hypothesis we have that

| (A.27) |

where the last equality follows from (A.21). This completes the proof.

References

- (1)

- Alvarez (2001) Alvarez, L. H. R. (2001). Singular stochastic control, linear diffusions, and optimal stopping: A class of solvable problems, SIAM Journal on Control and Optimization 39 (6): 1697–1710.

- Alvarez (2003) Alvarez, L. H. R. (2003). On the properties of -excessive mappings for a class of diffusions, Annals of Applied Probability 13 (4): 1517–1533.

- Alvarez (2004) Alvarez, L. H. R. (2004). A class of solvable impulse control problems, Appl. Math. and Optim. 49: 265–295.

-

Bayraktar and Egami (2007)

Bayraktar, E. and Egami, M. (2007).

On the one-dimensional optimal switching problem.

http://www.citebase.org/abstract?id=oai:arXiv.org:0707.0100 - Borodin and Salminen (2002) Borodin, A. N. and Salminen, P. (2002). Handbook of Brownian Motion Facts and Formulae, Birkhäuser, Boston.

- Brekke and Øksendal (1994) Brekke, K. A. and Øksendal, B. (1994). Optimal switching in an economic activity under uncertainty, SIAM Journal on Control and Optimization 32 (4): 1021–1036.

- Brennan and Schwarz (1985) Brennan, M. and Schwarz, E. (1985). Evaluating natural resource investments, Journal of Business 58: 135–157.

- Carmona and Dayanik (2008) Carmona, R. and Dayanik, S. (2008). Optimal multiple-stopping of linear diffusions and swing options, Mathematics of Operations Research 33 (2): 446–460.

- Carmona and Ludkovski (2008) Carmona, R. and Ludkovski, M. (2008). Pricing asset scheduling flexibility using optimal switching agreements, Applied Mathematical Finance 15 (6): 405–447.

- Davis (1993) Davis, M. H. A. (1993). Markov models and optimization, Vol. 49 of Monographs on Statistics and Applied Probability, Chapman & Hall, London.

- Dayanik and Karatzas (2003) Dayanik, S. and Karatzas, I. (2003). On the optimal stopping problem for one-dimensional diffusions, Stochastic Processes and their Applications 107 (2): 173–212.

- Dixit (1989) Dixit, A. (1989). Entry and exit decisions under uncertainty, Journal of Political Economy 97: 620–638.

- Duckworth and Zervos (2001) Duckworth, K. and Zervos, M. (2001). A model for investment decisions with switching costs., Annals of Applied Probability 11 (1): 239–260.

- Dynkin (1965) Dynkin, E. (1965). Markov processes, Volume II, Springer Verlag, Berlin.

- Fakeev (1971) Fakeev, A. G. (1971). Optimal stopping of a markov process, Theory of Probability and Applications 16: 694–696.

- Guo and Tomecek (2008) Guo, X. and Tomecek, P. (2008). Connections between singular control and optimal switching, SIAM J. Control Optim. 47(1): 421–443.

- Hamadène and Jeanblanc (2007) Hamadène, S. and Jeanblanc, M. (2007). On the starting and stopping problem: Applications in reversible investments, Mathematics of Operations Research 32(1): 182–192.

- Itô and McKean (1974) Itô, K. and McKean, H. P. (1974). Diffusion processes and their sample paths, Springer Verlag, New York.

- Johnson and Zervos (2009) Johnson, T. C. and Zervos, M. (2009). The explicit solution to a sequential switching problem with non-smooth data, to appear in Stochastics . Available at http://www.ma.hw.ac.uk/timj/inv.pdf and http://www.maths.lse.ac.uk/Personal/mihail/publications/johnson-zervos.pdf.

- Karatzas and Shreve (1998) Karatzas, I. and Shreve, S. E. (1998). Methods of Mathematical Finance, Springer-Verlag, New York.

- Karlin and Taylor (1981) Karlin, S. and Taylor, H. M. (1981). A Second Course in Stochastic Processes, Academic Press, Orlando, FL.

- Lebedev (1972) Lebedev, N. N. (1972). Special Functions and Their Applications, Dover Publications, New York.

- Øksendal and Sulem (2005) Øksendal, B. and Sulem, A. (2005). Applied Stochastic Control of Jump Diffusions, Springer Verlag, New York.

- Pham (2007) Pham, H. (2007). On the smooth-fit propoerty of one-dimensional optimal switching problems, Séminaire de Probabilités XL: 187–201.

- Pham and Vath (2007) Pham, H. and Vath, V. L. (2007). Explicit solution to an optimal switching problem in the two-regime case, SIAM Journal on Control and Optimization. 46 (2): 395–426.

- Tang and Yong (1993) Tang, S. J. and Yong, J. M. (1993). Finite horizon stochastic optimal switching and impulse controls with a viscosity solution approach, Stochastics Stochastics Rep. 45(3-4): 145–176.

- Zervos (2003) Zervos, M. (2003). A problem of sequential entry and exit decisions combined with discretionary stopping, SIAM Journal on Control and Optimization 42 (1): 397–421.