Accelerated Projected Gradient Method for Linear Inverse Problems with Sparsity Constraints

Abstract

Regularization of ill-posed linear inverse problems via penalization has been proposed for cases where the solution is known to be (almost) sparse. One way to obtain the minimizer of such an penalized functional is via an iterative soft-thresholding algorithm. We propose an alternative implementation to -constraints, using a gradient method, with projection on -balls. The corresponding algorithm uses again iterative soft-thresholding, now with a variable thresholding parameter. We also propose accelerated versions of this iterative method, using ingredients of the (linear) steepest descent method. We prove convergence in norm for one of these projected gradient methods, without and with acceleration.

1 Introduction

Our main concern in this paper is the construction of iterative algorithms to solve inverse problems with an -penalization or an -constraint, and that converge faster than the iterative algorithm proposed in [21] (see also formulas (7) and (8) below). Before we get into technical details, we introduce here the background, framework, and notations for our work.

In many practical problems, one cannot observe directly the quantities of most interest; instead their values have to be inferred from their effect on observable quantities. When this relationship between observable and interesting quantity is (approximately) linear, as it is in surprisingly many cases, the situation can be modeled mathematically by the equation

| (1) |

where is a linear operator mapping a vector space (which we assume to contain all possible “objects” ) to a vector space (which contains all possible data ). The vector spaces and can be finite– or infinite–dimensional; in the latter case, we assume that and are (separable) Hilbert spaces, and that is a bounded linear operator. Our main goal consists in reconstructing the (unknown) element , when we are given . If is a “nice”, easily invertible operator, and if the data are free of noise, then this is a trivial task. Often, however, the mapping is ill-conditioned or not invertible. Moreover, typically (1) is only an idealized version in which noise has been neglected; a more accurate model is

| (2) |

in which the data are corrupted by an (unknown) noise. In order to deal with this type of reconstruction problem a regularization mechanism is required [30]. Regularization techniques try, as much as possible, to take advantage of (often vague) prior knowledge one may have about the nature of . The approach in this paper is tailored to the case when can be represented by a sparse expansion, i.e., when can be represented by a series expansion with respect to an orthonormal basis or a frame [20, 11] that has only a small number of large coefficients. In this paper, as in [21], we model the sparsity constraint by adding an term to a functional to be minimized; it was shown in [21] that this assumption does indeed correspond to a regularization scheme.

Several types of signals appearing in nature admit sparse frame expansions and thus, sparsity is a realistic assumption for a very large class of problems. For instance, natural images are well approximated by sparse expansions with respect to wavelets or curvelets [20, 8].

Sparsity has had already a long history of successes. The design of frames for sparse representations of digital signals has led to extremely efficient compression methods, such as JPEG2000 and MP3 [39]. A new generation of optimal numerical schemes has been developed for the computation of sparse solutions of differential and integral equations, exploiting adaptive and greedy strategies [12, 13, 14, 17, 18]. The use of sparsity in inverse problems for data recovery is the most recent step of this concept’s long career of “simplifying and understanding complexity”, with an enormous potential in applications [2, 9, 15, 19, 21, 22, 23, 25, 24, 33, 35, 34, 38, 40, 44]. In particular, the observation that it is possible to reconstruct sparse signals from vastly incomplete information just seeking for the -minimal solutions [7, 6, 26, 41] has led to a new line of research called sparse recovery or compressed sensing, with very fruitful mathematical and applied results.

2 Framework and Notations

Before starting our discussion let us briefly introduce some of the notations we will need. For some countable index set we denote by , , the space of real sequences with norm

and as

usual. For simplicity of notation, in the following

will denote the -norm .

As is customary for an index set, we assume we have a natural

enumeration order for the elements of , using (implicitly)

a one-to-one map from to . In some convergence

proofs, we shall use the shorthand notations for ,

and (in the case where is infinite)

for .

We also assume that we have a suitable frame indexed by the countable

set . This means that there exist constants

such that

| (3) |

Orthonormal bases are particular examples of frames, but there also exist many interesting frames in which the are not linearly independent. Frames allow for a (stable) series expansion of any of the form

| (4) |

where . The linear operator (called the synthesis map in frame theory) is bounded because of (3). When is a frame but not a basis, the coefficients need not be unique. For more details on frames and their differences from bases we refer to [11].

We shall assume that is sparse, i.e., that can be written by a series of the form (4) with only a small number of non-vanishing coefficients with respect to the frame , or that is compressible, i.e., that can be well-approximated by such a sparse expansion. This can be modeled by assuming that the sequence is contained in a (weighted) -space. Indeed, the minimization of the norm promotes such sparsity. (This has been known for many years, and put to use in a wide range of applications, most notably in statistics. David Donoho calls one form of it the Logan phenomenon in [28] – see also [27] –, after its first observation by Ben Logan [37].) These considerations lead us to model the reconstruction of a sparse as the minimization of the following functional:

| (5) |

where we will assume that the data and the linear operator are given. The second term in (5) is often called the penalization or regularizing term; the first term goes by the name of discrepancy,

| (6) |

In what follows we shall drop the subscript , because the space in which we work will always be clear from the context. We discuss the problem of finding (approximations to) in that minimize the functional (5). (We adopt the usual convention that for , the penalty term “equals” , and that, for such , for all . Since we want to minimize , we shall consider, implicitly, only .) The solutions to the original problem are then given by .

Several authors have proposed independently an iterative soft-thresholding algorithm to approximate the solution [31, 42, 43, 29]. More precisely, is the limit of sequences defined recursively by

| (7) |

starting from an arbitrary , where is the soft-thresholding operation defined by with

| (8) |

Convergence of this algorithm was proved in [21]. Soft-thresholding plays a role in this problem because it leads to the unique minimizer of a functional combining and norms, i.e., (see [10, 21])

| (9) |

We will call the iteration (7) the iterative soft-thresholding algorithm or the thresholded Landweber iteration.

(a) (b)

3 Discussion of the Thresholded Landweber Iteration

The problem of finding the sparsest solution to the under-determined linear equation is a hard combinatorial problem, not tractable numerically except in relatively low dimensions. For some classes of , however, one can prove that the problem reduces to the convex optimization problem of finding the solution with the smallest norm [26, 7, 4, 6]. Even for outside this class, minimization seems to lead to very good approximations to the sparsest solutions. It is in this sense that an algorithm of type (7) could conceivably be called ‘fast’: it is fast compared to a brute-force exhaustive search for the sparsest .

A more honest evaluation of the speed of convergence of algorithm (7) is a comparison with linear solvers that minimize the corresponding penalized functional, such as, e.g., the conjugate gradient method. One finds, in practice, that the thresholded Landweber iteration (7) is not competitive at all in this comparison. It is, after all, the composition of thresholding with the (linear) Landweber iteration , which is a gradient descent algorithm with a fixed step size, known to converge usually quite slowly; interleaving it with the nonlinear thresholding operation does unfortunately not change this slow convergence. On the other hand, this nonlinearity did foil our attempts to “borrow a leaf” from standard linear steepest descent methods by using an adaptive step length – once we start taking larger steps, the algorithm seems to no longer converge in at least some numerical experiments.

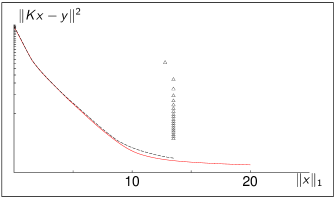

We take a closer look at the characteristic dynamics of the thresholded Landweber iteration in Figure 1. As this plot of the discrepancy versus shows, the algorithm converges initially relatively fast, then it overshoots the value (where ), and it takes very long to re-correct back. In other words, starting from , the algorithm generates a path that is initially fully contained in the -ball , with . Then it gets out of the ball to slowly inch back to it in the limit. A first intuitive way to avoid this long “external” detour is to force the successive iterates to remain within the ball . One method to achieve this is to substitute for the thresholding operations the projection , where, for any closed convex set , and any , we define to be the unique point in for which the distance to is minimal. With a slight abuse of notation, we shall denote by ; this will not cause confusion, because it will be clear from the context whether the subscript of is a set or a positive number. We thus obtain the following algorithm: Pick an arbitrary , for example , and iterate

| (10) |

We will call this the projected Landweber iteration.

The typical dynamics of this projected Landweber algorithm are illustrated in Fig. 1(a). The norm no longer overshoots , but quickly takes on the limit value (i.e., ); the speed of convergence remains very slow, however. In this projected Landweber iteration case, modifying the iterations by introducing an adaptive “descent parameter” in each iteration, defining by

| (11) |

does lead, in numerical simulations, to promising, converging results (in which it differs from the soft-thresholded Landweber iteration, where introducing such a descent parameter did not lead to numerical convergence, as noted above).

The typical dynamics of this modified algorithm are illustrated in Fig. 1(b), which clearly shows the larger steps and faster convergence (when compared with the projected Landweber iteration in Fig. 1(a)). We shall refer to this modified algorithm as the projected gradient iteration or the projected steepest descent; it will be the main topic of this paper.

The main issue is to determine how large we can choose the successive , and still prove norm convergence of the algorithm in .

There exist results in the literature on convergence of projected gradient iterations, where the projections are (as they are here) onto convex sets, see, e.g., [1, 16] and references therein. These results treat iterative projected gradient methods in much greater generality than we need: they allow more general functionals than , and the convex set on which the iterative procedure projects need not be bounded. On the other hand, these general results typically have the following restrictions:

-

•

The convergence in infinite-dimensional Hilbert spaces (i.e., is countable but infinite) is proved only in the weak sense and often only for subsequences;

-

•

In [1] the descent parameters are typically restricted to cases for which . In [16], it is shown that the algorithm converges weakly for any choice of , for arbitrarily small. Of most interest to us is the case where the are picked adaptively, can grow with , and are not limited to values below ; this case is not covered by the methods of either [1] or [16].

To our knowledge there are no results in the literature for which the whole sequence converges in the Hilbert space norm to a unique accumulation point, for “descent parameters” . It is worthwhile emphasizing that strong convergence is not automatic: in [16, Remark 5.12], the authors provide a counterexample in which strong convergence fails. (This question had been open for some time.) One of the main results of this paper is to prove a theorem that establishes exactly this type of convergence; see Theorem 5.18 below. Moreover, the result is achieved by imposing a choice of which ensures a monotone decay of a suitable energy. This establishes a principle of best descent similar to the well-known steepest-descent in unconstrained minimization.

Before we get to this theorem, we need to build some more machinery first.

4 Projections onto -Balls via Thresholding Operators

In this section we discuss some properties of -projections onto -balls. In particular, we investigate their relations with thresholding operators and their explicit computation. We also estimate the time complexity of such projections in finite dimensions.

We first observe a useful property of the soft-thresholding operator.

Lemma 4.1

For any fixed and for , is a piecewise linear, continuous, decreasing function of ; moreover, if then and for .

Proof: ; the sum in the right hand side is finite for .

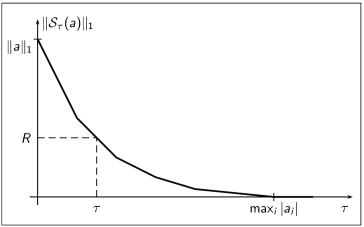

A schematic illustration is given in Figure 2.

The following lemma shows that the projection can be obtained by a suitable thresholding of .

Lemma 4.2

If , then the projection of on the ball with radius is given by where (depending on and ) is chosen such that . If then .

Proof: Suppose . Because, by Lemma 4.1, is continuous in and for sufficiently large , we can choose such that . (See Figure 2.) On the other hand (see above, or [10, 21]), is the unique minimizer of , i.e.,

for all . Since , it follows that

Hence is closer to than any other in . In other words, .

These two lemmas prescribe the following simple recipe for computing the projection . In a first step, sort the absolute values of the components of (an operation if is finite), resulting in the rearranged sequence , with for all . Next, perform a search to find such that

or equivalently,

the complexity of this step is again .

Finally, set

,

and . Then

These formulas were also derived in [35, Lemma 4.1 and Lemma 4.2], by observing that , where

| (12) |

The latter is again a thresholding operator, but it is related to an penalty term. Similar descriptions of the projection onto balls appear also in [5].

Finally, has the following additional properties:

Lemma 4.3

For any , is characterized as the unique vector in such that

| (13) |

Moreover the projection is non-expansive:

| (14) |

for all .

The proof is standard for projection operators onto convex sets; we include it because its technique will be used often in this paper.

Proof: Because is convex, for all and . It follows that for all . This implies

for all . It follows that

which proves (13).

5 The Projected Gradient Method

We have now collected all the terminology needed to identify some conditions on the that will ensure convergence of the , defined by (11), to , the minimizer in of . For notational simplicity we set . With this notation, the thresholded Landweber iteration (7) can be written as

| (15) |

As explained above, we consider, instead of straightforward soft-thresholding with fixed , adapted soft-thresholding operations that correspond to the projection operator :

| (16) |

The dependence of on is described above; is kept fixed throughout the iterations. If, for a given value of , were picked such that (where is the minimizer of ), then Lemma 4.2 would ensure that . Of course, we don’t know, in general, the exact value of , so that we can’t use it as a guideline to pick . In practice, however, it is customary to determine for a range of -values; this then amounts to the same as determining for a range of .

We now propose to change the step into a step (in the spirit of the “classical” steepest descent method), and to define the algorithm: Pick an arbitrary , for example , and iterate

| (17) |

In this section we prove the norm convergence of this algorithm to a minimizer of in , under some assumptions on the descent parameters .

5.1 General properties

We begin with the following characterization of the minimizers of on .

Lemma 5.1

The vector is a minimizer of on if and only if

| (18) |

for any , which in turn is equivalent to the requirement that

| (19) |

To lighten notation, we shall drop the subscript on

whenever no confusion is possible.

Proof: If minimizes on , then

for all , and for all ,

This implies

| (20) |

It follows from this that, for all and for all ,

| (21) |

Conversely, if , then for all and for all :

This implies

In other words:

or

This implies that minimizes on .

The minimizer of on need not be unique. We have, however

Lemma 5.2

If are two distinct minimizers of

on , then , i.e., .

Conversely, if , if minimizes and if then minimizes as well.

Proof: The converse is obvious; we prove only the direct

statement.

From the last inequality in the proof of Lemma 5.1 we

obtain

,

which implies .

In what follows we shall assume that the minimizers of in are not global minimizers for , i.e., that . We know from Lemma 4.2 that can be computed for simply by finding the value such that ; one has then . Using this we prove

Lemma 5.3

Let be the common image under of all minimizers of on , i.e., for all minimizing in , . Then there exists a unique value such that, for all and for all minimizing

| (22) |

Moreover, for all we have that if there exists a minimizer such that , then

| (23) |

Proof: From Lemma 4.2 and Lemma 5.1, we know that for each minimizing , and each , there exists a unique such that

| (24) |

For we have ; this implies and also that . If then . It

follows that does not depend on the choice of . Moreover, if

there is a minimizer for which ,

then .

Lemma 5.4

If, for some , two minimizers satisfy and , then .

Proof: This follows from the arguments in the previous proof;

implies . Similarly, implies , so that .

This immediately leads to

Lemma 5.5

For all that minimize , there are only finitely many . More precisely,

| (25) |

Moreover, if the vector is defined by

| (26) |

then for each minimizer of in .

Proof: We have already proved the set inclusion. Note that, since , the set is necessarily a finite set. We also have, for each minimizer ,

Remark 5.6 By changing, if necessary, signs of the canonical basis vectors, we can assume, without loss of generality, that for all . We shall do so from now on.

5.2 Weak convergence to minimizing accumulation points

We shall now impose some conditions on the . We shall see examples in Section 6 where these conditions are verified.

Definition 5.7

We say that the sequence satisfies Condition (B) with respect to the sequence if there exists so that:

| (B1) | ||||

| (B2) |

We shall often abbreviate this by saying that ‘the satisfy Condition (B)’. The constant used in this definition is . (We can always assume, without loss of generality, that ; if necessary, this can be achieved by a suitable rescaling of and .)

Note that the choice for all , which corresponds to the projected Landweber iteration, automatically satisfies Condition (B); since we shall show below that we obtain convergence when the satisfy Condition (B), this will then establish, as a corollary, convergence of the projected Landweber iteration algorithm (10) as well. We shall be interested in choosing, adaptively, larger values of ; in particular, we like to choose as large as possible.

Remark 5.8

-

•

Condition (B) is inspired by the standard length-step in the steepest descent algorithm for the (unconstrained, unpenalized) functional . In this case, one can speed up the standard Landweber iteration by defining instead , where is picked so that it gives the largest decrease of in this direction. This gives

(27) In this linear case, one easily checks that also equals

(28) in fact, it is this latter expression for (which inspired the formulation of Condition (B)) that is most useful in proving convergence of the steepest descent algorithm.

-

•

Because the definition of involves , the inequality (B2), which uses to impose a limitation on , has an “implicit” quality. In practice, it may not be straightforward to pick appropriately; one could conceive of trying first a “greedy” choice, such as e.g. ; if this value works, it is retained; if it doesn’t, it can be gradually decreased (by multiplying it with a factor slightly smaller than 1) until (B2) is satisfied. (A similar way of testing appropriate step lengths is adopted in [32].)

In this section we prove that if the sequence is defined iteratively by (11), and if the used in the iteration satisfy Condition (B) (with respect to the ), then the (weak) limit of any weakly convergent subsequence of is necessarily a minimizer of in .

Lemma 5.9

Assume and . For arbitrary fixed in , define the functional by

| (29) |

Then there is a unique choice for in that minimizes the restriction to of . We denote this minimizer by ; it is given by .

Proof: First of all, observe that the functional is strictly convex, so that it has a unique minimizer on ; let be this minimizer. Then for all and for all

The latter implication is equivalent to by Lemma 4.3.

An immediate consequence is

Lemma 5.10

If the are defined by (11), and the satisfy Condition (B) with respect to the , then the sequence is decreasing, and

| (30) |

Proof: Comparing the definition of in (11) with the statement of Lemma 5.9, we see that , so that is the minimizer, for , of . Setting , we have

We also have

This implies

Therefore, the series

converges and .

Because the set is bounded in ( are all in ), it is bounded in as well (since ). Because bounded closed sets in are weakly compact, the sequence must have weak accumulation points. We now have

Proposition 5.11 (Weak convergence to minimizing accumulation points)

If is a weak accumulation point of then minimizes in .

Proof: Let be a subsequence converging weakly to . Then for all

| (31) |

Therefore . From Lemma 5.10 we have , so that we also have . By the definition of (), and by Lemma 4.3, we have, for all ,

| (32) |

In particular, specializing to our subsequence and taking the , we have

| (33) |

Because , for , and is uniformly bounded, we have

| (34) |

so that our inequality reduces to

| (35) |

By adding , which also tends to zero as , we transform this into

| (36) |

Since the are all in , it follows that

| (37) |

or

| (38) |

where we have used the weak convergence of . This can be rewritten as

| (39) |

Since , we have

We conclude thus that

| (40) |

so that is a minimizer of on , by Lemma 5.1.

5.3 Strong convergence to minimizing accumulation points

In this subsection we show how the weak convergence established in the preceding subsection can be strengthened into norm convergence, again by a series of lemmas. Since the distinction between weak and strong convergence makes sense only when the index set is infinite, we shall implicitly assume this is the case throughout this section.

Lemma 5.12

For the subsequence defined in the proof of Proposition

5.11,

.

Proof: Specializing the inequality (39) to , we obtain

together with (a consequence of the weak convergence of

to ),

this implies , and thus .

Lemma 5.13

Under the same assumptions as in Proposition 5.11, there exists a subsequence of such that

| (41) |

Proof: Let be the subsequence defined in the proof of Proposition 5.11. Define now and . Since, by Lemma 5.10, , we have . On the other hand,

where we have used Proposition 5.11 ( is a

minimizer) and Lemma 5.1 (so that

). By Lemma

5.12, . Since

the are uniformly bounded, we have, by formula

(14),

Combining this with , we obtain

| (42) |

Since the are uniformly bounded, they must have at least one accumulation point. Let be such an accumulation point, and choose a subsequence such that . To simplify notation, we write , , . We have thus

| (43) |

Denote and . We have now

Since both terms on the right hand side converge to zero for (see (43)), we have

| (44) |

Without loss of generality we can assume . By Lemma 4.2 there exists such that . Because as , this implies that, for some finite , for . Pick now any that satisfies . There exists a finite so that . Set , and define the vector by if , if .

By the weak convergence of the , we can, for this same , determine such that, for all , . Define new vectors by if , if .

Because of (44), there exists such that for . Consider now . We have

On the other hand, Lemma 4.2 tells us that there exists such that , where we used in the last equality that for and for . From we conclude that for all . We then deduce

Because we picked , this is possible only if for all , , and if, in addition,

| (45) |

It then follows that .

We have thus obtained what we set out to prove: the subsequence of satisfies that, given arbitrary , there exists so that, for , .

Remark 5.14 In this proof we have implicitly assumed that . Given that , this assumption can be made without loss of generality, because it is not possible to have and infinitely often, as the following argument shows. Find such that and, and : . Then . Hence, , .

Remark 5.15 At the cost of more technicalities it is possible to show that the whole subsequence defined in the proof of Proposition 5.11 converges in norm to , i.e., that , without going to a subsequence .

The following proposition summarizes in one statement all the findings of the last two subsections.

Proposition 5.16 (Norm convergence to minimizing accumulation points)

Every weak accumulation point of the sequence defined by (11) is a minimizer of in . Moreover, there exists a subsequence of that converges to in norm.

5.4 Uniqueness of the accumulation point

In this subsection we prove that the accumulation point of is unique, so that the entire sequence converges to in norm. (Note that two sequences and , both defined by the same recursion, but starting from different initial points , can still converge to different limits and .)

We start again from the inequality

| (46) |

for all and for all , and its many consequences. Define to be the set of minimizers of on . By Lemma 5.2, , where is an arbitrary minimizer of in . By the convention adopted in Remark 5.1,

| (47) |

Moreover, for each element , if (see Lemma 5.5). The set is both closed and convex. We define the corresponding (nonlinear) projection operator as usual,

| (48) |

Because is convex, this projection operator has the following property:

| (49) |

(The proof is standard, and is essentially given in the proof Lemma 4.3, where in fact only the convexity of was used.) For each , we introduce now and defined by

| (50) |

Specializing equation (49) to , we obtain, for all and for all :

| (51) |

or

| (52) |

Because is a minimizer, we can also apply Lemma 5.1 to and conclude

| (53) |

With these inequalities, we can prove the following crucial result.

Lemma 5.17

For any , and for any ,

| (54) |

Proof: We set in (46), leading to

| (55) |

where we have used that . We also have, setting in the -version of (53),

| (56) |

or

| (57) |

where we have used . It follows that

| (58) |

or

| (59) |

which is also equivalent to

| (60) |

Adding to (60), we have

It follows that

| (61) |

which, in turn, implies that

| (62) |

This can be rewritten as

| (63) |

which implies .

We are now ready to state the main result of our work.

Theorem 5.18

The sequence as defined in (11), where the step-length sequence satisfies Condition (B) with respect to the , converges in norm to a minimizer of on .

6 Numerical Experiments and Additional Algorithms

6.1 Numerical examples

We conduct a number of numerical experiments to gauge the effectiveness of the different algorithms we discussed. All computations were done in Mathematica 5.2 [46] on a 2Ghz workstation with 2Gb memory.

We are primarily interested in the behavior, as a function of time (not number of iterations), of the relative error . To this end, and for a given operator and data , we need to know in advance the actual minimizer of the functional (5).

One can calculate the minimizer exactly (in practice up to computer

round-off) with a finite number of steps using the LARS algorithm

described in [29] (the variant called ‘Lasso’,

implemented independently by us). This algorithm scales badly, and

is useful in practice only when the number of non-zero entries in

the minimizer is sufficiently small. We made our own

implementation of this algorithm to make it more directly applicable

to our problem (i.e., we do not renormalize the columns of the

matrix to have zero mean and unit variance, as it is done in the

statistics context [29]). We also double-check the

minimizer obtained in this manner by verifying that it is indeed a

fixed point of the iterative thresholding algorithm

(7) (up to machine epsilon). We then have an

‘exact’ minimizer together with its radius

(used in the projected algorithms) and, according to Lemma

5.3, the corresponding threshold

with (used in the

iterative thresholding algorithm).

The numerical examples below are listed in order of increasing complexity; they illustrate that the algorithms can behave differently for different examples. In these experiments we choose , (where, as before, ); is the standard descent parameter from the classical linear steepest descent algorithm.

-

1.

When is a partial Fourier matrix (i.e., a Fourier matrix with a prescribed number of deleted rows), there is no advantage in using a dynamical step size as this ratio is always equal to 1. This trivially fulfills Condition (B) in Section 5.1. The performance of the projected steepest descent iteration simply equals that of the projected Landweber iterations.

-

2.

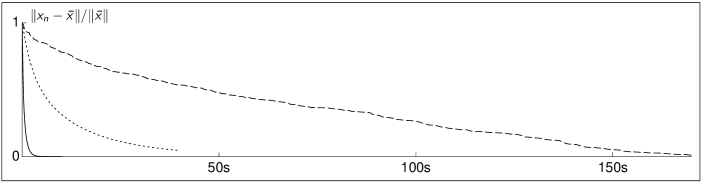

By combining a scaled partial Fourier transform with a rank 1 projection operator, we constructed our second example, in which is a matrix, of rank , with largest singular value equal to 0.99 and all the other singular values between 0.01 and 0.11. Because of the construction of the matrix, the FFT algorithm provides a fast way of computing the action of this matrix on a vector. For the and that were chosen, the limit vector has nonzero entries. For this example, the LARS procedure is slower than thresholded Landweber, which in turn is significantly slower than projected steepest descent. To get within a distance of the true minimizer corresponding to a relative error, the projected steepest descent algorithm takes , the thresholded Landweber algorithm , and LARS . (The relatively poor performance of LARS in this case is due to the large number of nonzero entries in the limit vector ; the complexity of LARS is cubic in this number of nonzero entries.) In this case, the are much larger than 1; moreover, they satisfy Condition (B) of Section 5.1 at every step. We illustrate the results in Figure 3.

Figure 3: The different convergence rates of the thresholded Landweber algorithm (dotted line), the projected steepest descent algorithm (solid line, near vertical axis) and the LARS algorithm (dashed line), for the second example. The projected steepest descent algorithm converges much faster than the thresholded Landweber iteration. They both do better than the LARS method. -

3.

The last example is inspired by a real-life application in geoscience [38], in particular an application in seismic tomography based on earthquake data. The object space consists of the wavelet coefficients of a 2D seismic velocity perturbation. There are degrees of freedom. In this particular case the number of data is . Hence the matrix has rows and columns. We apply the different methods to the same noisy data that are used in [38] and measure the time to convergence up to a specified relative error (see Table 1 and Figure 4). This example illustrates the slow convergence of the thresholded Landweber algorithm (7), and the improvements made by a projected steepest descent iteration (11) with the special choice above. In this case, this choice turns out not to satisfy Condition (B) in general. One could conceivably use successive corrections, e.g. by a line-search, to determine, starting from , values of that would satisfy condition (B), and thus guarantee convergence as established by Theorem 5.18. This would slow down the method considerably. The seem to be in the right ballpark, and provide us with a numerically converging sequence. We also implemented the projected Landweber algorithm (10); it is listed in Table 1 and illustrated in Figure 4.

The matrix in this example is extremely ill-conditioned: its largest singular value was normalized to 1, but the remaining singular values quickly tend to zero. The threshold was chosen, according to the (known or estimated) noise level in the data, so that ( = the number of data points), where is the data noise level; this is a standard choice that avoids overfitting.

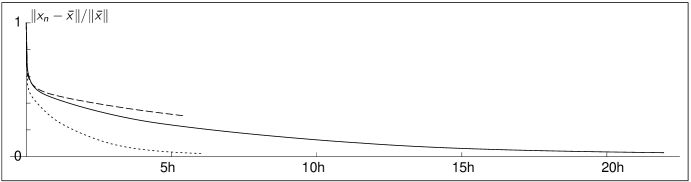

Figure 4: The different convergence rates of the thresholded Landweber algorithm (solid line), the projected Landweber algorithm (dashed line) and the projected steepest descent algorithm (dotted line), for the third example. The projected steepest descent algorithm converges about four times faster than the thresholded Landweber iteration. The projected Landweber iteration does better at first (not visible in this plot), but looses with respect to iterative thresholding afterwards. The horizontal axis has time (in hours), the vertical axis displays the relative error. In Figure 4, we see that the thresholded Landweber algorithm takes more than hours (corresponding to iterations) to converge to the true minimizer within a relative error, as measured by the usual distance. The projected steepest descent algorithm is about four times faster and reaches the same reconstruction error in about hours ( iterations). Due to one additional matrix-vector multiplication and, to a minor extent, the computation of the projection onto an -ball, one step in the projected steepest descent algorithm takes approximately twice as long as one step in the thresholded Landweber algorithm. For the projected Landweber algorithm there is an advantage in the first few iterations, but after a short while, the additional time needed to compute the projection (i.e., to compute the corresponding variable thresholds) makes this algorithm slower than the iterative soft-thresholding. We illustrate the corresponding CPU time in Table 1.

It is worthwhile noticing that for the three algorithms the value of the functional (5) converges much faster to its limit value than the minimizer itself: When the reconstruction error is 10%, the corresponding value of the functional is already accurate up to three digits with respect to the value of the functional at . We can imagine that in this case the functional has a long narrow “valley” with a very gentle slope in the direction of the eigenvectors with small (or zero) singular values.

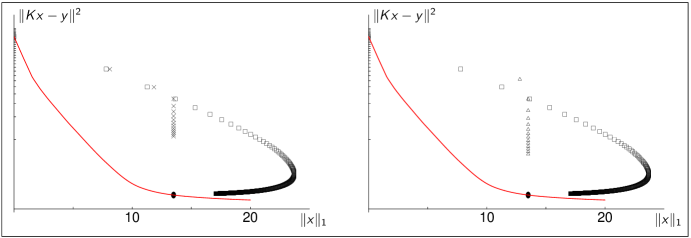

Relative thresholded Landweber projected st. descent projected Landweber error time time time 0.90 3 1s 2 1s 3 2s 0.80 20 8s 8 7s 15 11s 0.70 163 1m8s 20 17s 59 44s 0.50 3216 22m9s 340 4m56s 2124 27m17s 0.20 55473 6h23m 6738 1h37m 0.10 100620 11h38m 11830 2h51m 0.03 198357 21h47m 22037 5h20m Table 1: Table illustrating the relative performance of three algorithms: thresholded Landweber, projected Landweber and projected steepest descent, for the third example. The path in the vs. plane followed by the iterates is shown in Figure 1. The projected steepest descent algorithm, by construction, stays within a fixed -ball, and, as already mentioned, converges faster than the thresholded Landweber algorithm. The path followed by the LARS algorithm is also pictured. It corresponds with the so-called trade-off curve which can be interpreted as the border of the area that is reachable by any element of the model space, i.e., it is generated by for decreasing values of .

In this particular example, the number of nonzero components of equals . The LARS (exact) algorithm only takes seconds, which is much faster than any of the iterative methods demonstrated here. However, as illustrated above, by the second example, LARS looses its advantage when dealing with larger problems where the minimizer is not sparse in absolute number of entries, as is the case in, e.g., realistic problems of global seismic tomography. Indeed, the example presented here is a “toy model” for proof-of-concept for geoscience applications. The 3D model will involve millions of unknowns and solutions that may be sparse compared with the total number of unknowns, but not sparse in absolute numbers. Because the complexity of LARS is cubic in the number of nonzero components of the solution, such 3D problems are expected to lie beyond its useful range.

6.2 Relationship to other methods

The projected iterations (16) and (17) are related to the POCS (Projection on Convex Sets) technique [3]. The projection of a vector on the solution space (a convex set, assumed here to be non-empty; no such assumption was made before because the functional (5) always has a minimum) is given by:

| (65) |

Hence, alternating projections on the convex sets and give rise to the algorithm [5]: : Pick an arbitrary , for example , and iterate

| (66) |

This may be practical in case of a small number of data or when there is structure in , i.e., when is efficiently inverted. Approximating by the unit matrix, yields the projected Landweber algorithm (16); approximating by a constant multiple of the unit matrix yields the projected gradient iteration (17) if one chooses the constant equal to .

The projected methods discussed in this paper produce iterates that (except for the first few) live on the ‘skin’ of the -ball of radius , as shown in Fig. 1. We have found even more promising results for an ‘interior’ algorithm in which we still project on -balls, but now with a slowly increasing radius, i.e.,

| (67) |

where is the prescribed maximum number of iterations (the

origin is chosen as the starting point of this iteration). We do not

have a proof of convergence of this ‘interior point type’

algorithm. We observed (also without proof) that the

path traced by the iterates (in the

vs. plane) is very close to the trade-off curve (see Fig. 5);

this is a useful property in practice since at least part of the trade-off

curve should be constructed anyway.

Note that the strategy followed by these algorithms is similar to that of LARS

[29], in that they both start with and slowly

increase the norm of the successive approximations. It is also related to [36].

While we were finishing this paper, Michael Friedlander informed us

of their numerical results in [45] which are closely related to

our approach,

although their analysis is limited to finite dimensions.

Different, but closely related is also the recent approach by

Figueiredo, Nowak, and Wright [32]. The authors first

reformulate the minimization of (5) as a

bound-constrained quadratic program in standard form, and then they

apply iterative projected gradient iterations, where the projection

act componentwise by clipping to zero negative components.

7 Conclusions

We have presented convergence results for accelerated projected gradient methods to find a minimizer of an penalized functional. The innovation due to the introduction of ‘Condition (B)’ is to guarantee strong convergence for the full sequence. Numerical examples confirm that this algorithm can outperform (in terms of CPU time) existing methods such as the thresholded Landweber iteration or even LARS.

It is important to remark that the speed of convergence may depend strongly on how the operator is available. Because most of the time in the iterations is consumed by matrix-vector multiplications (as is often the case for iterative algorithms), it makes a big difference whether is given by a full matrix or a sparse matrix (perhaps sparse in the sense that its action on a vector can be computed via a fast algorithm, such as the FFT or a wavelet transform). The applicability of the projected algorithms hinges on the observation that the projection on an ball can be computed with a -algorithm, where is the dimension of the underlying space.

There is no universal method that performs best for any choice of the operator, data, and penalization parameter. As a general rule of thumb we expect that, among the algorithms discussed in this paper for which we have convergence proofs,

-

•

the thresholded Landweber algorithm (7) works best for an operator close to the identity (independently of the sparsity of the limit),

-

•

the projected steepest descent algorithm (11) works best for an operator with a relatively nice spectrum, i.e., with not too many zeroes (also independently of the sparsity of the minimizer), and

-

•

the exact (LARS) method works best when the minimizer is sparse in absolute terms.

Obviously, the three cases overlap partially, and they do not cover the whole range of possible operators and data. In future work we intend to investigate algorithms that would further improve the performance for the case of a large ill-conditioned matrix and a minimizer that is relatively sparse with respect to the dimension of the underlying space. We intend, in particular, to focus on proving convergence and other mathematical properties of (67).

8 Acknowledgments

M. F. acknowledges the financial support provided by the European Union’s Human Potential Programme under the contract MOIF-CT-2006-039438. I. L. is a post-doctoral fellow with the F.W.O.-Vlaanderen (Belgium). M.F. and I.L. thank the Program in Applied and Computational Mathematics, Princeton University, for the hospitality during the preparation of this work. I. D. gratefully acknowledges partial support from NSF grants DMS-0245566 and 0530865.

References

- [1] Ya. I. Alber, A. N. Iusem, and M. V. Solodov, On the projected subgradient method for nonsmooth convex optimization in a Hilbert space, Math. Programming 81 (1998), no. 1, Ser. A, 23–35.

- [2] S. Anthoine, Different Wavelet-based Approaches for the Separation of Noisy and Blurred Mixtures of Components. Application to Astrophysical Data., Ph.D. thesis, Princeton University, 2005.

- [3] L. M. Brègman, Finding the common point of convex sets by the method of successive projection, Dokl. Akad. Nauk. SSSR 162 (1965), 487–490.

- [4] E. Candès, J. Romberg, and T. Tao, Stable signal recovery from incomplete and inaccurate measurements, Comm. Pure Appl. Math. 59 (2006), no. 8, 1207–1223.

- [5] E. J. Candès and J. Romberg, Practical signal recovery from random projections., Wavelet Applications in Signal and Image Processing XI, Proc. SPIE Conf. 5914, 2004.

- [6] E. J. Candès, J. Romberg, and T. Tao, Exact signal reconstruction from highly incomplete frequency information, IEEE Trans. Inf. Theory 52 (2006), no. 2, 489–509.

- [7] E. J. Candès and T. Tao, Near-optimal signal recovery from random projections: universal encoding strategies?, IEEE Trans. Inform. Theory 52 (2006), no. 12, 5406–5425.

- [8] E.J. Candès and D. L. Donoho, New tight frames of curvelets and optimal representations of objects with piecewise singularities., Commun. Pure Appl. Math. 57 (2004), no. 2, 219–266.

- [9] C. Canuto and K. Urban, Adaptive optimization of convex functionals in Banach spaces, SIAM J. Numer. Anal. 42 (2004), no. 5, 2043–2075.

- [10] A. Chambolle, R. A. DeVore, N.-Y. Lee, and B. J. Lucier, Nonlinear wavelet image processing: variational problems, compression, and noise removal through wavelet shrinkage, IEEE Trans. Image Process. 7 (1998), no. 3, 319–335.

- [11] O. Christensen, An Introduction to Frames and Riesz Bases, Birkhäuser, Boston, 2003.

- [12] A. Cohen, Numerical Analysis of Wavelet Methods., Studies in Mathematics and its Applications 32. Amsterdam: North-Holland., 2003.

- [13] A. Cohen, W. Dahmen, and R. DeVore, Adaptive wavelet methods for elliptic operator equations — Convergence rates, Math. Comp. 70 (2001), 27–75.

- [14] , Adaptive wavelet methods II: Beyond the elliptic case, Found. Comput. Math. 2 (2002), no. 3, 203–245.

- [15] A. Cohen, M. Hoffmann, and M. Reiss, Adaptive wavelet Galerkin methods for linear inverse problems., SIAM J. Numer. Anal. 42 (2004), no. 4, 1479–1501.

- [16] P. L. Combettes and V. R. Wajs, Signal recovery by proximal forward-backward splitting, Multiscale Model. Simul., 4 (2005), no. 4, 1168–1200.

- [17] S. Dahlke, M. Fornasier, and T. Raasch, Adaptive frame methods for elliptic operator equations, Adv. Comput. Math. 27 (2007), no. 1, 27–63.

- [18] S. Dahlke, M. Fornasier, T. Raasch, R. Stevenson, and M. Werner, Adaptive frame methods for elliptic operator equations: The steepest descent approach, IMA J. Numer. Anal. (2007), doi 10.1093/imanum/drl035.

- [19] S. Dahlke and P. Maass, An outline of adaptive wavelet Galerkin methods for Tikhonov regularization of inverse parabolic problems., Hon, Yiu-Chung (ed.) et al., Recent development in theories and numerics. Proceedings of the international conference on inverse problems, Hong Kong, China, January 9-12, 2002. River Edge, NJ: World Scientific. 56-66 , 2003.

- [20] I. Daubechies, Ten Lectures on Wavelets, SIAM, 1992.

- [21] I. Daubechies, M. Defrise, and C. DeMol, An iterative thresholding algorithm for linear inverse problems, Comm. Pure Appl. Math. 57 (2004), no. 11, 1413–1457.

- [22] I. Daubechies and G. Teschke, Variational image restoration by means of wavelets: Simultaneous decomposition, deblurring, and denoising., Appl. Comput. Harmon. Anal. 19 (2005), no. 1, 1–16.

- [23] D. L. Donoho, Superresolution via sparsity constraints., SIAM J. Math. Anal. 23 (1992), no. 5, 1309–1331.

- [24] , De-noising by soft-thresholding., IEEE Trans. Inf. Theory 41 (1995), no. 3, 613–627.

- [25] , Nonlinear solution of linear inverse problems by wavelet-vaguelette decomposition., Appl. Comput. Harmon. Anal. 2 (1995), no. 2, 101–126.

- [26] D. L. Donoho, Compressed sensing, IEEE Trans. Inf. Theory 52 (2006), no. 4, 1289–1306.

- [27] D. L. Donoho and B. F. Logan, Signal recovery and the large sieve, SIAM Journal on Applied Mathematics 52 (1992), 577–591.

- [28] D. L. Donoho and P. Starck, Uncertainty principles and signal recovery, SIAM J. Appl. Math 49 (1989), 906–931.

- [29] B. Efron, T. Hastie, I. Johnstone, and R. Tibshirani, Least angle regression, Ann. Statist. 32 (2004), no. 2, 407–499.

- [30] H.W. Engl, M. Hanke, and A. Neubauer, Regularization of Inverse Problems., Mathematics and its Applications (Dordrecht). 375. Dordrecht: Kluwer Academic Publishers., 1996.

- [31] M. A. T. Figueiredo and R. D. Nowak, An EM algorithm for wavelet-based image restoration., IEEE Trans. Image Proc. 12 (2003), no. 8, 906–916.

- [32] M. A. T. Figueiredo, R. D. Nowak, and S. J. Wright, Gradient projection for sparse reconstruction: Application to compressed sensing and other inverse problems, to appear in IEEE Journal of Selected Topics in Signal Processing, (2007).

- [33] M. Fornasier and F. Pitolli, Adaptive iterative thresholding algorithms for magnetoenceophalography (MEG), (2007), preprint.

- [34] M. Fornasier and H. Rauhut, Iterative thrsholding algorithms, (2007), preprint.

- [35] , Recovery algorithms for vector valued data with joint sparsity constraints, SIAM J. Numer. Anal. (2007), to appear.

- [36] E.T. Hale, W. Yin and Y. Zhang, A fixed-point continuation method for -regularized minimization with applications to compressed sensing, Technical report, Rice University, 2007.

- [37] B. F. Logan, Properties of High-Pass Signals, Ph.D. thesis, Columbia University, 1965.

- [38] I. Loris, G. Nolet, I. Daubechies, and F. A. Dahlen, Tomographic inversion using -norm regularization of wavelet coefficients, Geophysical Journal International 170 (2007), no. 1, 359–370

- [39] S. Mallat, A Wavelet Tour of Signal Processing. 2nd Ed., San Diego, CA: Academic Press., 1999.

- [40] R. Ramlau and G. Teschke, Tikhonov replacement functionals for iteratively solving nonlinear operator equations., Inverse Probl. 21 (2005), no. 5, 1571–1592.

- [41] H. Rauhut, Random sampling of sparse trigonometric polynomials, Appl. Comput. Harm. Anal. 22 (2007), no. 1, 16–42.

- [42] J.-L. Starck, E. J. Candès, and D. L. Donoho, Astronomical image representation by curvelet transform, Astronomy and Astrophysics 298 (2003), 785–800.

- [43] J.-L. Starck, M. K. Nguyen, and F. Murtagh, Wavelets and curvelets for image deconvolution: a combined approach, Signal Proc. 83 (2003), 2279–2283.

- [44] G. Teschke, Multi-frame representations in linear inverse problems with mixed multi-constraints, Appl. Comput. Harm. Anal. 22 (2007), no. 1, 43–60.

- [45] E. van den Berg and M. P. Friedlander, In pursuit of a root, preprint, (2007).

- [46] S. Wolfram, The Mathematica Book, Fifth ed., Wolfram Media/Cambridge University Press, 2003.